<p>A flooded house is seen during the Hurricane Florence in Duplin County, North Carolina, on September 15, 2018. (Photo by Atilgan Ozdil/Anadolu Agency/Getty Images)</p>

Authorization of the National Flood Insurance Program (NFIP) would have ended today had it not been for Congress’s temporary reauthorization for another year, which awaits the president’s signature. This marks Congress’s 16th temporary extension since 2017’s devastating Hurricanes Harvey, Irma, and Maria. The program’s funding challenges stem from Hurricanes Katrina and Rita in 2005 and Superstorm Sandy in 2012, which resulted in insurance claims that generated a massive drain on federal coffers. As of this year, the program is more than $20 billion in debt.

Kicking the can

New program laws are transforming the NFIP over time (PDF) to be based on actuarial risks of flooding—eliminating the costs to the program from older, lower rates and effectively discouraging living in flood-prone places.

The NFIP’s long-term solvency is still uncertain, given the increase in flood events and populations in harm’s way. Homeowner premiums may not fully match risk or accurately account for the projected risks from climate change’s effects. Currently, premiums do not fully account for current public works for flood mitigation or a variety of property-level interventions hat could mitigate flood risks. And, importantly, neither the NFIP nor the broader federal flood management policy addresses the disproportionate burdens on low-income policyholders and households of color living in exposed communities.

Several proposals suggest improvements to NFIP affordability challenges—including subsidies for low- and moderate-income homeowners living in flood zones—and discourage new development and purchases of existing homes in high-risk areas.

But solutions to incorporate racial and wealth equity in NFIP reforms must go beyond the affordability of accessing a policy and explore possible disparities in the treatment of households after purchasing policies.

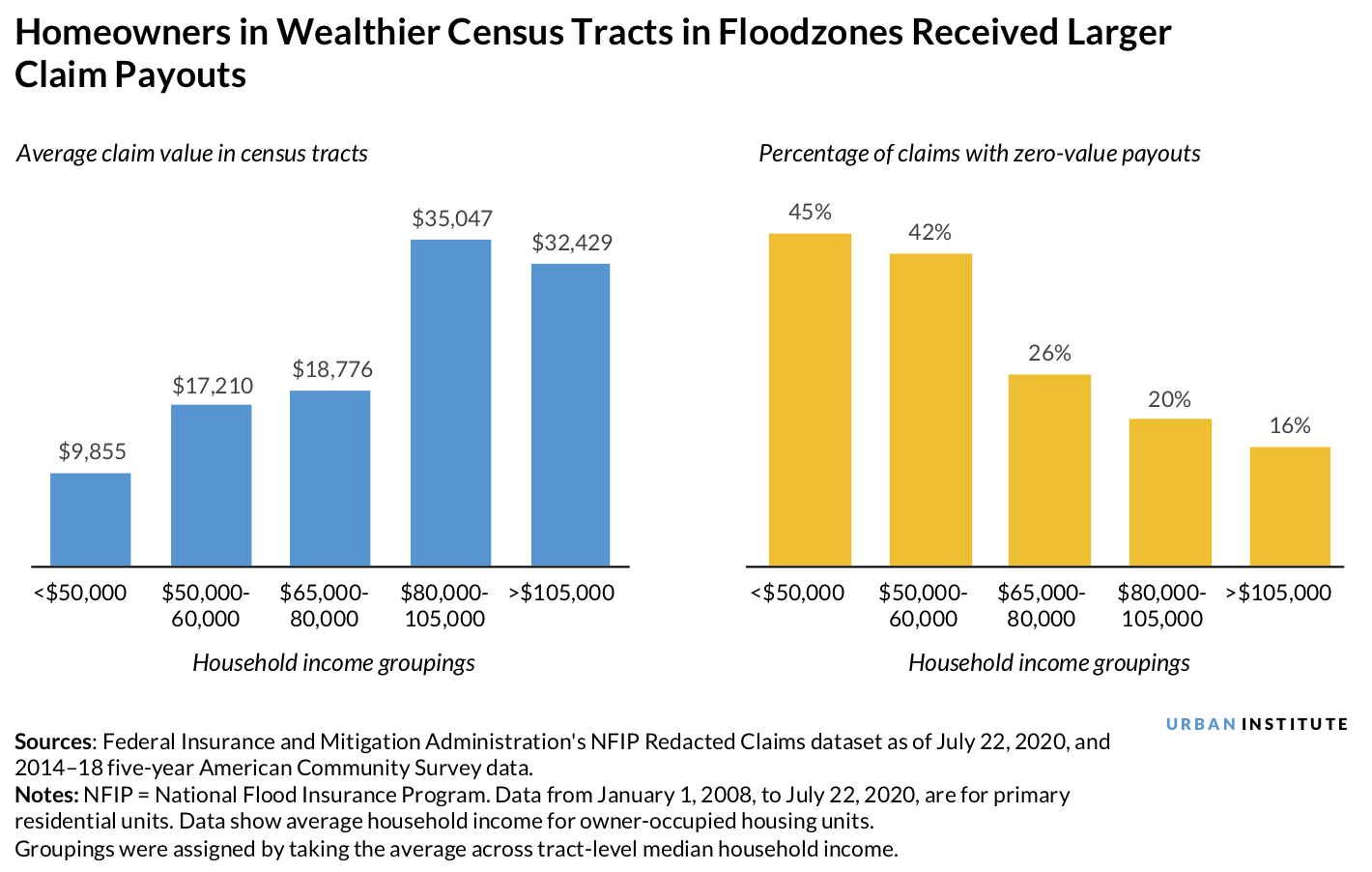

How claims are treated by policyholder race and income in New Orleans

Urban Institute staff recently explored whether residents of the greater New Orleans region have equal access to the benefits of NFIP-issued flood insurance by examining claim payment amounts and nonpayment rates across census tracts by race and income. We found that claims from homeowners who filed for property and content damages were distributed fairly evenly across racial and income lines, though disproportionately more claims came from census tracts within flood zones with higher average incomes than tracts with lower average incomes. We grouped nonwhite populations in tracts to limit sampling error for individual races and ethnicities in tracts with small populations.

Yet, when we explored the value of awards from claims and rates of nonpayment, we found significant disparities. On average, households in census tracts where more than 50 percent of the homeowners are white receive more on their NFIP claims and encounter a lower rate of unpaid claims than households in tracts where more than 50 percent of homeowners are people of color. This was true across the region for all claims and for households within flood zones tracts only.

We found similar patterns across communities by average household income for homeowners in flood zones in the greater New Orleans region (who are thus required to have flood insurance).

This analysis does not control for damage severity, homes’ overall construction quality, the average home value in census tracts, the differences in claim values, and payout rates—all of which raise important questions that could further explain inequities. For example, low-income households and households of color are more likely to live in poor-quality housing that could be more extensively damaged from a hazard event. Overt discrimination may also play a role in differences in treatment for claims.

Underlying this disparity is the systemic undervaluation of housing and possessions in low-income communities and communities of color. As with sale and assessed values, the insured value (PDF) of a home is still partially based on factors stemming from historical racial and income segregation. Valuation disparity in post-disaster conditions has been challenged before in the New Orleans region, when the Louisiana Fair Housing Action Center, Urban’s local partner, successfully won a settlement with the state and federal governments for undervaluing Hurricane Katrina recovery assistance to African American homeowners by basing aid on pre-Katrina property values rather than damages.

Further, claim awards based on home values do not reflect the disproportionate effects that even minor property damage has on the budgets of lower-income households and communities of color. Hazard events many not discriminate, but the preexisting vulnerabilities they exacerbate and their subsequent disparate effects and access to recovery resources do.

How to center equity in NFIP and disaster reform

The NFIP was originally created in 1968 with the assumption that it could partially substitute for federal emergency aid after events. That did not happen, but with the growing awareness of increasing risks to coastal and riverine communities, the opportunities to transform NFIP and reform the nation’s overall risk management and emergency policy framework are huge. Stakeholders in the disaster field could consider the following actions:

- Fair housing advocates and monitors can ensure fair housing laws regarding access and treatment to housing related services and requirements include hazard insurance.

- The NFIP can expand data collection and analysis of households’ purchases of home polices as well as treatment of policyholders by collecting demographic information to better assess disparities.

- State and local governments can support homebuyer, homeowner, and tenant education targeted at insurance awareness through advocates and home counseling and services.

- Federal policymakers can continue reforming the NFIP by integrating one of the affordability options (PDF) for low-income policyholders put forth by the Federal Emergency Management Agency (FEMA).

- FEMA, the US Department of Housing and Urban Development, the US Army Corps of Engineers, and local public works agencies can prioritize low-income communities and communities of color when they allocate federal investments in flood mitigation infrastructure.

- FEMA can increase funding for and require state emergency management officials conduct more outreach to low-income communities and communities of color for property-level mitigation opportunities, such as flood proofing, elevating, and buying out homes. They can administer these services more efficiently and effectively for households that cannot afford to wait.

- Federal and state lawmakers could also increase funds and remove local regulations to increase affordable, denser housing options outside of flood zones, creating incentives for safer building and reducing vulnerability.

Evidence suggests insurance changes are an integral part of comprehensive reforms of the country’s risk and emergency management policy framework. But to make reforms truly comprehensive, policymakers should r center equitable access to resources and outcomes.

Far too often, low-income neighbors and residents of color have lacked access to resources to prepare themselves and their homes before hazards hit, and they slip through the cracks during recovery efforts. These barriers exist because of historical decisions that limit where we live and our inconsistent principles around managing collective risks and devastations. We now have the opportunity to correct both.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.