<p>Photo via Shutterstock.</p>

Correction: The total loans purchased in the first table were corrected on 4/6/2018 by adding 100,000 to the loan count for every month except Jan-17.

Several private mortgage insurers (PMIs) announced recently that they will be more restrictive in insuring mortgages for borrowers who have debt that is 45 percent or more of their income. Some PMIs will insure mortgages for these borrowers only when the borrowers’ credit scores are 700 or above, and other insurers will charge higher fees for insuring these mortgages.

The PMIs realized that a purportedly “risk neutral” change in Fannie Mae’s underwriting criteria, implemented last summer to ease access to mortgage credit, had actually increased the risk these mortgages would default. Fannie Mae’s move eased credit availability and increased the volume of high-DTI (debt-to-income) loans, many of which also had high loan-to-value (LTV) ratios. This forced the PMIs to react.

The PMIs’ need for a quick adjustment illustrates how well-intentioned efforts to improve credit availability can run into roadblocks. For a robust and smoothly functioning housing finance system, we need to keep in mind the difficulties of balancing mortgage risk with mortgage access, and we need to elevate transparency.

Why did PMIs tighten their criteria?

Last May, Fannie Mae announced that, effective July 29, 2017, it would relax underwriting criteria by increasing the maximum DTI ratio a borrower could have and still qualify for a Fannie-backed loan from 45 percent to 50 percent. Urban Institute research supported the change, showing it would likely result in the approval of an additional 95,000 mortgages (85,000 of them Fannie mortgages) and improve credit availability.

Fannie Mae had allowed the delivery of high-DTI loans before the July 29 change, but these loans required 12 months of reserves and an LTV ratio of 80 percent or less, which limited the number of borrowers who qualified.

The July change lifted these two overlays from Fannie Mae’s automated underwriting system, the Desktop Underwriter, allowing for the delivery of more high-DTI loans. This change was made in conjunction with other enhancements to the Desktop Underwriter’s risk assessment criteria, which Fannie Mae had stated would be risk neutral.

The increase in high-DTI loans since Fannie Mae’s change has been substantial. Before it went into effect, the share of Fannie Mae’s monthly issuances (which lag originations by about two months) with DTI ratios above 45 percent was consistently 6 or 7 percent.

By September, this share had increased to nearly 8 percent. By February 2018, it had nearly tripled to around 20 percent.

From January to July 2017, Fannie purchased 80,467 loans with DTI ratios between 45 and 50 percent. But from August 2017 to February 2018, Fannie purchased 181,911 loans in the same DTI bucket.

This increase of more than 100,000 loans in just seven months exceeded our estimate (85,000 additional Fannie loans annually) and Fannie’s expectations. Freddie Mac also saw an increase in its volume of loans with DTI ratios between 45 and 50 percent, from about 41,000 to 63,000 loans, as some Freddie loans are run through the Desktop Underwriter.

Transparency was missing

While we applaud Fannie Mae’s decision to expand the credit box, this rollout needed greater transparency. The industry had expected that the two overlays—12 months of reserves and LTV ratios of 80 percent or below—would be replaced by other compensating factors, such as a higher credit score requirement. But few compensating factors were added, which meant Fannie was tolerating a higher probability of default in this bucket than was expected by the market, with no notice. Much of this added risk for high-LTV mortgages fell on PMIs because they are in the first-loss position.

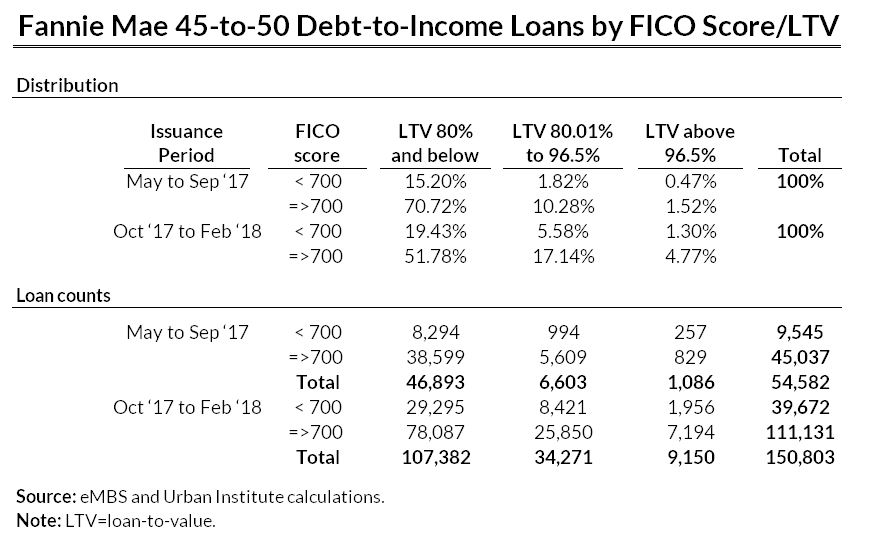

The table below shows the distribution by FICO score and LTV ratio of Fannie Mae loans with DTI ratios between 45 and 50 percent before and after the change. It shows a significant increase in the volume of loans with LTV ratios above 80 percent, for which the PMIs are on the hook (although the largest increase was driven by loans with LTV ratios of 80 percent or below). Many borrowers with LTV ratios above 80 percent, FICO scores below 700, and DTI ratios above 45 percent would find the Federal Housing Administration more economical because it does not base its prices on risk.

After several PMIs announced they were tightening their underwriting criteria or increasing their pricing, Fannie Mae fine-tuned the risk assessment criteria within the Desktop Underwriter to partially mitigate the risk of high-DTI loans, effective March 17, 2018.

We would expect PMIs to reevaluate their overlays as the new loans roll in. We also expect the number of high-DTI loans to eventually settle in at a higher volume than before the change but lower than we have today.

Why does this matter?

Mortgage credit has become remarkably tight in the postcrisis era, but loosening it without accepting more risk is not easy. In addition, guarantee fees provide most of the GSEs’ cross-subsidization: more creditworthy borrowers subsidize less creditworthy ones. So tinkering with these fees (or with loan-level pricing adjustments) is neither economically nor politically straightforward.

As private entities that employ pure risk-based pricing, the PMIs have more pricing flexibility than the government-sponsored enterprises. In fact, private mortgage insurance pricing does change periodically. With proper notice, the PMIs could have adjusted their pricing to reflect the increased risk. But these loans could also have simply been outside the risk spectrum some PMIs consider acceptable, which is why those PMIs applied a hard FICO score floor of 700.

Despite widespread agreement that credit is too tight, this episode reminds policymakers how well-intentioned efforts to improve credit availability can be complicated to enact and have unintended consequences. As we work to reform the housing finance system, transparency and careful analysis will be critical to our success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.