<p>A view of Amoeba Music after Los Angeles ordered the closure of all non-essential services and entertainment venues earlier this week and hours before the 'Safer at Home' emergency order was issued by authorities amid the ongoing threat of the coronavirus outbreak on March 19, 2020. (Photo by AaronP/Bauer-Griffin/GC Images)</p>

<div> </div>

Each day, major segments of the economy are shutting down or scaling back in a nationwide effort to slow transmission of the novel coronavirus. Thousands of workplaces have closed, and millions of Americans are now working from home, likely for an extended period.

But for millions of other workers, particularly those who are self-employed or paid hourly, working from home is not an option, and many will not continue to get paid as customer demand dries up, businesses close, shifts are canceled, and workers are laid off.

For instance, hourly paid employees, who make up over half of all wage and salary workers, constitute more than two-thirds (PDF) of the retail trade and leisure and hospitality workforce (PDF), which are among those hardest hit by the current economic crisis. According to one recent poll, only about one-quarter of all hourly workers can do at least part of their job from home.

New data from the December 2019 round of the Urban Institute’s Well-Being and Basic Needs Survey of nonelderly adults show that despite the nation being at the tail end of its longest economic expansion on record, many hourly and self-employed workers were already struggling to make ends meet before the outbreak.

What the data show

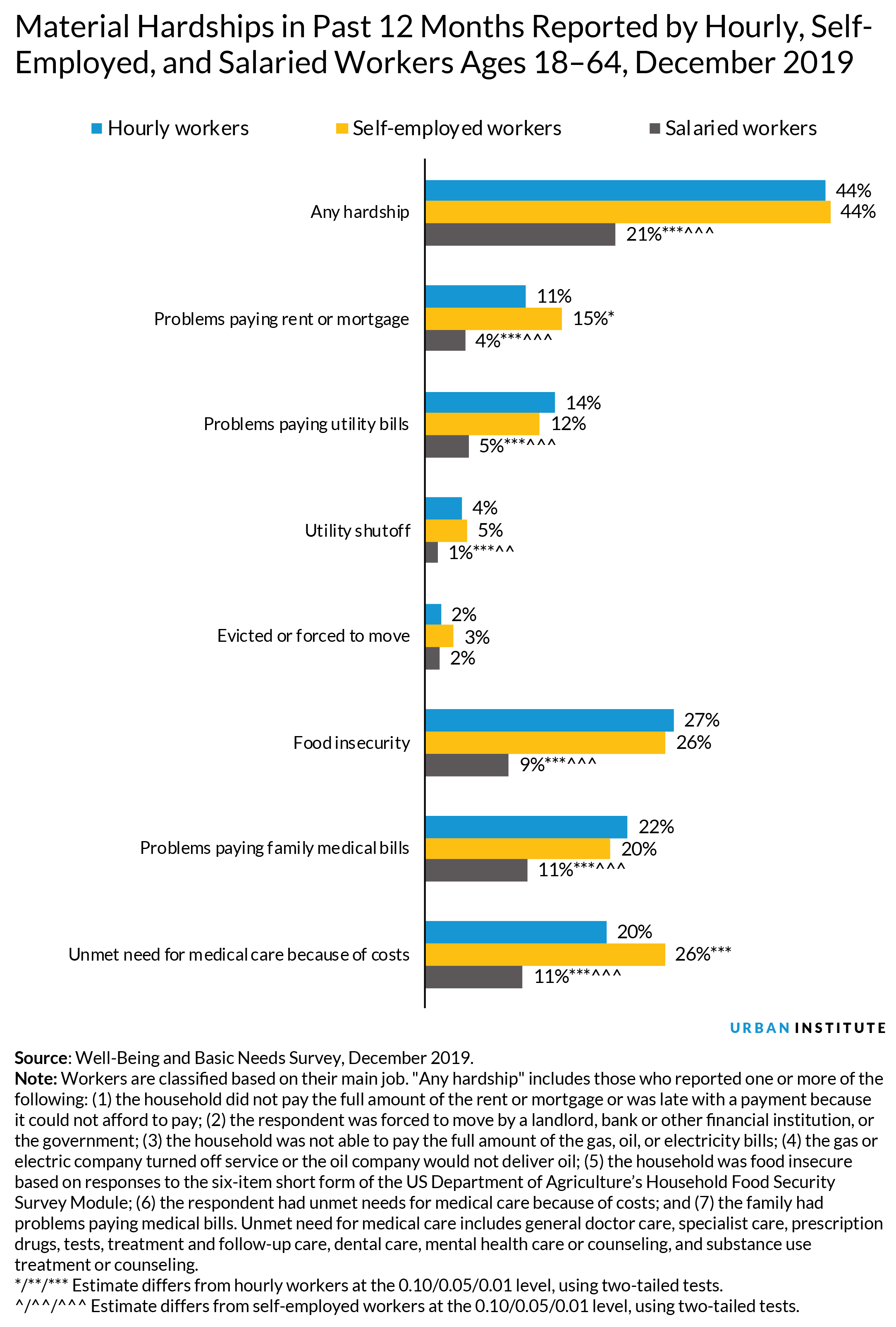

About 44 percent of both hourly and self-employed workers reported difficulty paying for basic needs such as housing, utilities, food, or medical care during 2019, more than double the share of salaried workers reporting at least one of these forms of material hardship during the same period.

This includes more than one-quarter of hourly workers (27 percent) and self-employed workers (26 percent) who reported household food insecurity, compared with 9 percent of salaried workers.

Hourly and self-employed workers were each more than twice as likely as salaried workers to have had difficulty paying their rent or mortgage or utility bills, and they were more likely to have had problems paying medical bills or to have gone without medical care because of its cost.

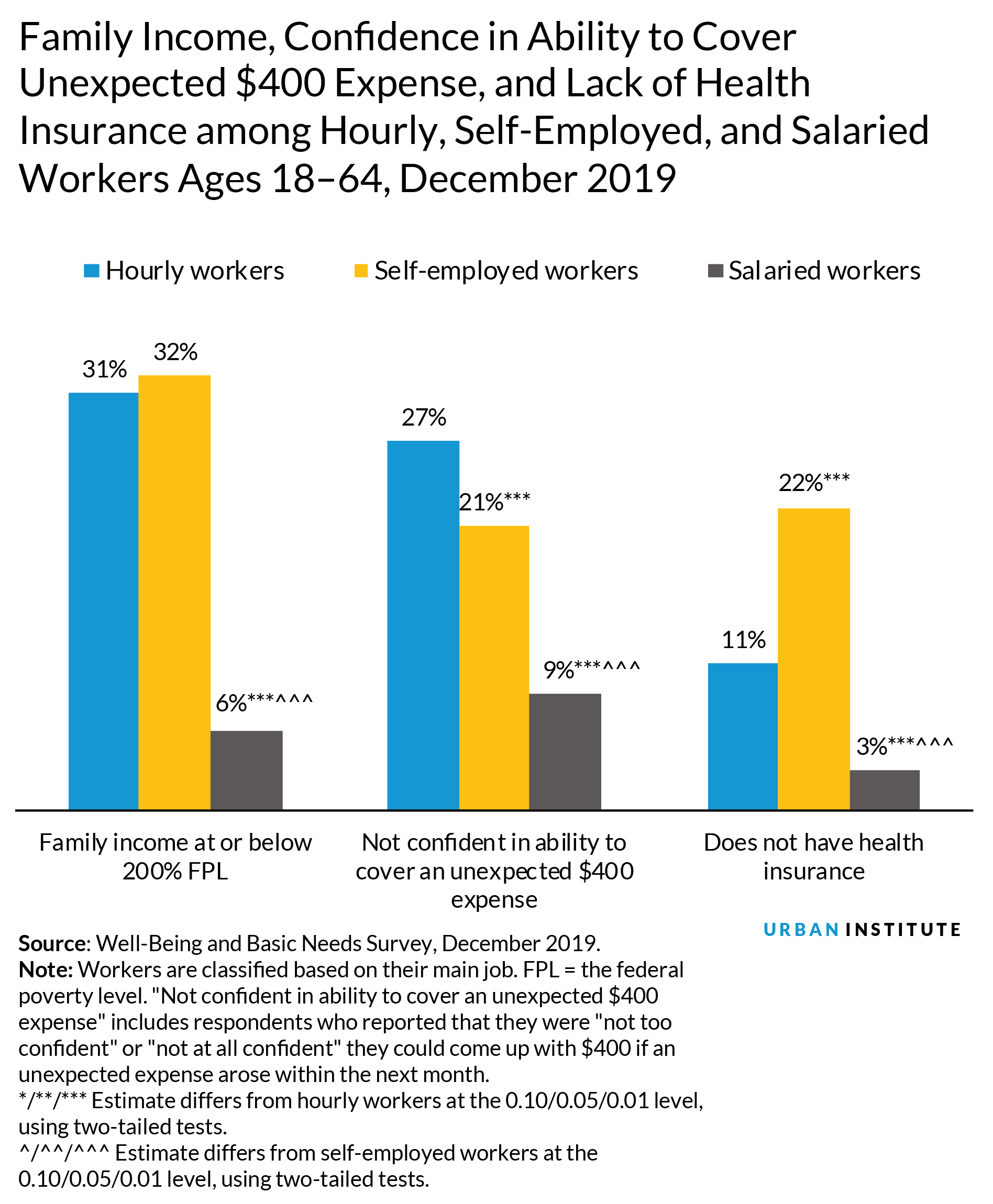

The high levels of material hardship among hourly and self-employed workers reflect their precarious financial situations and limited protection in an emergency. Nearly one-third of hourly and self-employed workers had family incomes below twice the federal poverty level or about $25,000 for a single adult and just over $50,000 for a family of four in 2019. Only about 6 percent of salaried workers had incomes that low.

There were also significant disparities in the ability of different groups of workers to draw on savings or other resources to cover unexpected expenses. Over one-quarter of hourly workers and about 21 percent of self-employed workers were not too confident or not at all confident they could come up with $400 if an unexpected expense arose within the next month, compared with less than 10 percent of salaried workers.

Hourly and self-employed workers were also less likely to be protected against high medical bills, with 11 percent of hourly workers and 22 percent of the self-employed lacking health insurance (compared with only 3 percent of salaried workers), which could discourage them from seeking preventive care and other medical treatment.

If the loss of income during the coronavirus outbreak leads to increased material hardship among workers, it could have both immediate and long-lasting effects on their and their families’ health and well-being, and could even exacerbate the current strain on the health care system.

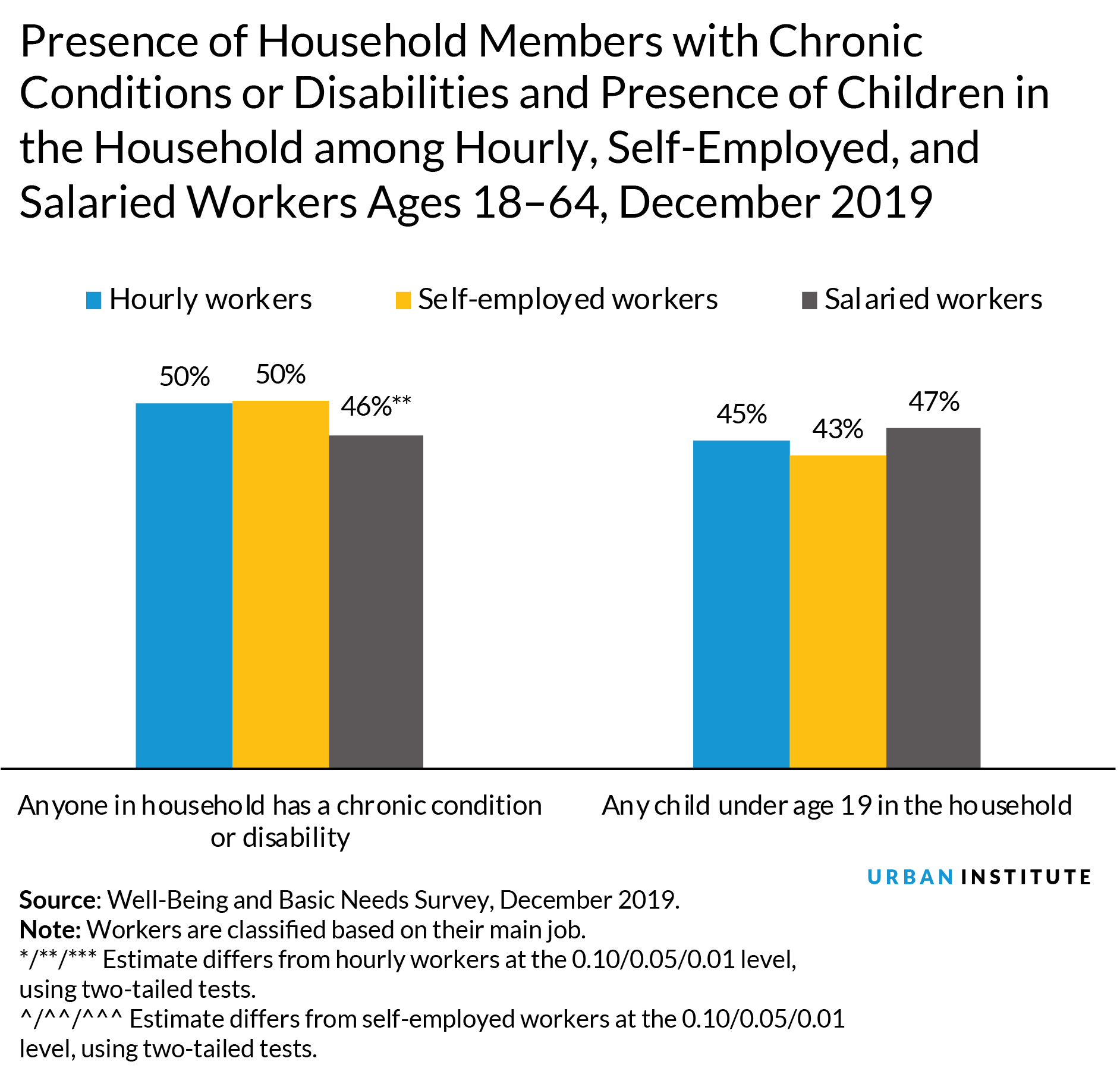

About half of hourly and self-employed workers and nearly half of salaried workers lived in households with someone who already has a chronic condition or disability. If the economic consequences of the coronavirus outbreak make it more difficult for these households to meet their basic needs, they could have more difficulty managing existing health conditions and be at greater risk of hospitalization.

The risks to children are real as well. More than 40 percent of all types of workers lived with children under age 19. Material hardship and the stress it places on families have been linked to poor long-term health and developmental outcomes for children.

What policies could help?

The many hourly and self-employed workers who were financially insecure before the economy slowed nearly to a halt could face dire consequences without strong measures to replace lost income.

But some of these workers are ineligible for unemployment insurance benefits under current rules for various reasons, such as lacking sufficient earnings in the base period for determining eligibility or because they do not have a direct relationship with an employer. These workers may not necessarily benefit from the extended unemployment insurance benefits included in the initial relief bill recently signed into law.

For those who are eligible, unemployment insurance does not replace a worker’s entire income, and there are limits on the amount a person can receive.

Other parts of the safety net may also fail to support them during a crisis. Because Medicaid eligibility is based on an applicant’s current monthly income, many workers who face a precipitous drop in earnings may become newly eligible. But other workers who experience a more modest decline in earnings may continue to earn too much to qualify for Medicaid but not enough to afford private health insurance coverage. In states that did not expand Medicaid under the Affordable Care Act, even very large reductions in earnings may not be enough to qualify for these benefits.

To ensure families can meet their basic needs, relief efforts must get money into the hands of both workers and non-workers who will not be reached by safety net and social insurance programs under existing eligibility rules and must mitigate the harm resulting from sharp declines in income. These efforts will be especially important for self-employed workers and small-business owners, who don’t have an employer that can provide additional support.

Momentum is building for a broad range of policies to achieve this objective, including federal cash payments to US households; emergency unemployment insurance; increased eligibility and benefits for safety net programs such as Medicaid and food assistance; loans to help businesses keep workers on payroll; and a moratorium on evictions, foreclosures, and utility shutoffs.

As the economy slows and more people are unable to work, these and other unconventional strategies will be critical for filling gaps in the safety net and ensuring all US residents have the means to weather the crisis.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.