The COVID-19 pandemic has disproportionately affected Native American, Alaska Native, and Native Hawaiian homeowners. According to the US Census Bureau, there are 2.1 million Native households in the United States. Of these, around 1.1 million, or 53 percent, are homeowners. (This category includes American Indians, Alaska Natives, and Native Hawaiians alone or in combination with one or more races.) Centuries of systemic racism, disinvestment, displacement, and resource extraction have limited capital in their communities.

As a result, Native households—both those who live on tribal land and off—experienced disparate economic hardships long before the COVID-19 crisis, and evidence suggests the pandemic’s economic impact may be more acute for Native homeowners. For example, Native homeowners have faced higher unemployment rates during the COVID-19 shutdowns and have had trouble accessing pandemic-related federal assistance.

The American Rescue Plan Act allotted $10 billion for a Homeowner Assistance Fund (HAF) to further support the recovery of homeowners with low incomes and homeowners who historically have faced barriers to homeownership. HAF includes allocations specifically for distribution by tribes and tribal leaders.

This assistance is critical but is not a one-shot solution for Native homeowners. To ensure Native communities can keep their homes, both on tribal land and off, HAF distribution efforts should center the needs and voices of Native homeowners.

Federal pandemic relief has helped but isn’t enough to guarantee Native homeowners can keep their homes

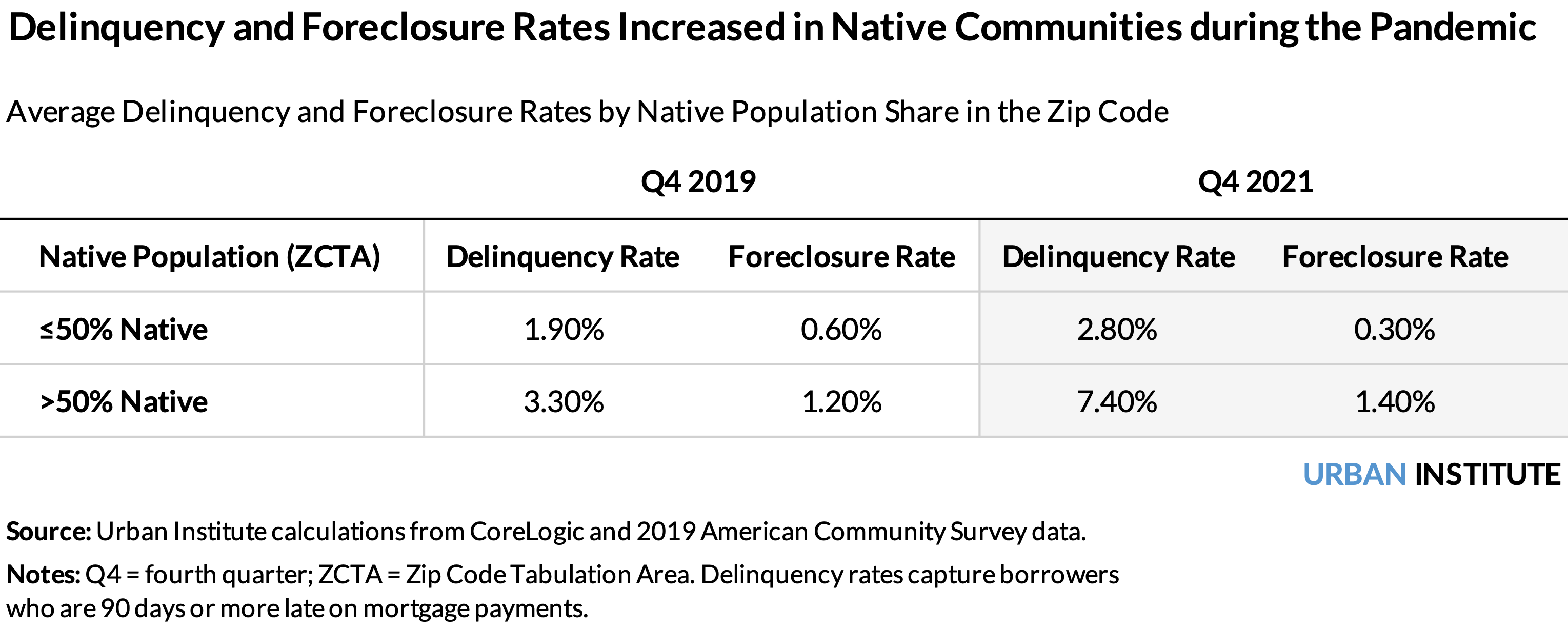

Data show the adverse effects the pandemic has had on Native homeowners. In the fourth quarter (Q4) of 2021, homeowners in zip codes with majority-Native populations were more likely to be 90 or more days delinquent or in foreclosure than other areas. The foreclosure rate increase in Q4 2021 coincides with the end of the federal foreclosure moratorium. Of the 197 majority-Native zip codes, 196 overlap at least partially with tribal areas defined by the US Census Bureau.

To help struggling homeowners during the pandemic, policymakers passed forbearance options for federally backed loans, including the US Department of Housing and Urban Development’s Section 184 Indian Home Loan Guarantee Program.

Section 184 is tailored to Native communities and, as of December 2021, guarantees $3.9 billion in mortgage debt outstanding. These loans are available for homes in approved operating areas encompassing 23 states and select counties in 12 states. The program covers various land types, including all tribal trust land, where 22 percent of all Native households live.

Today, more than 90 percent of Section 184 mortgage volume is outside of trust land where local foreclosure laws apply to Native owners.

Data on loans under the Section 184 program provides a proxy for the experiences of Native homeowners with mortgages. During the pandemic, Section 184 loans have been delinquent just as often as loans from other federal programs, but their share of delinquent loans that have entered forbearance is much smaller; 38 percentage points less than mortgages in the Federal Housing Administration program in June 2020 and 12 percentage points less as of December 2021, according to loan-level data from servicers.

This difference in the take-up of federal forbearance relief may explain why the foreclosure rate in majority-Native communities is higher than the national average. Though COVID-19 forbearance plans are winding down for all federal programs, borrowers who had forbearance are better positioned to get back on track with missed payments—lacking forbearance puts borrowers at risk of quicker foreclosure action.

With policy protections waning, the foreclosure rate among Native homeowners with mortgages could surge, particularly for owners living outside trust lands. Amid elevated housing equity positions, homeowners may not lose their home to foreclosure, but they may be forced to sell their home.

The Homeowner Assistance Fund offers promising relief

States are beginning to distribute funds from HAF to offer financial relief for qualifying homeowners. To serve Native communities, $482 million of HAF’s total funds are allocated for distribution by tribes and tribal entities.

But HAF allocations account for only one-third of the increase in past-due homeowner costs (principal, interest, tax, and insurance payments) during the pandemic. Considering Native communities face disproportionate housing risk and have had prior difficulties receiving pandemic-related federal assistance, states can take the following steps to maximize HAF’s benefit to Native populations:

- Include Native homeowners in state distribution plans

With Native homeowners facing greater risk than the average homeowner, the $482 million special allocation to tribes may fall short of what is needed. States can leverage general HAF money to cover potential shortcomings and, in doing so, adhere to HAF regulations, which prioritize historically disadvantaged groups.

States should consider engaging tribal leaders and housing entities throughout HAF distribution efforts to monitor whether need is being met. In addition, by including Native homeowners in their strategic plans, which should be grounded in data, states can create informed strategies for reaching Native homeowners. - Offer technical assistance and knowledge sharing

Distributing HAF dollars will require the infrastructure development from the ground up, including streamlined communication with homeowners, marketing, and standardized templates and data for mortgage services.

Building the necessary infrastructure presents a unique challenge to tribes, in part because tribal communities tend to be remote. States should consider contributing resources and technology through technical assistance to help tribal leaders and entities with distribution efforts.

States have an opportunity to ensure aid reaches communities who need it most. Strategies that center the needs and voices of tribal communities will enable Native communities to keep their homes, build wealth, and maintain economic security.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Show your support for research and data that ignite change.