<p>Matthew and Caitlin Edwards with Wyatt, 5, on the front steps of their home. Photo by John Tlumacki/The Boston Globe via Getty Images</p>

You may have heard that the share of first-time homebuyers has declined in recent years. That’s true if you’re looking just at the housing market since 2008, but you have to look behind the numbers and at a longer time frame to see that first-timers have fared well recently compared with repeat homebuyers who have truly stalled.

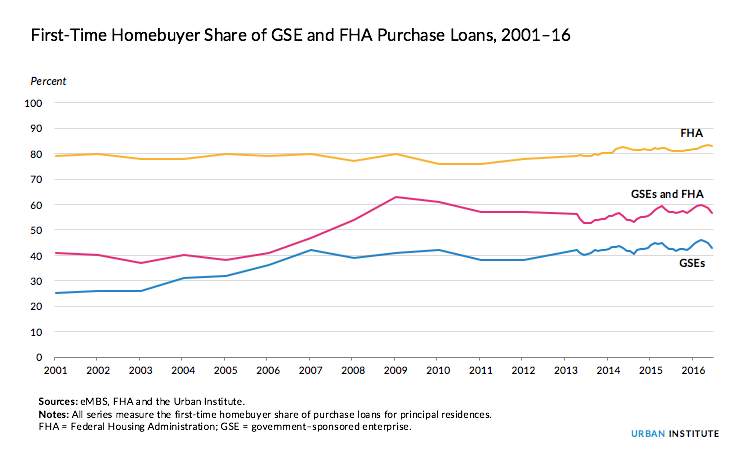

The first-timers’ share of all government-sponsored enterprise (GSE) and Federal Housing Administration (FHA) loans declined from 59 to 57 percent between January and June 2016, and the share hasn’t been above 60 percent since hitting highs of 62 and 63 percent in 2009 and 2010.

In the past decade, however, first-timers have been doing well. They have consistently represented at least 53 percent of the market since 2008 compared with less than 48 percent between 2001 and 2007.

What’s changed is the presence of repeat homebuyers in the market, the families who have lived in their starter home or their second or third home for a few years and are ready to buy a different, usually larger/more expensive home as a result of their increased equity and higher earning power.

In 2001, there were 1.8 million repeat homebuyers in the market, and while their numbers declined until 2008, there were always at least one million each year. In 2009, there were just under 700,000 repeat homebuyers. By 2015, this number had recovered to just over 900,000 but this is still half the number from 2001.

What’s happened to the number of first-timers in that same period? There were 1.3 million in 2001 and 1.3 million in 2015. There has been some variation throughout the 14 years, but much less volatility than for repeat homebuyers.

Why is it so hard for repeat homebuyers today?

All borrowers have faced a tighter credit environment since 2007 and home prices that have still not recovered to pre-crisis levels. Have these conditions impacted first-timers and repeat homebuyers differently? Maybe so.

The basic strategy for buying a starter home is to establish a strong credit history, have stable income, and save enough money for a down payment on what is often a more inexpensive home. The tight credit environment makes qualifying for the loan trickier, but for a buyer with reliable employment, saving for the smaller down payment a starter home requires remains feasible, and lower home prices have reduced the amount needed.

The basic strategy for moving up from a starter home to a bigger home, however, has been to accumulate equity in the home through consistent price appreciation, and convert that equity into the down payment for a more expensive home. Traditionally, borrowers could afford the higher payments on the larger mortgage because their incomes were rising. But falling home prices during the financial crisis have eroded this equity, and most homes are worth less than their 2007 peak: Home values nationwide must still increase by 6.5 percent to reach peak values. Real incomes have been flat since the mid-1990s, and credit standards are tight, further limiting trade-up activity.

So the next time you hear that first-time homebuyers have it hard these days, you’ll know better. First-time homebuyers represent a higher percentage of the market than they did before the financial crises. It’s the homebuyers who bought before the boom and hoped to cash in on price appreciation to trade up to their dream home who are struggling these days. While their numbers are rising, we do appear to have a generation stuck in their starter homes.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.