<p>Photo by Monkey Business Images via Shutterstock.</p>

The title of this post was edited to clarify the myth about small-dollar mortgages. The original title was “Debunking the Myth That Small-Dollar Mortgages are Riskier.” (Corrected 6/28/2019).

The difficulty of obtaining mortgages for low-cost homes has made homeownership even harder at the most affordable end of the spectrum. Only one in four homes purchased for $70,000 or less in 2015 was financed with a mortgage, compared with almost 80 percent of homes worth between $70,000 and $150,000.

There are many reasons why it’s harder to get a mortgage for the more than 600,000 homes for sale nationwide at or below $70,000, but one common reason mentioned is that small-dollar mortgage loans are riskier because the potential buyers of these homes have worse credit profiles and the loans don’t perform as well.

We recently took a closer look at the data and debunked this myth. The data show that small-dollar mortgage borrowers have comparable credit profiles to borrowers of midsize mortgages and that the loans perform similarly.

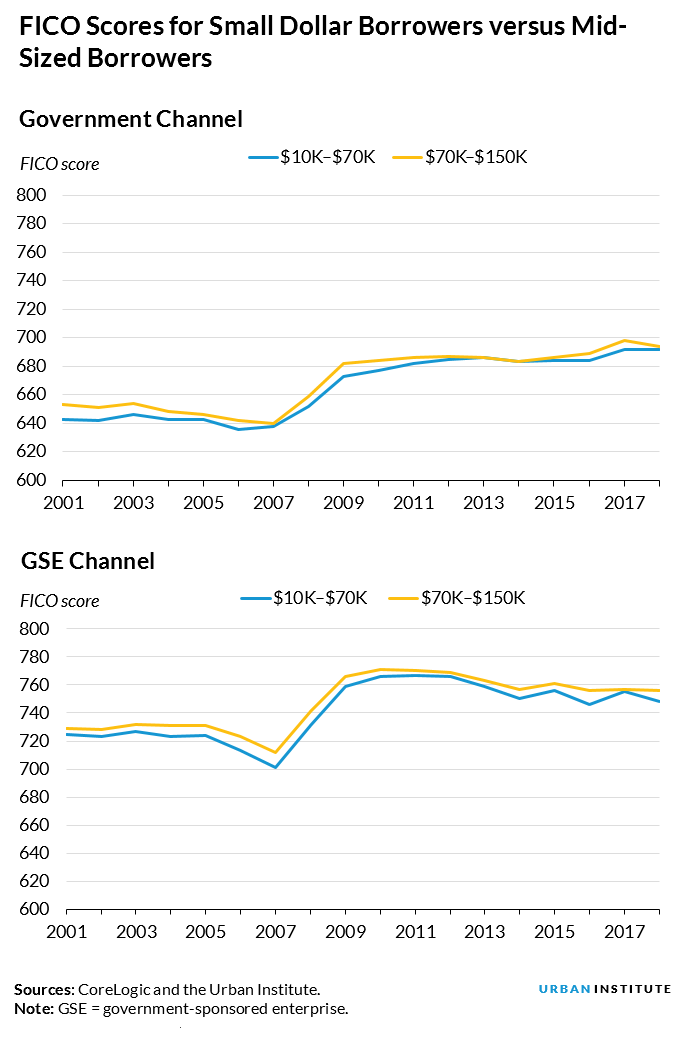

Small-dollar borrowers have comparable credit profiles

Although fewer small-dollar mortgages are originated each year, those who have been able to get one of these loans have comparable credit profiles to those who obtain midsize mortgages across the government, portfolio, government-sponsored enterprise (GSE), and private-label security (PLS) channels. Within the GSE and government-insured loan channels, for example, the FICO scores of small and midsized loan borrowers have consistently been within 10 points of each other for the past 17 years.

The loan-to-value (LTV) ratios are comparable as well, and debt-to-income (DTI) ratios are actually about 3 to 4 percentage points lower for small-dollar mortgage borrowers across all channels, likely because of lower monthly payments from lower loan balances.

Small-dollar loans also perform similarly to loans with higher balances

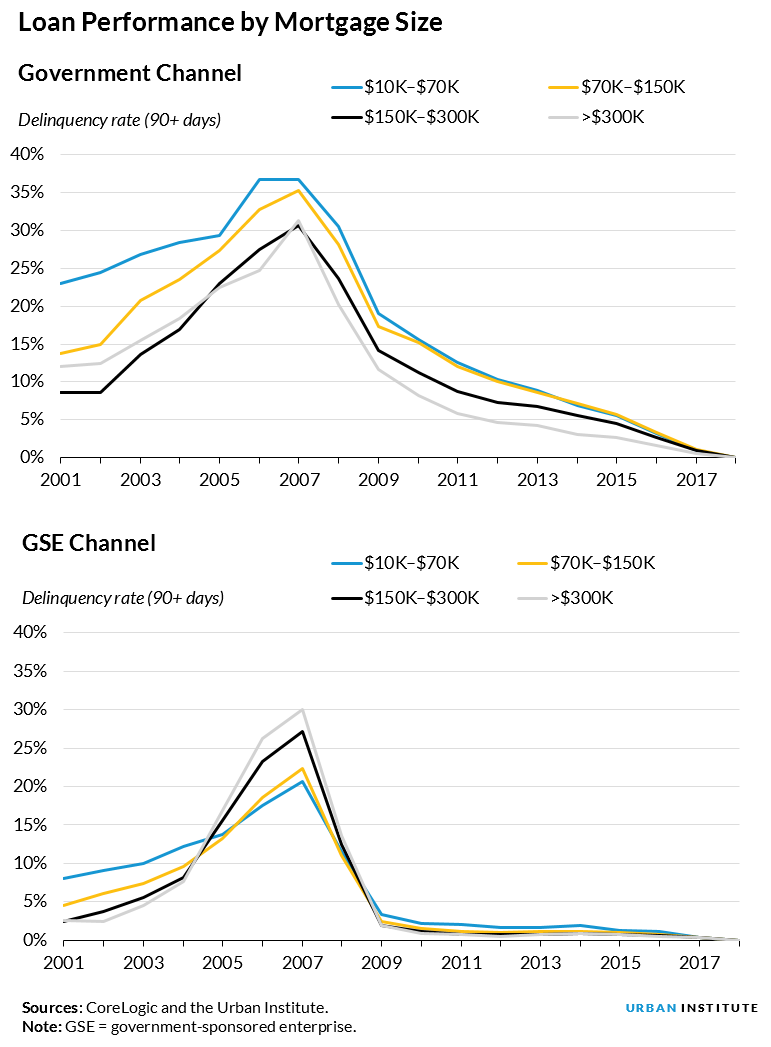

In general and through time, small-dollar mortgage loans perform similarly to loans with higher balances. Part of the relatively small difference in performance can be explained by the similarly small differences in credit scores, DTI ratios, and LTV ratios discussed above.

For example, in the government channel, during the precrisis period, small-dollar mortgages had noticeably higher default rates, and borrowers of those loans had lower credit scores. When the credit score gap narrowed following the crisis, the default rate gap also narrowed.

In contrast, in the GSE and portfolio channels, small-dollar mortgages have consistently lower credit scores, but they performed close to, and in some cases better than, their larger loan counterparts during the housing boom years leading up to the crisis. For example, for 2006 origination cohorts, the default rates were 17.5 percent for loans up to $70,000 and 18.6 percent for loans between $70,000 and $150,000.

Our analysis shows that borrowers of small-dollar mortgages pose relatively the same risk as those with midsize mortgages and that these loans perform similarly.

We hope that by debunking the myth of the riskiness of small-dollar mortgages, steps can be taken to improve the availability and viability of financial products and that improvements can be made to mortgage lending for low-cost properties to help potential low- and moderate-income households in markets across America become homeowners.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.