Low interest rates are good for those seeking credit, right? In principle, the Fed’s resolve to stay its course in promoting economic recovery over the next several years should help the unbanked and underbanked population. In fact, interest rates in mainstream financial markets mean little to those who access financial services—for credit, savings, and payments—through nonbank institutions such as payday lenders, pawnshops, rent-to-own stores, refund anticipation lenders, auto-title lenders, check cashers, and the like. These alternative providers market their services to low- and –moderate income (LMI) consumers, who can ill-afford the high associated fees and charges.

Just how prevalent is the use of non-bank credit products? Looking especially at state differences in product use, we tabulated data from the Current Population Survey (CPS) January 2009 supplement on the unbanked and underbanked. This FDIC-sponsored and Census-administered questionnaire was completed by about 54,000 households nationally, roughly one year after the Great Recession began. The survey asked “whether you or anyone in your household have . . .”:

- used payday loan or payday advance services (ever);

- sold items at a pawnshop (ever);

- rented or leased anything from a rent-to-own store (ever); or

- taken out a tax refund anticipation loan (in the past five years).

Those who said yes to one or more of these credit sources we classified as alternative credit users.

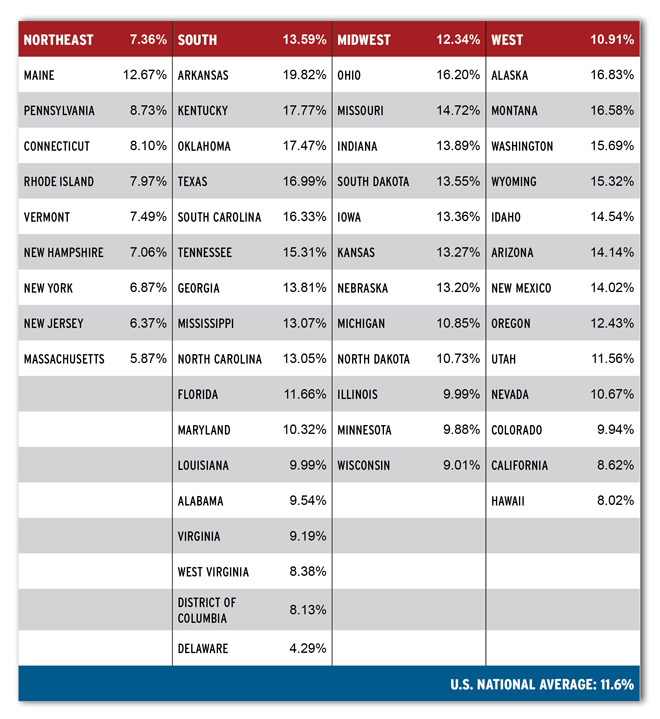

The findings? Among households nationally, the average rate of alternative credit use was 11.6 percent, with multi-fold differences among states reflecting variations in supply and demand factors. By Census region, the highest rate of use was in the South (13.6 percent), followed by the Midwest (12.3 percent), West (10.9 percent), and Northeast (7.4 percent). The rate of use exceeded 12 percent in eight states, five of them in the South. Arkansas topped the list (19.8 percent) followed by Kentucky, Oklahoma, Texas, Alaska, Montana and South Carolina (ranging between 17.8 and 16.3 percent). At the other extreme, usage rates were under 8 percent in seven states, all but one in the Northeast. Delaware came in at only 4.3 percent, followed by Massachusetts, New Jersey, New York, New Hampshire, Vermont, and Rhode Island (ranging between 5.9 and 8.0 percent).

Rate of Alternative Credit Use, by Region and State (% of Households)

You’d hope that historically low interest rates would open the door somewhat wider to mainstream credit products for the LMI market segment (those below 200 percent of the poverty level). To the contrary, lenders are now requiring higher down payments and are imposing tighter underwriting standards (e.g., credit scores and debt-to-income ratios), even for their more credit-worthy customers. This will continue to force the LMI borrowers to rely on alternative high-cost loan products, which may become even more costly as regulatory actions (such as the curtailment of refund anticipation loans) limit the products available to the already underserved market.

To promote a broad-based consumer-led recovery, policies aimed at making low-interest credit available will need to improve credit access across income levels and geographic regions. One indicator of success will be diminished reliance of the unbanked and underbanked on high-cost alternative credit sources. This will bear watching as the economy struggles to gain traction over the coming years.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.