Black Americans have struggled to build housing wealth for decades, with Black households accounting for 12.1 percent of all US households but holding only 5.5 percent of primary-residence housing wealth in 2019. Redlining, persistent racial segregation, and systemic discrimination have locked this racial wealth gap into the housing market.

Designed to combat the lasting effects of redlining, the Community Reinvestment Act (CRA) gives low- and moderate-income (LMI) borrowers and borrowers in LMI neighborhoods a CRA credit for bank lending. Although the CRA has expanded credit access to underserved communities and borrowers, current regulations do not ensure equitable outcomes, particularly for Black households in underserved communities.

Our previous findings show that lending to LMI borrowers and neighborhoods is not the same as lending to borrowers of color or neighborhoods of color. In this analysis, we highlight that Black homebuyers have been significantly underserved in LMI neighborhoods across major metropolitan areas. This new analysis sheds light on the need to address race more explicitly as regulators consider revisions to the CRA regulations.

Black homebuyers are underrepresented in mortgage lending, particularly in LMI neighborhoods.

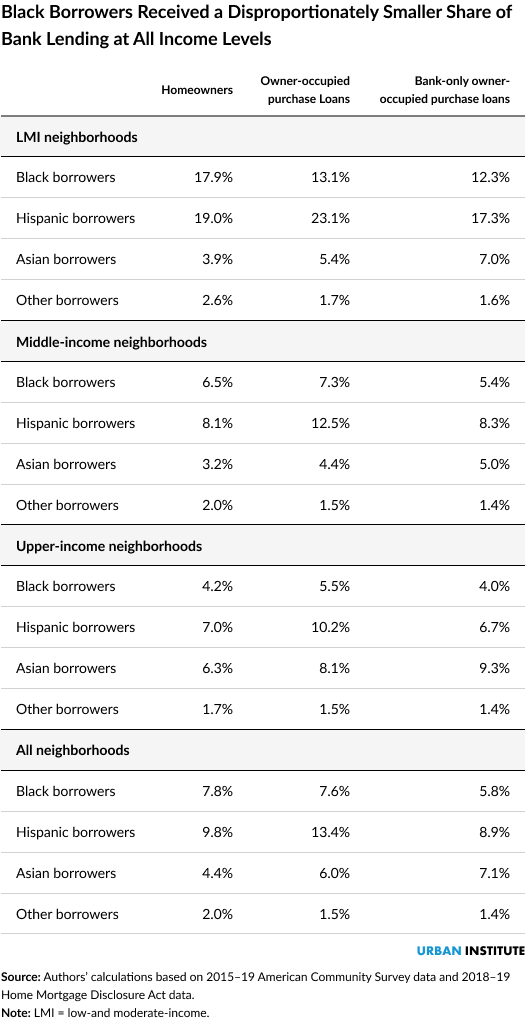

To examine how current mortgage lending serves each racial and ethnic group, we made two comparisons. First, we compared the racial composition of all 2018–19 owner-occupant purchase lending with the current homeownership rate of people of color. This comparison tells us whether each racial or ethnic group receives a share of loans in line with current homeownership rates. Because current homeownership rates by race and ethnicity bake in systemic discrimination and historic redlining, they should be understood as a baseline estimate of mortgage lending need. Increasing the Black homeownership rate will require lending to Black homebuyers beyond their current homeownership share.

Second, we compared the composition of owner-occupant purchase lending by banks, which are subject to the CRA, with lending by all institutions, including nonbanks not subject to the CRA.

Using 2018–19 Home Mortgage Disclosure Act data, we found that Black borrowers are somewhat underrepresented relative to their current homeownership rate but are particularly underserved in LMI neighborhoods.

During this period, 7.8 percent of US homeowners were Black, but Black borrowers received only 7.6 percent of all owner-occupied home purchase loans. In LMI neighborhoods, 17.9 percent of homeowners were Black, but Black homebuyers received only 13.1 percent of owner-occupied purchase loans. Bank loans to Black homebuyers during this period also composed only 12.3 percent of bank lending in LMI neighborhoods—a 5.6 percentage-point shortfall compared with already-depressed overall mortgage lending.

This shortfall continues up the income ladder. In middle-income neighborhoods, bank lending lagged the Black share of current homeowners by 1.1 percentage points. In higher-income neighborhoods, bank loans also fell short (4.0 percent versus 4.2 percent). And in all neighborhoods, Black borrowers experienced a 2 percentage-point shortfall in bank lending.

The underrepresentation of Black borrowers persists across almost all major metropolitan areas

This pattern of lending shortfalls for Black borrowers is pervasive, affecting most metro areas. For all but a few metro areas, Black borrowers in LMI neighborhoods receive less lending than the Black share of existing homeowners in these neighborhoods.

This underrepresentation of Black borrowers is particularly pronounced in metro areas with larger shares of Black homeowners. In Memphis, where Black homeowners compose 71.1 percent of current homeowners in LMI areas, Black borrowers received only 52.2 percent of owner-occupied purchase loans—a 18.9 percentage-point shortfall. We found similar patterns in New Orleans, Birmingham, and Richmond, where more than 30 percent of homeowners in LMI neighborhoods are Black.

Other racial and ethnic groups also see depressed lending rates

Turning to other racial and ethnic groups, we found divergent patterns. In contrast to Black borrowers, Hispanic and Asian borrowers received loans that exceeded their current homeownership rates across neighborhoods of all income levels. In all neighborhoods, Hispanic homeowners composed 9.8 percent of existing homeowners and received 13.4 percent of current owner-occupied purchase loans. Similarly, Asian households composed 4.4 percent of existing homeowners and received 6.0 percent of current owner-occupied purchase loans.

Hispanic and Asian borrowers receive a larger proportion of new lending in part because these demographic groups skew young and a sizeable share of households in these groups are in their prime homebuying years (ages 25 to 44). Conversely, because lending to Hispanic and Asian borrowers fell short in comparison with the homeownership rate of the 25-to-44-year-old cohort suggests that even these groups are not being fully served.

In all neighborhoods, Hispanic households composed 14.5 percent of 25-to-44-year-old homeowners but received only 13.4 percent of owner-occupied purchase loans. Asian households composed 8.9 percent of 25-to-44-year-old homeowners but received only 6.0 percent of owner-occupied purchase loans.

Considering race and ethnicity more explicitly in CRA lending could create more equitable practices

The CRA’s current focus on LMI neighborhoods and borrowers has left significant gaps in lending to neighborhoods and borrowers of color, particularly Black borrowers. As the bank regulators consider modernizing CRA regulations, our analysis suggests they should consider explicitly incorporating consideration of race into CRA lending regulations. By putting more emphasis on neighborhoods and borrowers of color, the CRA could take a step toward overcoming the long-term persistence of redlining’s effects and narrow ongoing racial homeownership gaps.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.