Medical debt is a critical challenge to Americans’ financial stability and well-being. People with medical debt are more likely to forgo needed medical care, have difficulty meeting basic needs, and face an increased risk of bankruptcy.

Recent Urban research shows there are great disparities in who carries the most medical debt. Adults who live in communities where the majority of the population are people of color are more likely to have medical debt in collections reported on their credit reports. In particular, Black adults are more likely to have difficulty paying for family medical expenses. These inequities reinforce the racial wealth gap and contribute to disparities in health outcomes.

Racial and ethnic disparities in medical debt are rooted in a legacy of discrimination

Evidence shows residential segregation of Black Americans is associated with adverse birth outcomes, decreased life expectancy, and increased risk of chronic disease. These health outcomes place Black Americans and communities of color at higher risk of incurring substantial medical expenses.

Structural barriers and systemic racism in housing, credit, and employment opportunities increase financial vulnerability among communities of color, making it more difficult for households of color to manage medical bills and pay debts on time.

Access to health insurance protects households against medical debt by making health care costs more manageable. Although the expansion of Medicaid (PDF) under the Affordable Care Act reduced disparities in health care coverage, racial and ethnic inequities in coverage and access to care persist, especially in states that have chosen not to expand Medicaid. Structural racism in the labor market also prevents people of color from obtaining jobs with employer-sponsored health insurance.

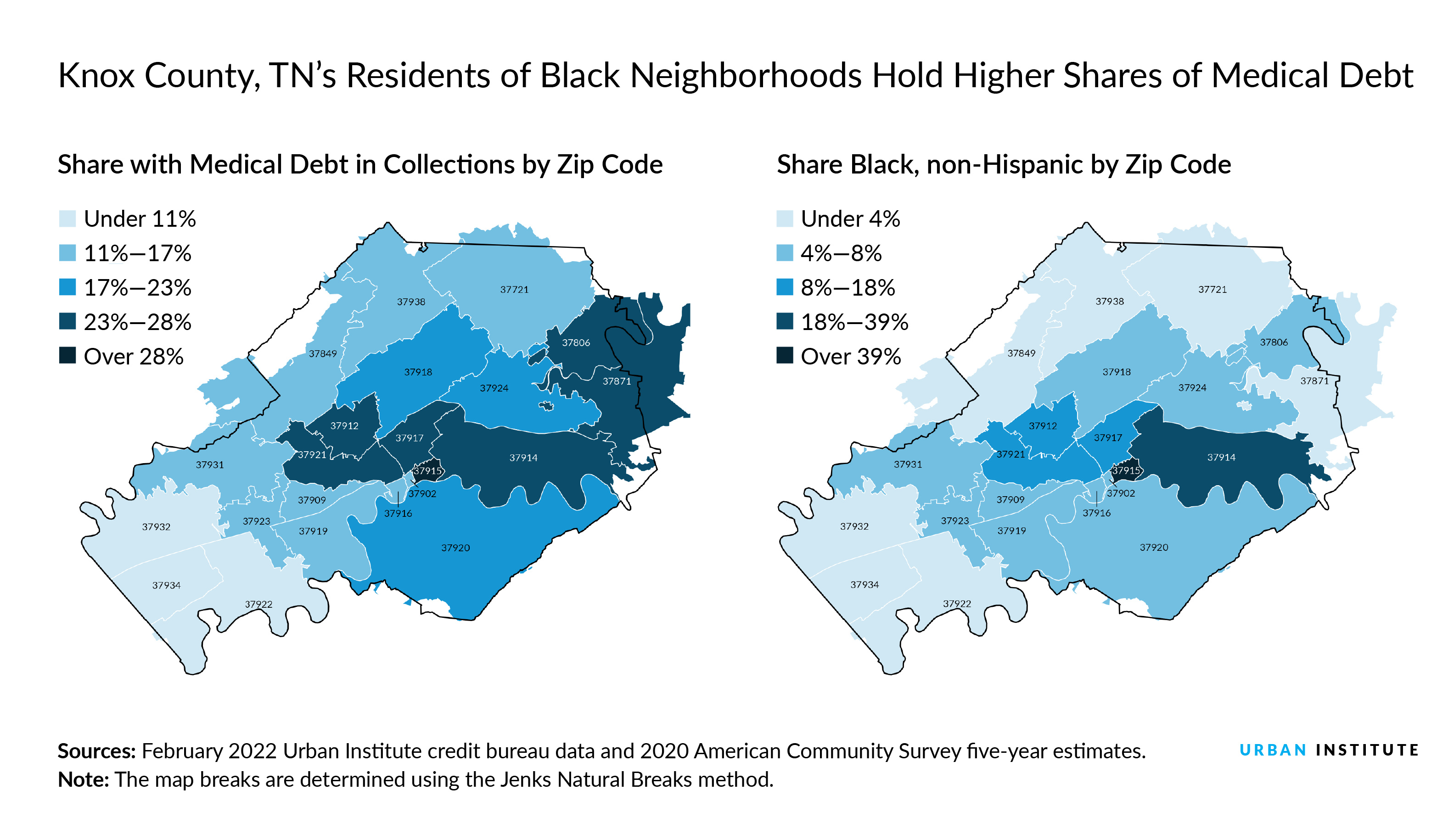

Disparities in medical debt are especially prominent in the South. To demonstrate the prevalence of these inequities, we worked with Kaiser Health News to explore the distribution of medical debt in collections within Knox County, Tennessee, which shows one of the greatest racial disparities in the US.

Only 17 percent of adults living in predominantly white communities in Knox County had medical debt in collections reported in their credit records, compared with about 40 percent of residents in communities of color. The national average for medical debt in collections is 11 percent in white communities and 15 percent in communities of color.

Out of the 18 percent of residents in Knox County who identify as people of color, Black residents comprise about 9 percent of the county population and live primarily in the central areas of the county. These areas, in and around the city of Knoxville, are also those with the highest prevalence of medical debt. In particular, the majority-Black zip code 37915 has the highest share of medical debt in collections in Knox County, the lowest insurance coverage, the lowest median income, and among the highest levels of chronic diseases.

This community was shaped by redlining and urban renewal policies that reinforced racial segregation during the 1950s and 1960s. Racial inequities in income, wealth, and access to health care—the result of these historical and structural factors—likely play a role in this zip code’s higher rates of medical debt.

Urban renewal efforts destroyed individual and community assets to build new housing projects—mostly concentrated in the 37915 zip code—and redlining prevented Black households from moving from the area. As a result, this racial segregation likely reinforced disparities in access to health care, quality of care, and other environmental factors that worsen health outcomes.

How state and local policymakers can address burdensome medical debt

To reduce racial disparities in the accumulation of medical debt, states like Tennessee could expand Medicaid eligibility (PDF) or provide supplemental financial assistance to lower the cost of purchasing health insurance. National-level estimates indicate that expanding Medicaid in all states, along with the recent extension of the enhanced Marketplace tax credits, would allow 1.2 million currently uninsured Black Americans access to health insurance coverage, reducing disparities in coverage and medical debt.

Lessons from other states with lower medical debt—such as California, Maine, and Maryland— offer strong state-level policy solutions. Common policies seen in these states include increased consumer protections that require health care providers to establish and notify patients of charity care policies and to provide accurate and itemized medical bill information.

Other policies could protect consumers from wage garnishments, home foreclosures, and other consequences of medical debt. Wage garnishments that stem from hospital lawsuits disproportionately affect Black patients, often leaving families unable to meet other basic needs, such as food, housing, and continued health care.

In addition to states with strong policies, the White House has recently announced action to lessen the burden of medical debt for American households. These actions show promising opportunities to address the prevalence of medical debt and improve financial well-being among households of color.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.