Cash-out refinances were one of the main contributors to the financial crisis. These loans increased from 21 percent of total loan production in 2001 to 46 percent by the third quarter of 2015, and they performed worse and had greater losses than purchase loans and rate refinances, even when controlling for credit characteristics.

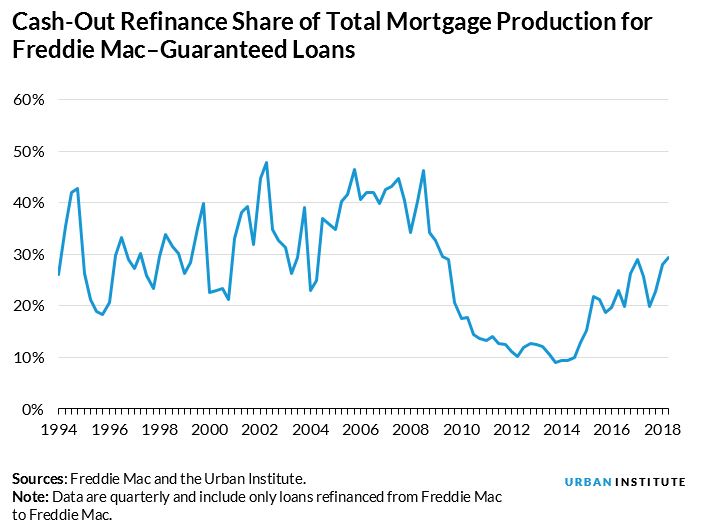

Freddie Mac publishes quarterly statistics that allow us to monitor the cash-out refinance market. In the most recent quarter, the share of refinance loans where borrowers increase their loan balance to extract equity from their home has reached the highest point since 2008 and stood at 77 percent of total refinances in the second quarter of 2018.

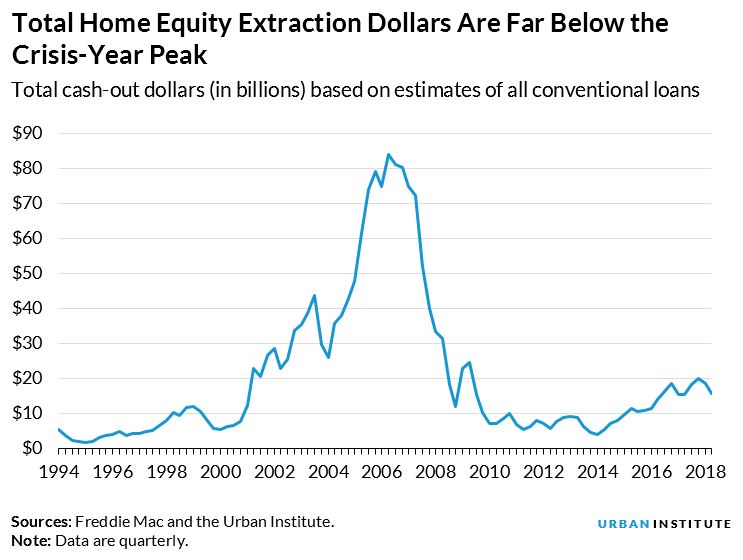

But the volume of home equity cashed out is still below the crisis peaks: home equity cashed out through the conventional channel in the second quarter totaled $15.8 billion, far below the dangerous highs between $75 and $85 billion in the precrisis years.

Moreover, the growing share of cash-out refinances is expected when you consider the current fundamentals of the mortgage market.

Here are three reasons the growing share is no reason for concern.

1. The cash-out refinance share is strongly correlated with home price appreciation and rising interest rates.

Homeowners typically choose to refinance their mortgage to lower their monthly payment by obtaining a lower interest rate (a rate refinance) or to extract equity from their home (a cash-out refinance).

The current environment—rising interest rates and strong home price appreciation—is driving the higher cash-out refinance share. Home price appreciation has been robust over the past few years, averaging between 6 and 8 percent. When homes are increasing in value, borrowers have an incentive to refinance their loans and tap into their mounting equity.

Furthermore, interest rates are on the rise, recently hitting an eight-year high, so a growing portion of currently outstanding mortgages have interest rates already below the current mortgage rate. Most borrowers cannot refinance their loans at a lower interest rate, meaning the predominant reason to refinance is to extract home equity.

2. The cash-out refinance share of total production is in line with historical trends.

It may seem alarming that the cash-out share of refinanced loans is as high as it was in 2008, but it is important to put this number in context.

Over the past few months, the overall refinance share of total mortgage loans has been at or near the lowest point in years, largely because rising interest rates have made rate refinances unattractive to most mortgage holders. Refinance loans make up such a small share of total loan production—currently below 30 percent for Freddie Mac—so the cash-out refinance share of all loans is still within a reasonable range and below the dangerous levels of the crisis years. When we look at the cash-out refinance share of all loans back to 1994, we find that today’s share is at or below other periods of rising interest rates and strong home price appreciation.

Cash-out refinances are just one of the ways homeowners can extract equity from their homes. Other products, such as home equity lines of credit (HELOCs), home equity conversion mortgages, and second liens allow homeowners to tap into their equity. None of these products are growing. The Federal Deposit Insurance Corporation shows outstanding HELOC volume is down 8 percent year over year; Freddie Mac data indicate that some cash-out refinance activity is actually debt consolidation.

3. Borrowers are extracting less equity than they did during the financial crisis.

During the period of runaway home price appreciation and lax lending standards that preceded the financial crisis, borrowers were extracting a larger share of their home equity through cash-out refinances than they are today. Cash-out dollars as a share of refinanced originations peaked at 31 percent in 2006, meaning borrowers were extracting a significant portion of their equity.

Today, cash-out dollars as a share of all refinanced originations is 21 percent and has averaged just below 8 percent since the crisis. Part of this reflects the fact that Fannie Mae, Freddie Mac, and the Federal Housing Administration have lowered the maximum loan-to-value ratio for cash-out refinances, reducing the amount of cash that can be extracted.

Similarly, when we look at the volume of cash-out dollars, measured from Freddie Mac data, we find that we are far below the peak of the crisis. Even though the share of cash-out refinances is high when looking at all refinances, the combination of the low refinance volume overall and the fact that borrowers are taking out less equity when they cash out means that the volume of cash-out dollars remains low.

While cash-outs make up the highest share of refinances they have since 2008, this is no reason for alarm. In an environment of home price appreciation, people commonly tap into their home equity.

Cash-out refinances allow homeowners to make home improvements, pay for educational and health care expenses, or maybe even buy the boat they’ve always wanted. Of course, prudent underwriting of the risks is always important, and current numbers indicate that cash-out underwriting is being done prudently.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.