<p>Erik Von Weber/Getty Images</p>

For borrowers with federal mortgages, the Coronavirus Aid, Relief, and Economic Security Act provided a much-needed lifeline by allowing borrowers to defer their mortgage payments (PDF) for six months, with the ability to defer another six months if needed. To take advantage of forbearance, borrowers need only attest to the fact that they have a pandemic-related financial hardship. But not all eligible borrowers have taken advantage of forbearance and have become “needlessly delinquent.”

As of September 28, the Mortgage Bankers Association reported that 6.87 percent of mortgage borrowers are in forbearance, including 4.46 percent of borrowers with Fannie Mae and Freddie Mac mortgages and 9.15 percent of borrowers with Ginnie Mae mortgages. A quarter of those borrowers are using forbearance as an insurance policy and continue to make payments. But despite this widespread pickup of the forbearance option, approximately 400,000 homeowners who became delinquent after the pandemic began have forgone forbearance and become delinquent.

These borrowers may not know they are eligible for forbearance or do know but wrongly fear having to make “double payments” when the forbearance period ends. To provide information and support to these borrowers, it is important to understand who they are.

Ginnie Mae’s monthly securities data provide information on more than 200,000 Ginnie Mae borrowers who were current in March but were at least 30 days delinquent by July. Fannie Mae and Freddie Mac do not provide equivalent data, but because the Ginnie Mae borrowers compose almost half the total needlessly delinquent borrowers, they can give us some insight. We found four key characteristics of needlessly delinquent borrowers.

1. There is no difference in borrowers’ creditworthiness.

We found virtually no difference in the credit scores of the needlessly delinquent borrowers and the 559,506 delinquent borrowers taking advantage of forbearance. Both groups had scores between 662 and 664.

2. Needlessly delinquent loans are almost equally likely to be serviced by banks and nonbanks.

The shares of needlessly delinquent loans serviced by banks and nonbanks sit at around 2 percent, with banks slightly higher and nonbanks slightly lower. In contrast, banks have a lower share of delinquent loans in forbearance than their nonbank counterparts (6.2 percent versus 3.2 percent). Some of the differential can be attributed to the securitized dataset we used. Servicers are permitted to buy delinquent loans out of a security when the loan becomes 90 days delinquent. Bank servicers find this practice beneficial, as they have the cash to do the payout, and their cost of funds is lower than the rate on the mortgage. Nonbank servicers often do not have the cash, and their cost of funds is higher than the rate on the mortgage, making the buyout less economic.

3. Needlessly delinquent mortgages are equally likely, no matter the year originated.

The share of needlessly delinquent mortgages remains constant at around 2 percent, regardless of the year the mortgage was originated (the “vintage” year). In contrast, the share of delinquent borrowers taking advantage of forbearance increases with more recently originated mortgages.

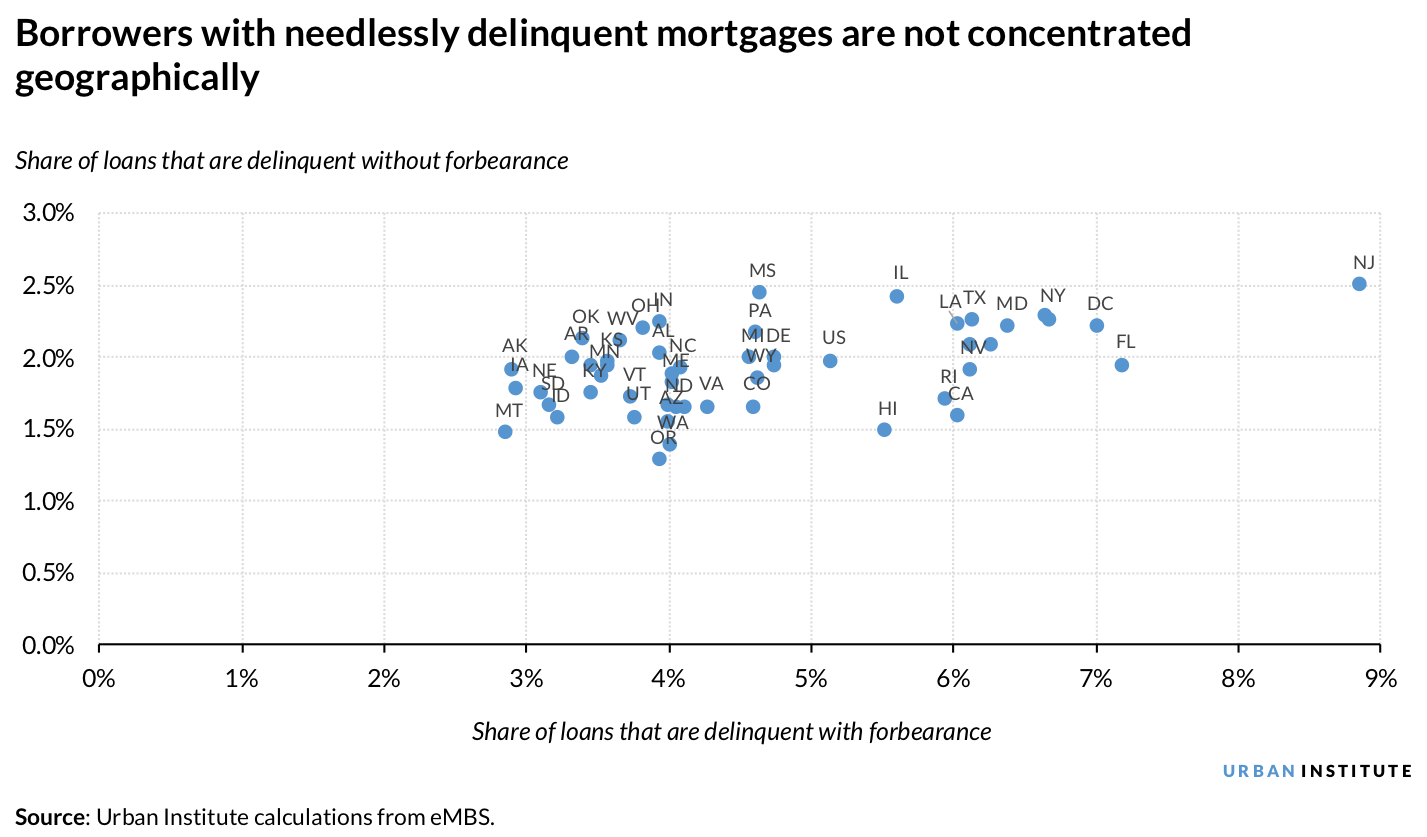

4. Needlessly delinquent loans have no strong geographic concentration.

The rate at which mortgages are delinquent and not in forbearance remains relatively constant across states at 2 percent. But the share of delinquent loans in forbearance varies widely, from a low of 2.86 percent in Montana and Arkansas to high of 8.86 percent in New Jersey.

Broad outreach is needed to support needlessly delinquent borrowers

We hoped our analysis would show needlessly delinquent borrowers are concentrated among certain servicers, in a particular geographic area, or in a particular vintage to make outreach easier, but that was not the case. Roughly 2 percent of government borrowers are needlessly delinquent across different servicer types, vintage years, and geographies, which suggests that an outreach campaign to reach these borrowers must be broad. Servicers are an important part of this outreach, but outreach efforts must also include assistance from consumer groups. Although some government messaging around forbearance options as an alternative has occurred, broader outreach may be in order.

A note on the methodology: We calculated the July delinquency rate for all loans in Ginnie Mae securities that were current in March. Specifically, the delinquency rate measures the share of loans that were current in March but delinquent in July as a share of all loans current in March. We then assessed all loans current in March, whether they were delinquent in July or not, for whether they were also in forbearance in July. Combined, this gives us both a delinquency rate across the loans current in March as well as a distinction between loans in forbearance and loans not in forbearance.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.