<p>A man takes a photo of the skyline from Telegraph Hill in San Francisco, Tuesday, June 27, 2017. Photo by Jeff Chiu/AP.</p>

The Bay Area in Northern California is a popular place to live and a difficult place to leave. So the area’s epic housing crisis—driven by a lack of supply and sustained demand in this job-rich, coastal region —will likely continue to squeeze homeowners across the income spectrum out of the market for many years to come.

The lack of affordable housing supply coupled with tight credit has kept minority and low-income people from accessing homeownership. At the same time, rising construction costs and restrictive zoning laws have constrained housing supply so much that even well-off renters can’t find a home to buy, despite being ready with a preapproved mortgage or a suitcase full of cash.

Four charts illustrate the perfect storm in the Bay Area’s housing market:

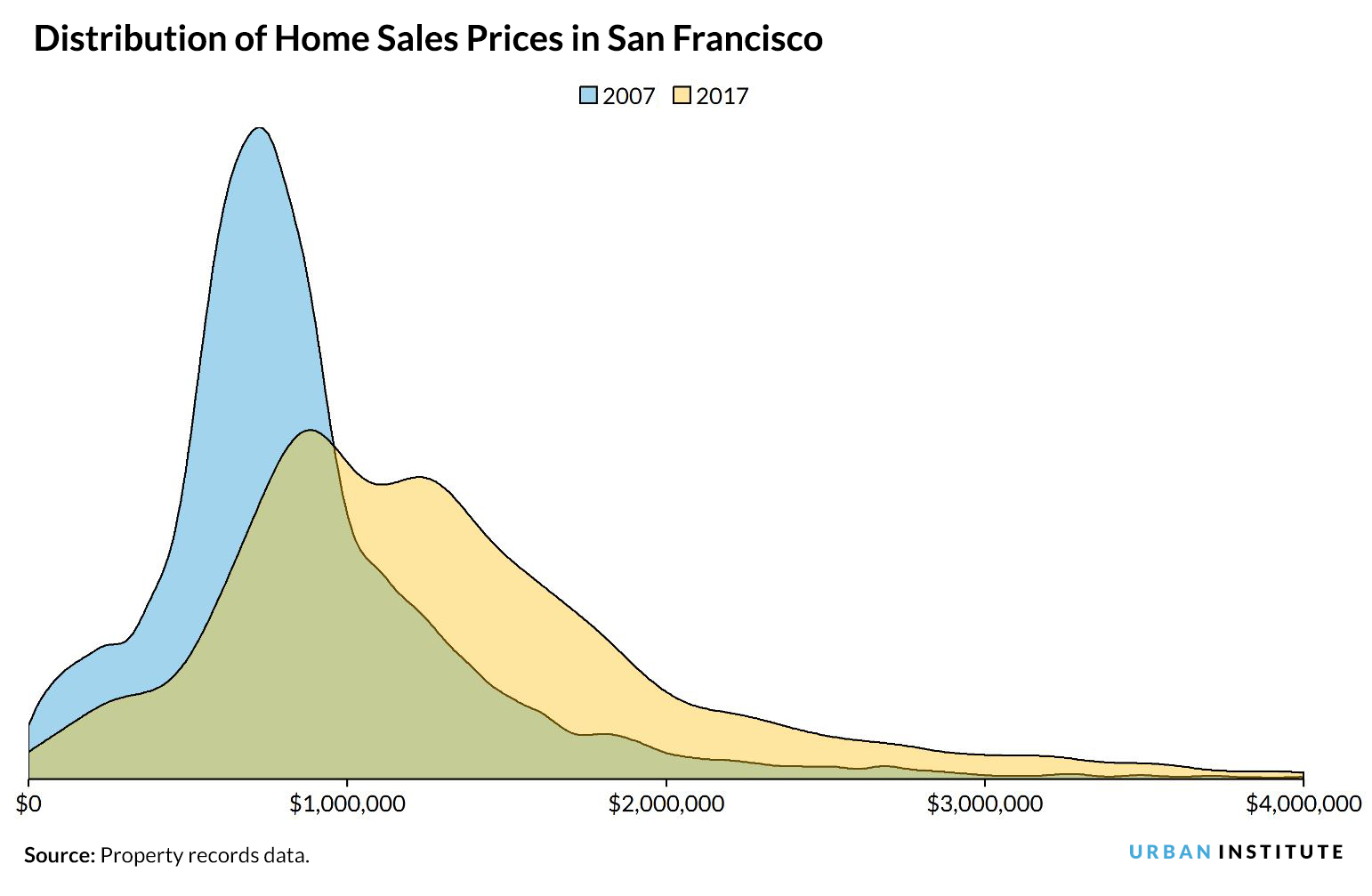

$2 million is the new $1 million.

Thanks to the Bay Area’s continued strength as a job hub and failure to build new single- or multifamily homes quickly enough to meet demand, the price of single-family homes has increased exponentially in the past decade. Ten years ago, there were many $1 million homes, but homes priced above that point were hard to find.

As this graph shows, however, between 2007 and 2017, the $1 million home has become more common, the $2 million home is no longer shocking and the $3 million home has become the next frontier.

Affordability isn’t even the biggest problem for some renters.

According to our Housing Affordability Renters Index, one in four local renters can still afford to buy a home in San Francisco. So while the cost is high, the supply problem is what stands in the way of homeownership for these renters.

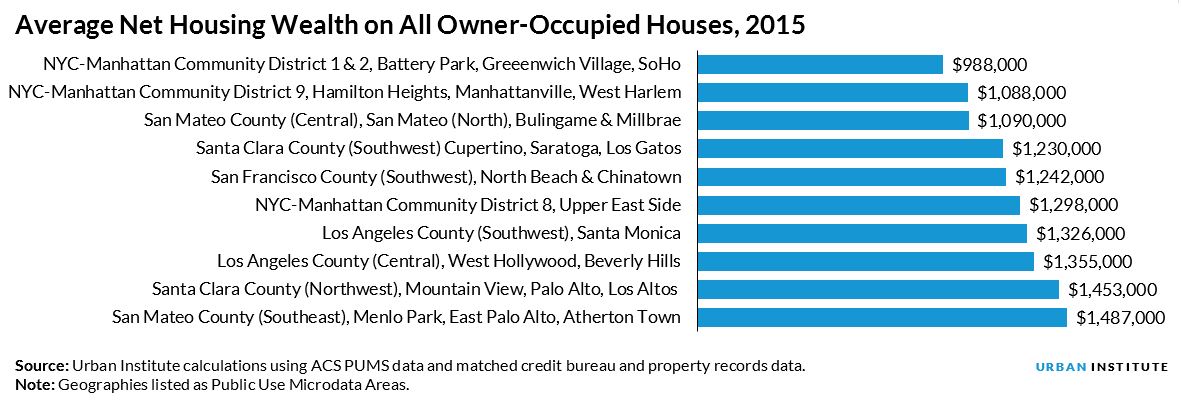

Existing homeowners are staying put as their equity builds.

For those who bought a home in the Bay Area a decade ago, it’s tempting to stay in that house, especially as home prices continue appreciating much faster than wages. Two years ago, the average San Francisco homeowner was near the top of the home equity rankings, with average home equity of $1.2 million. That’s a lot of money which has grown to even more recently and will only continue to grow. This rapid and extreme house appreciation exacerbates the supply problem for other homebuyers – restricting supply and contributing to high prices.

Minorities and low-income families are struggling to find places to live.

As the map below shows, the Bay Area’s rapid growth has left Hispanic and black borrowers behind.

The extreme competition for housing units has driven up prices and credit standards, making it difficult for low-income people to access homeownership. The current housing inventory does not meet the needs of essential members of the community, including teachers, firefighters, and police officers.

As we continue to look for solutions to the housing supply crisis, we need to ensure there are homes available on both the high end and low end of the price spectrum.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.