<p>(EyeWolf/Getty Images)<br />

</p>

The Asian American population in the US has increased significantly, from 3.6 million in 1980 to 18.8 million in 2019, and it is projected to account for 9.1 percent of the population (or 36.8 million people) by 2060. But this rapidly growing population has substantially lower homeownership rates than white Americans: 57 percent of Asian households owned homes in 2018, compared with 72 percent of non-Hispanic white households.

One contributing factor is that Asian applicants have higher mortgage denial rates than white mortgage applicants, despite having higher credit scores. In this analysis, we document this finding and shed light on the barriers Asian applicants face on their way to becoming homeowners.

Asian mortgage applicants experience higher denial rates than white applicants, despite having higher credit scores and higher incomes

Using 2019 Home Mortgage Disclosure Act (HMDA) data, we found that the denial rate for Asian mortgage applicants is 8.7 percent, compared with 6.7 percent for white mortgage applicants.

To more fully understand this pattern, we must account for underwriting variables that lenders examine when considering whether to approve a loan. A key factor is creditworthiness, as measured by credit scores. Surprisingly, the long-standing relationship between credit scores and denial rates is upended for Asian mortgage applicants. The median credit score for Asian mortgage applicants was 761 in 2020, compared with 748 for white applicants.

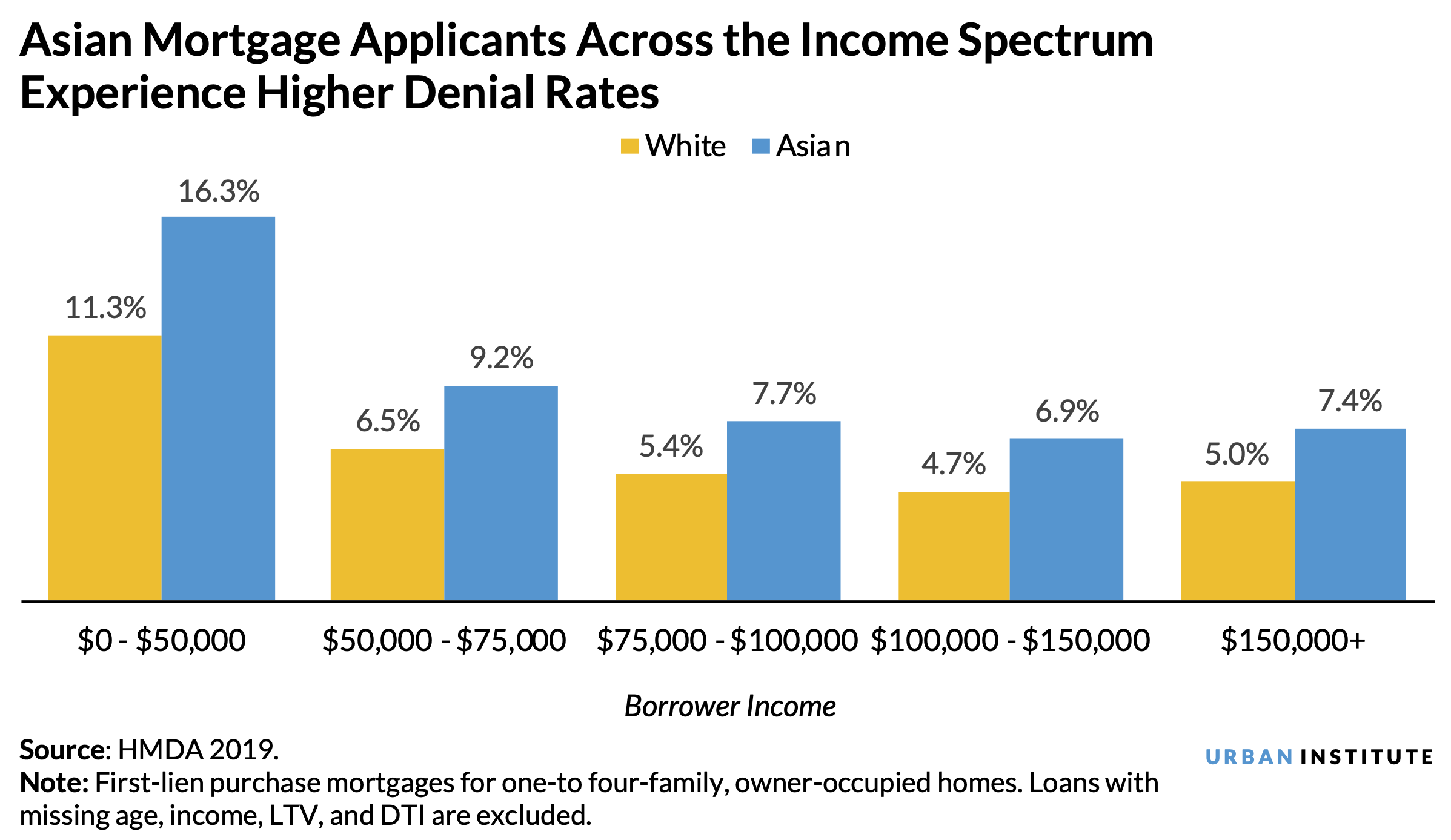

When we examine this relationship across another key underwriting factor, income, we find that Asian applicants are denied more frequently than white applicants at all income levels. In 2019, median income was $107,000 for Asian applicants and $82,000 for white applicants. For Asian applicants with annual incomes below $50,000, 16.3 percent were denied a mortgage, compared with 11.3 percent of white applicants in that income bracket. This pattern continues up the income ladder, with high-income Asian applicants being 50 percent more likely to have their mortgage application denied than white applicants.

The Asian-white denial gap exists at all debt-to-income levels

One potential reason Asian applicants have higher denial rates could be that they have more debt relative to income. In 2019, 37.2 percent of purchase loan applications from Asian borrowers were denied because of a high debt-to-income (DTI) ratio, compared with a 28.7 percent denial rate for white applicants.

But our analysis shows that even with the same level of income and DTI ratio, Asian applicants continue to receive more denials. For Asian applicants with DTI ratios below 30 percent, 11.5 percent with annual incomes below $50,000 are denied mortgages, compared with 9.2 percent of white applicants in that income bracket. This gap continues up the income spectrum, even for those earning more than $150,000 per year, and the gap widens as DTI ratio increases. For those with DTI ratios of 43 percent and above, 17.3 percent of Asian applicants and 10.7 percent of white applicants with annual incomes of more than $150,000 are denied.

We need more research on other differential borrower characteristic between Asian and white borrowers with high indebtedness to understand why the denial gap widens for applicants as DTI ratios increase.

The denial gap persists across almost all major metropolitan areas

Previous research has shown that most Asian Americans live in California, New Jersey, New York, Texas, and Washington. In metropolitan areas with large numbers of Asian mortgage applicants, we found that the denial gap persists and holds regardless of home price tier.

In expensive areas, such as San Francisco and New York City, the denial gap is around 3 percentage points, more than the national average 2 percentage-point denial gap. But we find the largest gap in areas with middle- or low-price housing markets. In San Antonio and Indianapolis, for example, the denial gap was more than 5 percentage points in 2019. This finding suggests that Asian applicants are consistently denied more frequently than white applicants, regardless of home price.

We need more research to understand the barriers leading to the higher denial rates for Asian homebuyers

This analysis highlights an important yet often overlooked barrier Asian applicants face in the housing market. More research is needed to understand why Asian homebuyers are denied mortgages more frequently than white borrowers, despite having, on average, higher credit scores and higher incomes. Failing to address this denial gap would keep more potential Asian homebuyers out of homeownership and widen the homeownership gap between Asian and white households. If additional research confirms systemic bias against Asian applicants, policymakers will need to recalibrate the underwriting system that leads to these results.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.