A number of recent media reports have speculated that young Americans will be the big losers when the Affordable Care Act goes into effect in January 2014.

This speculation stems from a provision in the health reform law specifying that insurers can charge customers age 64 and older at most three times the amount charged to 21-year-olds buying the same coverage. Today, nongroup insurers typically charge older policyholders five or more times the price quoted to younger customers.

Those concerned say the new rules will require insurers to overcharge young customers in order to subsidize coverage for their older clientele. They also say this pricing structure will drive many young adults out of the nongroup market, leaving them uninsured.

But new research from Urban Institute’s Health Policy Center, and funded by the Robert Wood Johnson Foundation, tells us that the restriction on age rating will not throw disproportionate out-of-pocket expenses on the backs of young Americans, nor will it drive them from the marketplace in droves.

Here’s why: Although insurers would charge lower average premiums for customers age 21 to 27 using a 5:1 rule (as opposed to a 3:1 rule), increased eligibility for Medicaid benefits, tax credits offered through state health insurance exchanges, and greater access to employer-sponsored plans under the ACA will protect most young adults financially.

Effects of the Affordable Care Act for Young Adults by 2017

Let’s take a closer look at what the Urban Institute’s Health Insurance Policy Simulation Model told us about the effects these rules are likely to have on young adults by 2017:

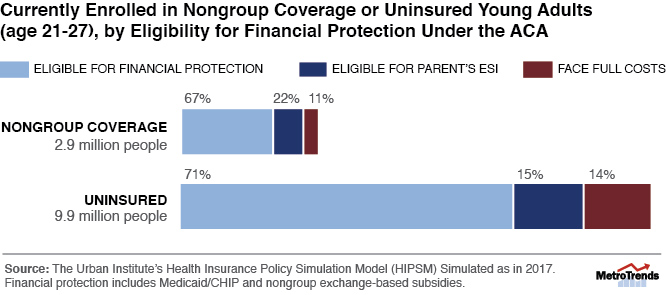

- Roughly 96 percent of the 21- to 27-year-olds who purchase single nongroup coverage from an exchange would get subsidies that keep their costs on par with a 5:1 rule.

- Two-thirds of the 2.9 million 21- to 27-year-olds currently covered by nongroup health insurance—that is, those most likely to run from higher premiums—would be eligible to receive health insurance subsidies either through the exchanges or through the expanded Medicaid program.

- Two-thirds of the remaining 1 million in that group would still be younger than 26 and in families where they would be eligible for coverage on their parents’ employer-based health insurance plans.

- Approximately 71 percent of the 9.9 million uninsured 21- to 27-year-olds would be eligible for subsidies either through the exchanges or through the expanded Medicaid program.

- An additional 15 percent of uninsured 21- to 27-year-olds would still be younger than 26 and could obtain coverage on their parents’ plan.

In addition to the provisions we factored into our model, under the law, young adults in the nongroup market will purchase higher-value insurance than many have today, with all policies covering essential health benefits. Those under 30 will also have the option of buying higher-deductible/lower-cost plans than those we analyzed.

Effects of the Affordable Care Act for Older Purchasers by 2017

Now let’s look at what our model said about the effects the rules would have on older health insurance purchasers by 2017:

- On average, premiums drop $1,770 for adults age 57 to 64, relative to a 5:1 rule.

- Approximately 86 percent of adults older than 57 who purchase single nongroup coverage from an exchange would be eligible for subsidies.

So while it’s true that the restrictions on age rating will increase the nominal costs for young adults purchasing health coverage, the actual out-of-pocket costs will not be much different on average than they would under the health reform law with a 5:1 rule.

The subsidies written into the law simultaneously protect young adults from greater personal expenses and safeguard the health insurance market from a mass exodus of young buyers. At the same time, older policyholders—those who need the most care—will be able to get it at a more affordable price.

In sum, the critics’ case has been overstated.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.