<p>Photo by By Kara Mysh/Shutterstock.</p>

The plight of the American middle class has been a central issue in recent elections. Academics have generally cited data showing middle-income families experienced virtually no growth in real incomes over the last several decades. But some analysts disagree, citing increases in observed living standards, consumption, and in incomes adjusted for taxes and transfers. The Census Bureau’s official income series shows median family incomes rose about 25 percent from 1984 to 2016.

So why the differences among researchers? Some argue that inflation is overstated, even after the Bureau of Labor Statistics (BLS) improved measurements in the Consumer Price Index (CPI). Because estimates of real income growth involve adjusting money incomes for inflation, overstating inflation means understating real incomes.

One factor generally ignored is how to account for shelter costs in estimating inflation. Researchers calculating real income growth by adjusting for CPI inflation rarely offset increases in income for homeowners. Improving these estimates could involve accounting for imputed income, or, as our research suggests, altering the shelter component of inflation for homeowners to reflect the changing costs they experience by using the housing services their home provides.

We find that altering the shelter cost calculation for homeowners makes a sizable impact on the measurement of income gains for median-income families and contradicts the narrative of stagnant growth.

Why using the CPI to adjust for inflation can be misleading

For renters, it makes sense to measure changes in shelter costs by the changes in rents they pay. For homeowners, the BLS estimates changes in owners’ housing costs as equal to changes in the home’s rental value. The rationale is that owners bear a cost equal to what they could receive if they left their home and rented it to someone else.

But, in a sense, homeowners are both owners and renters. As renters use up housing services, their costs increase. As owners, they earn imputed income (or income they have because they avoided paying that cost to someone else). So, current estimates of real income growth are misleading because analysts usually adjust homeowners’ money income for inflation in rents but ignore their offsetting increase in income.

To illustrate, instead of thinking of a homeowner as both a renter and an owner, think of two homeowner families who move and end up renting from each other. Let’s say rents increase over the next several years for both dwellings at the rate estimated by the BLS. Although shelter costs increase for both owners, income received from the other homeowner increases by the same amount, and neither owner experiences a lower standard of living.

Similarly, homeowners who rent to themselves are shielded from a decline in living standards when rents increase. Including imputed income in the shelter cost calculation is one way around this problem.

Another approach to improving shelter cost calculations

To avoid having to count imputed income or imputed rent, our shelter cost measure incorporates changes in the cost of buying the home at the beginning of the period, paying any required taxes and maintenance, and then selling it at the end of the period. This approach captures changes in living costs for homeowners directly.

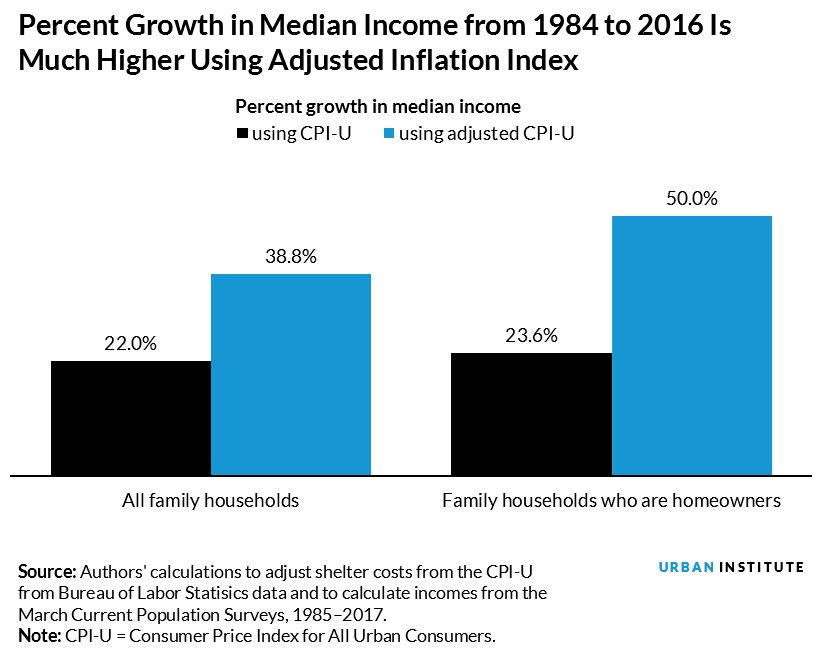

Drawing on several datasets to estimate real income growth between 1984 and 2016, we find that median incomes increase 19 percentage points faster with our shelter cost index than with the standard CPI. All the added income growth takes place among homeowners. Gains in the median income of homeowner families more than double, from 24 percent in 1984 to 50 percent in 2016.

Two striking conclusions emerge from these new estimates. First, the common perception of stagnant growth in median incomes is inaccurate. Shifting to our shelter cost index for homeowners raises median incomes substantially.

Second, gains from homeownership have been understated, especially because homeownership is a hedge against rent increases. The postcrisis shift away from promoting homeownership may have gone too far.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.