<p>(Barry Winiker/Getty Images)</p>

The few most selective, best-endowed private nonprofit colleges and universities in the nation get a lot of attention, despite the small share of students they educate. Yet our new evidence uncovers that, in addition to the other benefits that come with their elite education—particularly for students from low-income or underrepresented backgrounds—students at these colleges accumulate far less debt than students who attend the rest of the nation’s nonprofit four-year colleges and universities.

Between the late 1990s and 2016, many of the nation’s well-endowed and highly selective institutions adopted a combination of policies to reduce the prices they charge families of modest means, including replacing loans with grants for some or all students and modifying how they measure a family’s ability to pay. These policy decisions have allowed institutions to offer more grant aid to low-income students and to families whose incomes are too high to qualify for any federal or state need-based aid but who cannot afford the high prices at these colleges. During this time, the list price tuition increased substantially faster than inflation, generating more revenue from high-income families.

We use survey data from the Consortium on Financing Higher Education (COFHE)—a group of 35 wealthy, highly selective private colleges and universities—to compare debt patterns at these institutions with national patterns from the National Postsecondary Student Aid Study (NPSAS). At these elite schools, low- and moderate-income students graduated with far less debt in 2016 than similar students 12 years earlier—and with less debt than other bachelor’s degree recipients.

In the first graph, we focus on students in the classes of 2004 and 2016 from families with incomes of less than $50,000. This income was 108 percent of the median family income in 2004 but less than 69 percent of the median family income in 2016. Thus, respondents in this income range in 2016 came from lower-income circumstances than those in 2004 yet were far more likely to graduate with no debt or small amounts of debt.

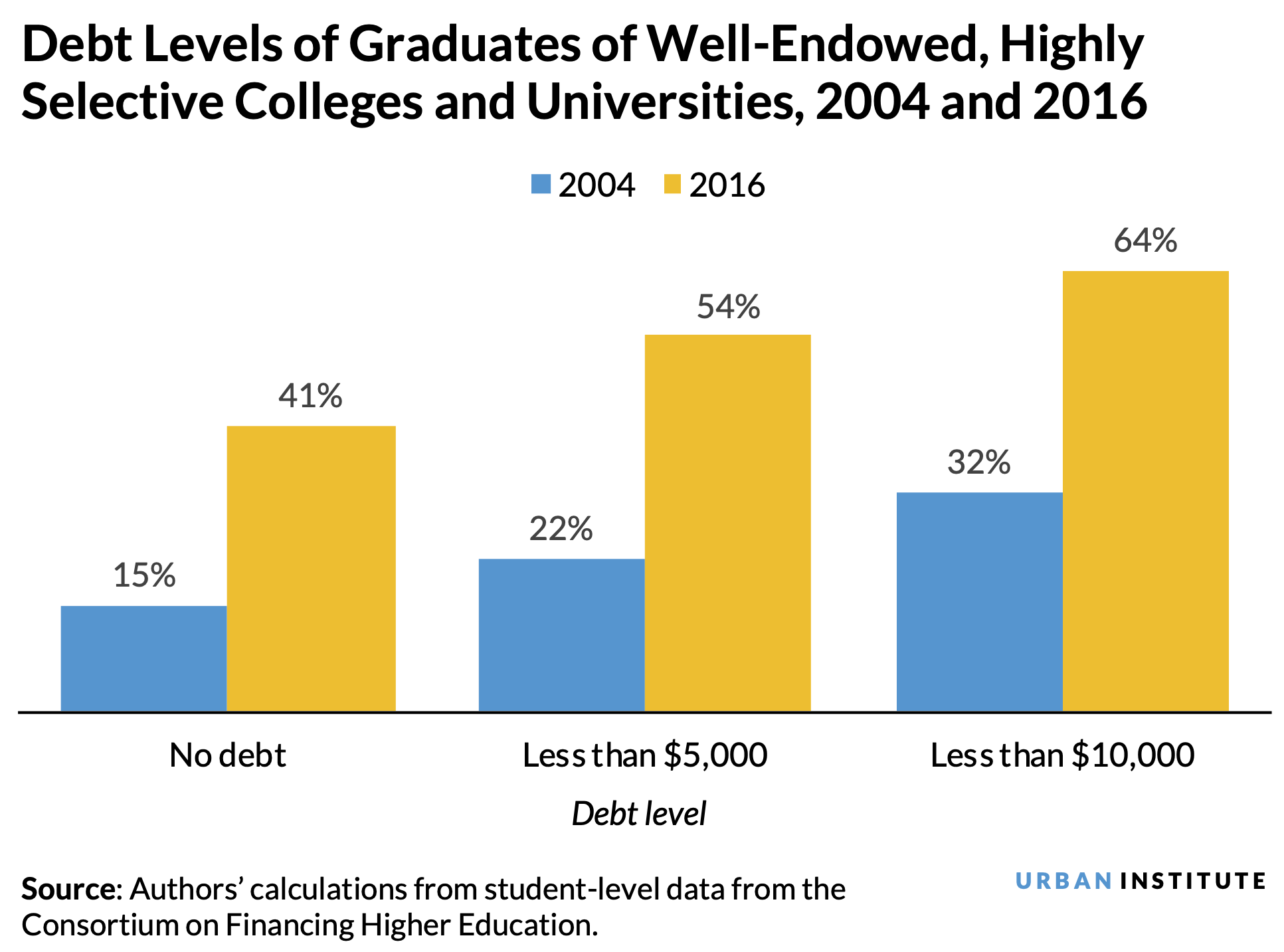

In the 2004 COFHE survey, 16 percent of respondents reported their family income was less than $50,000. In the 2016 survey, this share was 13 percent. These percentages are broadly representative of the student populations at elite schools, where 5 to 15 percent were Pell grant recipients at this time. According to NPSAS data, the share of dependent bachelor’s degree recipients from families with incomes below $50,000 was 37 percent in 2004 and 31 percent in 2016.

Students from families earning $50,000–$100,000, or roughly one to two times the median household income, were also more likely to graduate from these elite institutions debt free or with small amounts of debt in 2016 than in 2004. Forty percent of respondents said they graduated with less than $10,000 in debt in 2004. Fifty-two percent gave this response in 2016 ($10,000 in 2016 debt is less than $8,000 in 2004 dollars).

Comparing the results from the elite institutions with broader national averages from the NPSAS surveys, we see the overall share of graduates of the elite colleges who did not borrow at all rose from 50 percent in 2004 to 61 percent in 2016. In contrast, the share of all bachelor’s degree recipients in the national NPSAS data who graduated without debt fell from 38 percent to 32 percent.

In 2004, graduates of the elite colleges from families with incomes below $50,000 were less likely to graduate without debt than those from families with similar incomes at other institutions. By 2016, the situation had reversed. The share of low-income bachelor’s degree recipients across all colleges who graduated without debt fell from 30 percent to 25 percent over these years, and the fraction of the elite college sample who graduated debt-free soared from 15 percent to 41 percent.

A similar pattern emerges for students who graduated with high levels of debt. In 2004, the share of students from families with incomes below $50,000 graduating with $30,000 or more in debt was twice as high at the nation’s wealthiest private institutions as in the nation as a whole. In the 2004 survey, the maximum debt category is “more than $30,000.” That amount exceeds $38,000 in 2016 dollars, so the “more than $40,000” category in 2016 is a near match. By 2016, low-income students from the wealthiest schools were much less likely than others to have borrowed more than $40,000. Drawing conclusions about extreme debt is difficult because students who borrow much larger amounts are subsumed into these maximum categories.

Schools have only partial control over student borrowing, but the nation’s highly endowed private colleges have made substantial progress on reducing student debt for low- and moderate-income students.

The nation’s best-resourced private colleges have made great strides at reducing debt burdens on students from low- and moderate-income families. Increases in federal and state grant aid could go a long way toward doing the same for students at other institutions.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.