<p>White House Coronavirus Task Force Coordinator Dr. Deborah Birx speaks during the daily briefing on the novel coronavirus, COVID-19, at the White House on March 18, 2020, in Washington, DC. President Donald Trump ordered suspension of all evictions and home loan foreclosures. (Photo by BRENDAN SMIALOWSKI/AFP via Getty Images)</p>

The 2008 Great Recession exposed major flaws in the US mortgage servicing infrastructure. Many of these flaws have been addressed to create a better system. Our current loss mitigation toolkit is much more enhanced and can better workout a variety of borrower situations, ranging from job loss to hardship to negative equity. The economic downturn resulting from COVID-19 will be the first time these enhancements are tested in real time. The question is whether they are adequate and, if not, what more needs to be done to improve them.

The Great Recession taught us why swift action is critical to avoiding disastrous effects on the housing market. On March 18, the Department of Housing and Urban Development (HUD) announced (PDF) a 60-day moratorium on foreclosures and evictions for borrowers with Federal Housing Administration (FHA) mortgages, and the Federal Housing Finance Agency made a similar announcement for government-sponsored enterprise (GSE) mortgages. The GSEs also announced (PDF) that the more flexible forbearance and modification policies that apply to natural disasters would apply during the COVID-19 crisis.

The COVID-19 public health emergency is different than the 2008 financial meltdown

Following 2008, we witnessed severe house price declines, negative equity, and a flood of defaults. House price declines were accompanied by a swift run-up in job losses and unemployment. As a result, borrowers were not only unable to make payments in a timely manner but also unable to exit existing mortgages by selling their home.

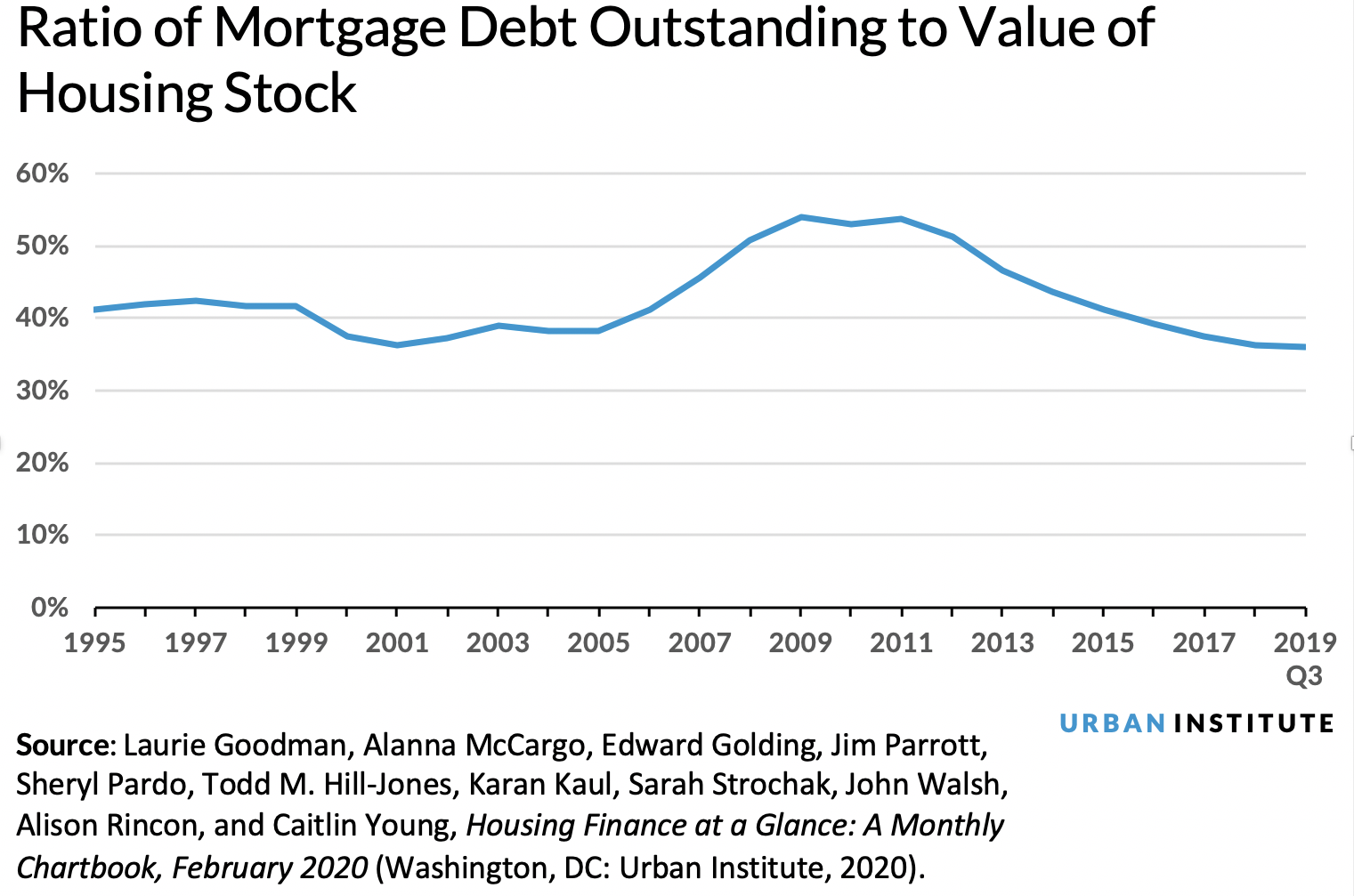

In comparison, Americans today have record levels of home equity. The ratio of total mortgage debt outstanding to the value of the US housing stock is at a record-low 36 percent, compared with 54 percent on the eve of the Great Recession. Yes, house prices could fall if we enter an extended recession, but the large equity buffer will enable borrowers to stay in their homes longer if their payment issues can be mitigated. What homeowners need right now is immediate payment relief to get through the next few months of uncertainty, income loss, and unemployment.

Are existing loss mitigation options adequate?

Before the 2008 crash, short-term assistance programs, such as repayment plans and forbearance plans, were available but often not well codified, and they often added delinquent interest and fees to the mortgage balance, limiting payment relief. Permanent assistance through mortgage modifications was either unavailable or negotiated between borrower and lender on a case-by-case basis.

However, skyrocketing delinquencies during the Great Recession created a need for a full menu of standardized loss-mitigation alternatives that could be deployed on a massive scale. This started with the Making Home Affordable programs, which provided standardized modifications through the Home Affordable Modification Program (HAMP) and foreclosure alternatives through Home Affordable Foreclosure Alternatives.

These programs were designed to work for borrowers with or without equity. In these programs, standardization was key. Even though only 1.7 million borrowers received HAMP modifications, an additional 6.7 million received proprietary modifications, with many private programs taking guidance from HAMP. Although HAMP has ended for GSE and private loans, the FHA’s implementation of HAMP (FHA-HAMP) continues. The GSEs have introduced a much-improved Flex Mod program, which is considerably more streamlined than FHA-HAMP or their previous standard modification.

Two early intervention tools, repayment plans and forbearance, have also been standardized. And as a result of experience with natural disasters, GSEs have increased the forbearance term. In November 2018, Fannie and Freddie began to allow two consecutive six-month terms of forbearance, with more available in extenuating circumstances.

Similar policies are now being applied to COVID-19 response. Although forbearance remains an effective early intervention tool, we have to be mindful of its impact on credit scores. If forbearance is not properly reported to the credit bureaus, it is treated as a delinquency. The resulting decline in credit score causes long-term financial harm to affected borrowers. The GSEs issued (PDF) guidance on March 18 suspending credit bureau reporting of delinquencies related to COVID-19 forbearance, repayment, or trial plans.

Streamlined refinancing programs are a missed opportunity

With declining mortgage rates, refinancing becomes a natural tool for payment reduction; but it isn’t simple. When refinance applications spike, capacity-constrained lenders become much more selective about who to refinance and what rates to charge. The result? Lenders are more likely to refinance borrowers with stronger credit and straightforward applications that can be approved easily. And high demand plus limited capacity gives lenders more leeway to increase their profits, resulting in higher rates for consumers.

Although that result reflects free market supply and demand dynamics, steps can be taken to increase lender capacity by improving the availability of streamlined refinances. The success of the crisis-era Home Affordable Refinancing Program (HARP), which reduced payments for 3.4 million borrowers, shows the merit of this approach. This streamlined program offered simplified documentation, no or reduced loan-level pricing adjustments (LLPA), automated appraisal, and mortgage insurance transferability.

The streamlined features result in a faster and more efficient process, which can help improve lender capacity to process applications. Although LLPA waivers allowed borrowers to get larger payment relief, automated appraisals eliminated hundreds of dollars from closing costs. Traditional rate–refinances don’t offer any of these advantages. Automated appraisals are more important than ever because homeowners and appraisers will want to maximize social distancing during this public health crisis.

The GSEs still offer refinance programs that are direct descendants of HARP: Fannie Mae’s High LTV Refinance Option and Freddie Mac’s Enhanced Relief Refinance Mortgage. However, both programs are very limited, and they restrict eligibility to loans with a 97 LTV ratio or higher. Although this helped millions of underwater borrowers during the crisis, it renders most of today’s borrowers ineligible.

What can be done to reach more borrowers?

Reducing the LTV threshold would expand eligibility, allowing many borrowers to more quickly repair their financial condition. And borrowers less likely to get a traditional refinance are exactly the ones we need to help the most.

This is a balancing act. Expanding refinance eligibility will have a negative effect on mortgage-backed security prices, which will, in turn, raise rates to new borrowers. But during a crisis period, such action seems warranted.

Overall, the loss mitigation toolkit we have in 2020 is much more robust than what we had in 2008. And the responsiveness of HUD and the FHFA indicates that they understand how valuable the postcrisis programs are in the current crisis and are remembering a key lesson from the 2008 experience: swift early intervention, even if imperfect, is much more effective than delayed actions.

Although no one knows how serious the upcoming downturn will be or how long it will last, the need of the hour is to provide immediate payment relief to the largest possible number of borrowers. The lost opportunity has been to allow the streamlined refinance programs to mostly lapse, with no crisis-type provisions for immediate restoration.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.