<p>Wanda Bee, Real Estate consultant with Re/Max, shows a condo to prospective buyer, Gioconda Velez-Brooks, at the Brickell East condos on March 31, 2016 in Miami, Florida. Photo by Joe Raedle/Getty Images.</p>

Homes are more affordable than they’ve been over the past 20 years, but this might not remain true for long. Rising interest rates and rising home prices threaten the future affordability of homeownership, and increasingly high rental costs can jeopardize borrowers’ ability to save for a down payment. In many US cities, housing has already surpassed affordable levels.

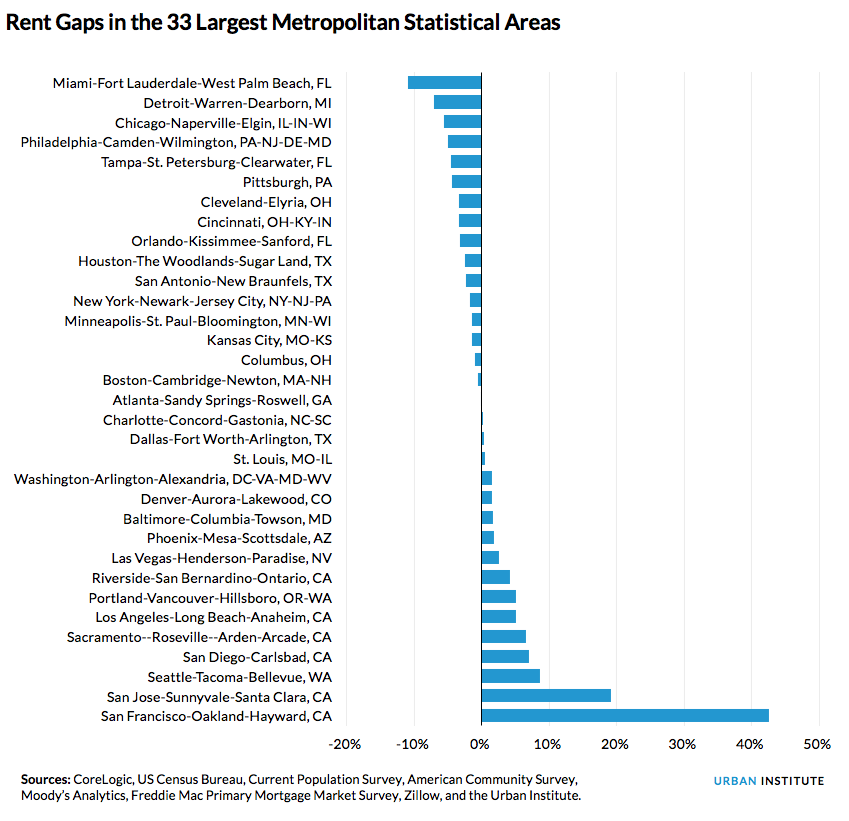

But the nature of the affordability challenge looks different across the country. In 17 of 33 large metropolitan statistical areas (MSAs), it’s cheaper to own a home, putting 3.5 percent down, than it is to rent. And in many cities where homeownership is the more affordable option, it’s expensive to buy a home.

In these cities, low–down payment and down payment assistance programs can help families achieve homeownership. Our new report, which provides information about these programs by state, can help policymakers and consumers locate the best tools for the affordability challenges they face.

In 16 cities, it’s cheaper to rent than to own a home

The chart below lists 33 MSAs based on the affordability of owning a home with a 3.5 percent down payment, and the cost of renting a home in the same market. The MSAs are listed based on the “rent gap,” or the difference between the cost of owning and renting.

In 16 of the 33 MSAs, it’s cheaper to rent than to buy a home, sometimes significantly so. The most extreme example is San Francisco, the most expensive city for homeownership. Monthly payments for a mortgage on the median-priced house with 3.5 percent down takes up 80 percent of the median borrower’s income. This is significantly more expensive than renting, where the borrower making the median income would pay 37 percent of that income in rent. The rent gap is nearly 43 percent.

Other cities on the West Coast show a similar trend, though none as extreme as San Francisco. In Seattle, which ranks seventh in the cost of homeownership, renting is also the cheaper option. A borrower who buys a home with a low down payment there can expect to pay an additional 8.6 percent of their income on housing.

Six California cities have rent gaps that exceed 4 percent: Los Angeles, Riverside, Sacramento, San Diego, San Francisco, and San Jose. Other cities where renting is notably cheaper include Las Vegas and Portland.

In 17 cities, it’s cheaper to own, but homeownership may still be expensive

Cities where owning is less expensive than renting tend to be more affordable, but this is not always the case. In over half the MSAs we studied, owning a home was more affordable than renting on a monthly basis, and in nine of these cities, homebuyers could save more than 3 percent of their incomes.

Miami has the largest negative rent gap in the country. The median borrower would save 11 percent of their income if they bought the median-priced home with 3.5 percent down instead of renting. But it’s not cheap to buy in Miami, which ranks 11th in mortgage affordability nationally, with a median mortgage payment that consumes 32 percent of the median income.

Because Miami is the second-most-expensive city for rental housing, however, the median rent consumes 42 percent of the median income. So even at this high cost, homeownership is still the better bet.

Other cities, such as Chicago, Orlando, and Tampa, have high rental costs but more affordable homeownership. Chicago ranks 13th for rental costs but merely 24th for the cost of owning a home. This yields a rent gap of nearly 6 percent. Orlando and Tampa have rent gaps of 3 and 5 percent, respectively.

Down payment assistance can put homeownership within reach in high-cost cities

Each city presents a unique challenge to homeownership. Our new report shows how borrowers can benefit from down payment assistance programs. If borrowers can make the higher mortgage payments required with lower down payments, additional programs offer grants to cover down payments and closing costs. These programs can help put borrowers into homes so they can start building equity.

In cities like Miami and Chicago, homeownership is the more cost-efficient option. But renters still spend a large portion of their incomes on rent, which can impede their ability to save for a down payment. Thirty-six percent of Miami applicants and 43 percent of Chicago applicants were eligible for down payment assistance, yielding average assistance of $10,023 and $5,647, respectively. In these two cities, and in other cities with negative rent gaps, this help could put homeownership within reach for many families.

Low– and no–down payment loans have a role to play in the current housing environment, and the 2,144 active down payment assistance programs across the country offer additional assitance to borrowers. But the limited availability of down payment programs and minimum eligibility requirements raise obstacles for many borrowers.

These programs also vary in pricing and offer high-risk loans that may require private mortgage insurance, so counseling and consumer education are critical to ensuring that consumers understand how the programs work and any additional costs that may be incurred. Our new report, which provides information about these programs by state, will help policymakers and consumers locate the best tools for the affordability challenges they face.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.