The November 2023 edition of At A Glance, the Housing Finance Policy Center’s reference guide for mortgage and housing data, shows that for the first time in series history (dating back to 2004) serious delinquency rates on Fannie Mae single-family loans equals the rate on Fannie Mae multifamily loans. This month’s introduction addresses challenges in the multifamily market.

Introduction

While the Single-family Market Continues to Heal, the Multifamily Market Shows Emerging Signs of Trouble

Since the aftermath of the pandemic recession, serious delinquency rates on 1-4 family GSE mortgages continues to fall, sitting at historically low levels. Serious delinquency rates on GSE multifamily loans also remain low, but they are rising. The higher multifamily serious delinquency rates correspond with a challenging landscape in the multifamily market. Amid the continued prospect of interest rates remaining “higher for longer”, these risks could have important implications for the GSEs given their growing role in debt financing existing multifamily properties.

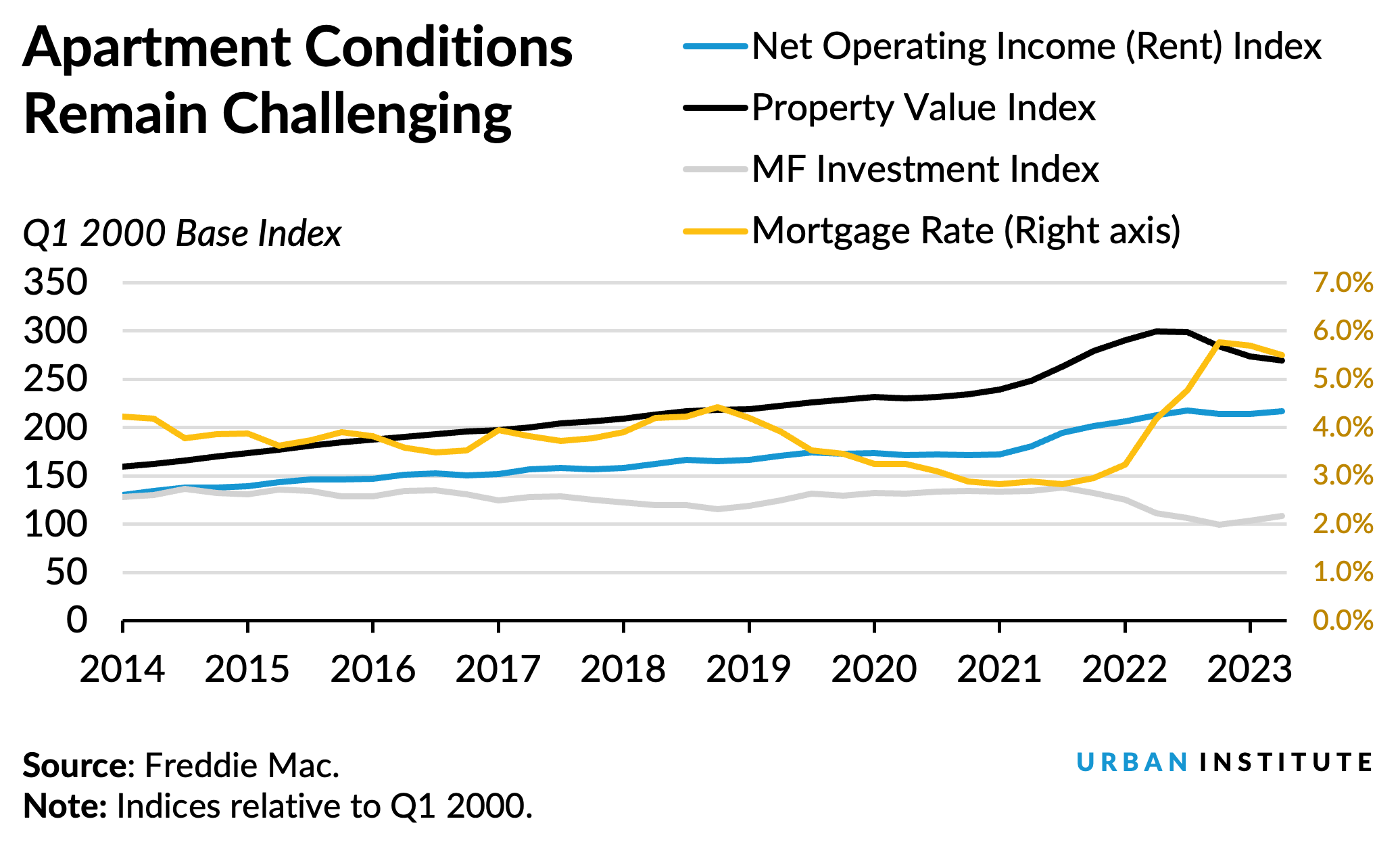

Approximately 87 percent of occupied multifamily units are renter-occupied. But according to the Apartment Investment Market Index (AIMI), produced by Freddie Mac, the multifamily investment environment has weakened nationwide. This index measures what investors are paying per dollar of net operating income, taking into account both interest rates and property values. As illustrated by the AIMI, the general weakness in the multifamily market has coincided with the upward trajectory of interest rates; this decreases the AIMI’s value because it increases debt service payments. Between the third quarter of 2021 and the second quarter of 2023, multifamily mortgage rates, compiled from the American Council on Life Insurers, rose from 2.8 percent to 5.5 percent. Over this same period, the AIMI has fallen by 21.2 percent to an index measure of 108.6.

The lower AIMI, reflecting higher mortgage rates, is partly attenuated by higher net operating income (NOI) and by falling property values. Higher net operating income will increase the AIMI due to the greater rental income investors are receiving on the property while falling property values can boost the AIMI because it reduces the cost of investing. Over this same two-year period, the NOI index, largely reflecting rents, increased by 11.2 percent to an index value of 216.6. However, the index has stagnated over the past three quarters. And while the property value index is 2.5 percent higher over the entire eight-quarter period, it began to decline in the second quarter of 2022.

While falling property values may reduce costs for new investors, they may also lower the equity of current property owners. And the impact of lower property values is amplified for mortgaged properties. Amid higher mortgage rates, falling property values and stagnating NOI, the Mortgage Bankers’ Association reports in its Commercial/Multifamily Quarterly Databook covering the second quarter of 2023 that delinquency rates on multifamily loans have been rising. This affirms the rising trend in serious delinquency rates among GSE multifamily loans and stands in contrast to the declining trend in GSE serious delinquency rates on 1-4 family loans (see page 33 of this chartbook).

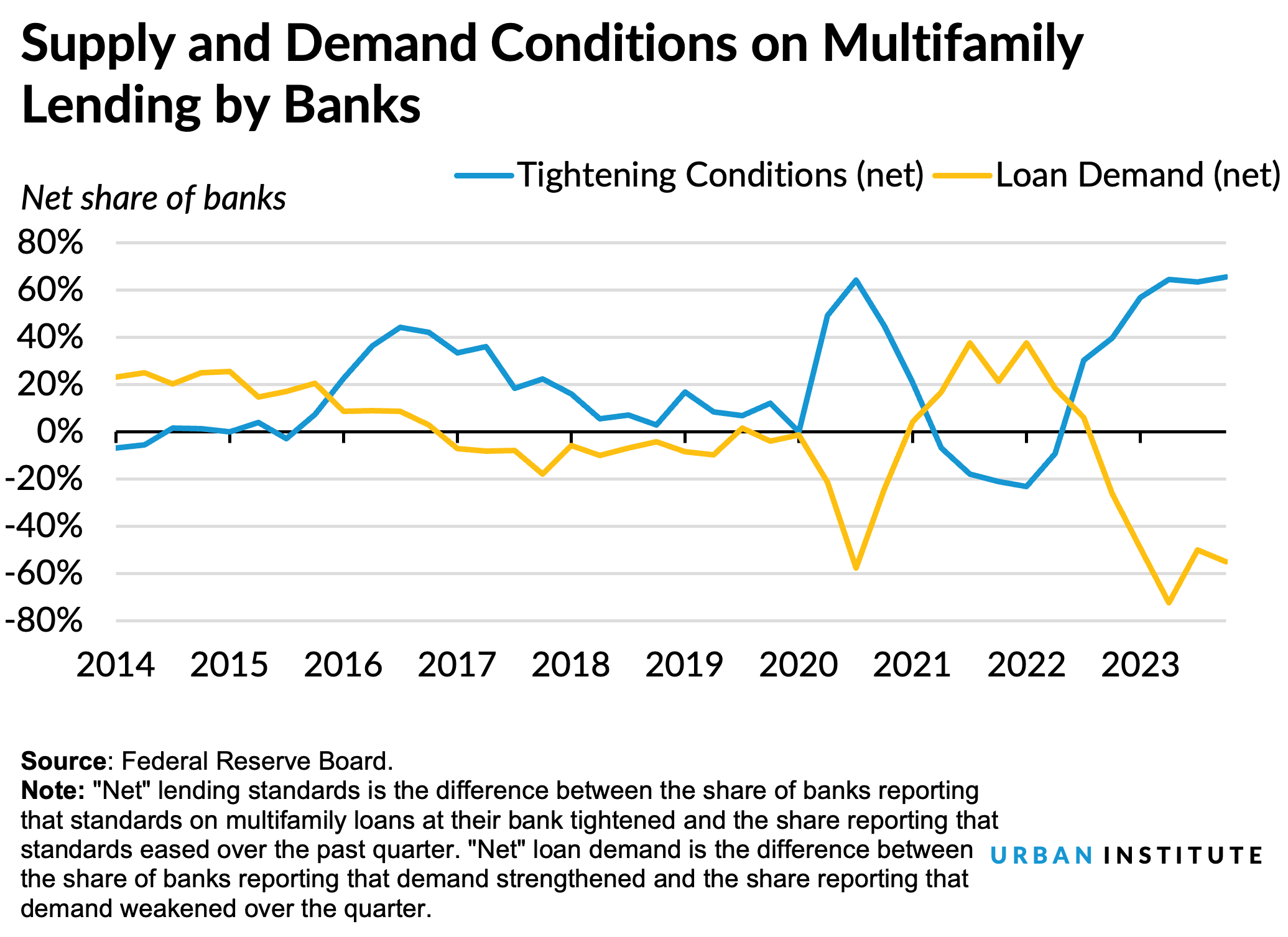

Amid worsening multifamily conditions, multifamily debt financing activity appears to be stalling. Lending standards on multifamily loans reported by banks through the Senior Loan Officer Opinion Survey are tightening significantly. At the same time demand for multifamily loans is declining.

The multifamily market may continue to struggle in the near term. In 2023, new multifamily unit completions are likely to be stronger while vacancy rates among 5+ unit multifamily rents are higher. In fact, multifamily completions have been higher in 2020, 2021, 2022 and 2023 than any year since the late 1980s. This suggests that property values as well as rents could continue to soften. The Housing Finance Policy Center will continue to track these developments and assess their impact on the GSEs, the mortgage lending landscape and the broader financial system.