Police expenditures include spending on police, sheriffs, state highway patrols, and other governmental departments charged with protecting public safety.

Corrections expenditures are for the operation, maintenance, and construction of prisons and jails, as well as the activities of probation officers and parole boards.

Court expenditures, which the Census defines as "judicial" expenditures, cover government spending on civil and criminal courts plus spending on activities associated with courts such as prosecuting and district attorneys, public defenders, witness fees, law libraries, and register of wills. It does not include probation or crime victim compensation and reparation.1

- How much do state and local governments spend on police, corrections, and courts?

- How does state spending differ from local spending and what does the federal government contribute?

- How have police, corrections, and courts expenditures changed over time?

- How and why does spending differ across states and localities?

How much do state and local governments spend on police, corrections, and courts?

In 2021, state and local governments spent $135 billion on police (4 percent of state and local direct general expenditures), $87 billion on corrections (2 percent), and $52 billion on courts (1 percent).

Nearly all state and local spending on police, corrections, and courts in 2021 went toward operational costs such as salaries and benefits (96 percent for police, 97 percent for corrections, and 98 percent for courts). Capital spending accounted for 4 percent or less of total spending for each expenditure category in 2021.

Capital spending has never been a large share of either police or court expenditures. From 1977 to 2021, the highest annual share of capital spending for police expenditures was 5 percent (multiple years). From 1992 to 2021, the highest share of capital spending for court expenditures was 6 percent (1997). (We do not have access to courts expenditure data for years prior to 1992.)

In contrast, capital spending on corrections, such as prison construction, was greater than 10 percent every year from 1977 to 1995. The share of capital spending on corrections reached a high of 16 percent in 1988. However, capital spending's share of corrections spending has not been above 10 percent since 1995, and its share has been below 5 percent every year since 2010.

How does state spending differ from local spending and what does the federal government contribute?

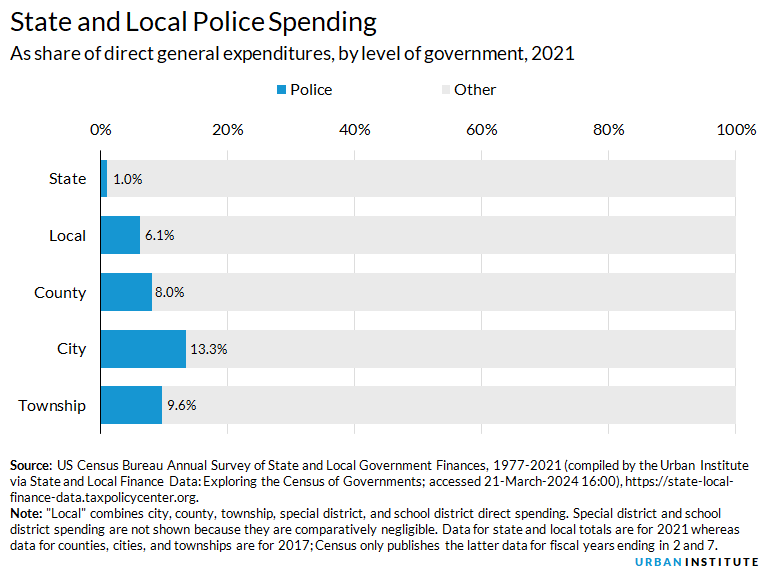

Most direct spending on police was done by local governments (87 percent) in 2021. As a share of direct general expenditures, police spending was 1 percent of state expenditures and 6 percent of local expenditures that year. State expenditures on police mostly included spending on highway patrols, while local funds supported sheriffs' offices and police departments.

Looking at specific types of local government in 2017 (the most recent year that we have data for these levels of government), police spending accounted for 13 percent of city direct general expenditures, 10 percent of township expenditures, and 8 percent of county expenditures.

In contrast, most direct spending on corrections was done by state governments in 2021 (64 percent). As a share of direct general expenditures, corrections spending was 3 percent of state expenditures and 2 percent of local expenditures in 2021. State spending on corrections included state-operated prisons, while local spending was concentrated on county jails.

Spending on courts was roughly split between state and local governments in 2020 (49 percent for states and 51 percent for localities). As a share of direct general expenditures, courts spending was roughly 1 percent for both state expenditures and local expenditures. Among local governments, court spending in 2017 as a percentage of general expenditures was the highest at the county level (5 percent of county direct general expenditures).

Nearly all state and local spending on police, corrections, and courts was funded by state and local governments because federal grants account for a very small share of these expenditures. However, these totals do not include direct federal spending on criminal justice (e.g., federal prisons). The federal government directly spent $30 billion on police, $7 billion on corrections, and $15 billion on courts in 2017 (the most recent year that we have data).

How have police, corrections, and courts expenditures changed over time?

From 1977 to 2021, in 2021 inflation-adjusted dollars, state and local government spending on police increased from $47 billion to $135 billion, an increase of 189 percent. Among major programs, the spending growth on police trailed both public welfare and health and hospital expenditures and was roughly equal with spending growth for higher education expenditures. Much of the increase in public welfare spending over this period was driven by federal spending increases on Medicaid.

Over the same period, real corrections expenditures increased from $19 billion to $87 billion, an increase of 346 percent. Spending growth on corrections over this period was higher than all other major programs except for public welfare. However, this in part reflects the relatively low spending totals on this program. In real dollars, corrections spending increased $67 billion from 1977 to 2021, while public welfare increased nearly $708 billion. (For more information on spending growth see our state and local expenditures page.)

We do not have access to court spending back to 1977, but from 1992 to 2021, in inflation-adjusted dollars, state and local government spending on courts increased from $32 billion to $52 billion, an increase of 65 percent.

As a share of all state and local direct general expenditures, none of these criminal justice expenditures have changed much over the past 40-plus years. However, that consistency is in part a reflection of how much state and local governments spend on other programs, and particularly on elementary and secondary education and public welfare, both of which account for roughly one-fifth of state and local direct general expenditures. From 1977 to 2021, police spending has consistently accounted for roughly 4 percent of direct state and local general expenditures. Over the same period, corrections spending as a share of state and local spending increased slightly from 1.6 percent to 2.4 percent. Court spending as a percentage of state and local direct general expenditures remained under 2 percent from 1992 to 2021.

How and why does spending differ across states and localities?

Across the US, state and local governments spent $407 per capita on police protection in 2021. The District of Columbia3 spent the most per capita on police in 2021 at $1,000, followed by California ($636), Alaska ($552), and New York ($539). The lowest-spending per capita states in 2021 were Kentucky ($232), Arkansas ($241), Indiana ($251), and Maine ($256).

Data: View and download each state's per capita spending by spending category

State and local governments spent $262 per capita on corrections in 2021. Alaska spent the most per capita on corrections in 2021 ($517), followed by California ($460), the District of Columbia ($412), New Mexico ($381), and Oregon ($377). The lowest-spending states per capita in 2021 were Missouri ($144), Hawaii ($153), Iowa and South Carolina (both $154), and New Hampshire ($155).

Note: For data on corrections spending, please use our State and Local Finance Data tool.

In 2021, states and local governments spent $158 per capita on courts. The District of Columbia spent the most on courts per capita in 2021 ($347), followed by Alaska ($341), New York ($249), and California ($236). The lowest spending states in 2021 were Arkansas ($87), Alabama ($88), Oklahoma ($91), Maine ($93), and North Carolina ($95).

Per capita spending is an incomplete metric because it does not provide any information about a state’s demographics, policy decisions, or administrative procedures.

For example, states with high per capita spending on police tend to have high levels of spending per employee, reflecting the labor-intensive nature of police work. That is, states that spend more per capita tend to have higher costs of living and that drives up wages. Thus, cost of living differences among states account for some of the variation in per capita spending.

States with high per capita spending on corrections are a mix of states with high labor costs and those with large populations of individuals in state or local prisons or under parole or probation.

However, police and corrections employees are often paid above the amount that these labor market conditions might predict. Some states with moderate per capita corrections costs, such as Georgia, compensate for a high number of people in prison, on probation, or on parole by employing fewer staff per inmate, probationer, and parolee, and by spending less per employee on payroll costs.4

There are also significant differences in police spending, as a share of overall spending, across localities simply because different levels of government fund police (and other services) in different states. For example, the city of Las Vegas, Nevada spent less than 2 percent of its budget on the police in 2021, but Clark County, Nevada spent 14 percent of its budget on police. In contrast, police spending accounted for 23 percent of the City of Milwaukee's budget but just 6 percent of the County of Milwaukee's budget. New York City spent nearly $6 billion on police in 2021, but that was only 6 percent of its budget in part because New York City public school spending was included in the city's budget—and accounted for a third of the city’s overall spending in 2021.

The average spending on police for jurisdictions with more than one million people was 10 percent in 2017. The average for jurisdictions with fewer than 50,000 people was 13 percent. Again, this variation is driven in large part by what particular services jurisdictions deliver (and do not deliver).

Interactive Data Tools

Reducing mass incarceration requires far-reaching reforms

What everyone should know about their state’s budget

State and Local Finance Data: Exploring the Census of Governments

Further Reading

Following the Money on Fines and Fees

Aravind Boddupalli and Livia Mucciolo (2022)

What Police Spending Data Can (and Cannot) Explain amid Calls to Defund the Police

Richard C. Auxier (2020)

Promoting a New Direction for Youth Justice: Strategies to Fund a Community-Based Continuum of Care and Opportunity

Samantha Harvell, Chloe Warnberg, Leah Sakala, and Constance Hull (2019)

Public Investment in Community-Driven Safety Initiatives

Leah Sakala, Samantha Harvell, and Chelsea Thomson (2018)

Assessing Fiscal Capacities of States: A Representative Revenue System–Representative Expenditure System Approach, Fiscal Year 2012

Tracy Gordon, Richard Auxier, and John Iselin (2016)

Notes

1 Data are from Census functions E62, F62, G62, E04, F04, G04, E05, F05, G05, E25, F25, and G25.

2 Direct general spending refers to all direct spending (or spending excluding transfers to other governments) except spending specially enumerated as utility, liquor store, employee-retirement, or insurance trust. Unless otherwise noted, all data are from the US Bureau of the Census, Survey of State and Local Government Finance, 1977–2021, compiled by the Urban Institute via State and Local Finance Data: Exploring the Census of Governments (https://state-local-finance-data.taxpolicycenter.org), accessed on March 16, 2024 The census recognizes five types of local government in addition to state government: counties, municipalities, townships, special districts (e.g., a water and sewer authority), and school districts. All dates in sections about expenditures reference the fiscal year unless explicitly stated otherwise.

3 The District of Columbia is often an outlier because, although it functions as a state and a locality, it most closely resembles a central city in terms of its population and economic activity, much of which comes from nonresidents. Its ranking among states should be interpreted within this context.

4 For an analysis of components of state and local spending using 2012 data, see the Urban Institute’s interactive tool, What everyone should know about their state’s budget.