In May 2025, the House of Representatives passed budget reconciliation legislation, H.R. 1, that would make substantial changes to health coverage programs. Although provisions that would cut Medicaid enrollment have received the most attention so far, changes to the health insurance Marketplaces would also be extensive. The bill includes an array of eligibility cuts, subsidy reductions, and new paperwork barriers that would substantially reduce enrollment in the Marketplace and result in some people becoming uninsured.

Why This Matters

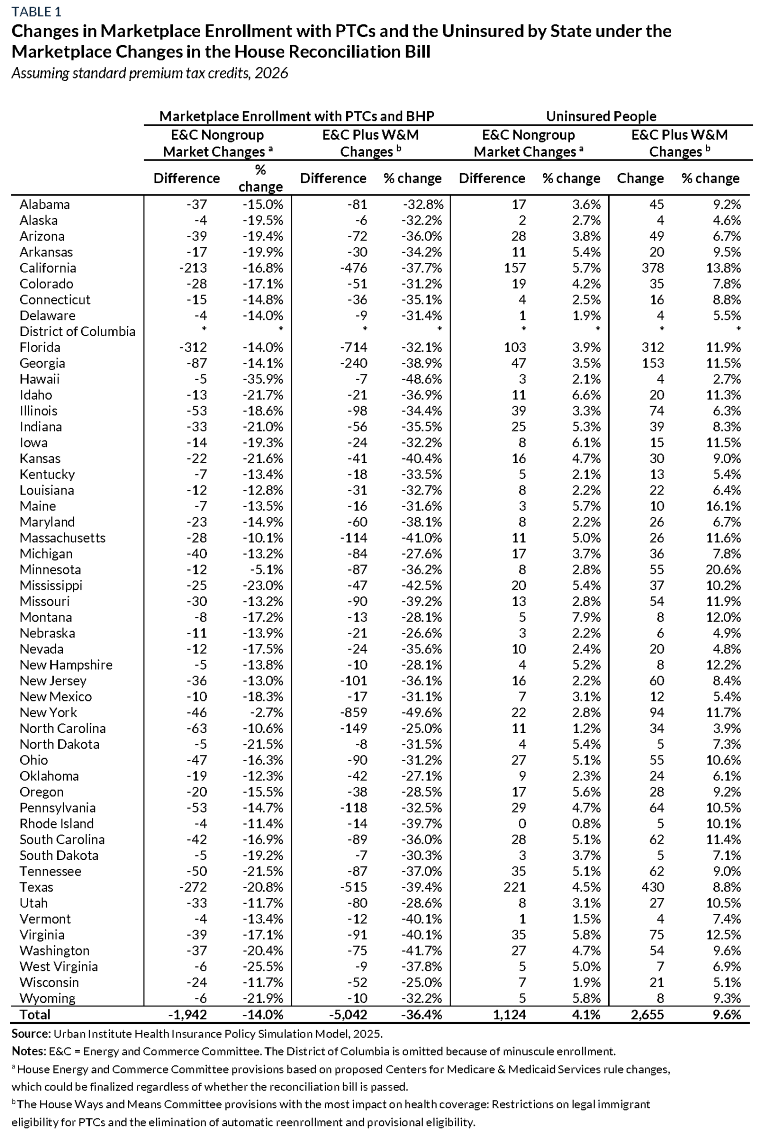

We add to existing analyses by providing state-by-state estimates of the bill’s provisions on Marketplace enrollment and the number of uninsured, in addition to our national estimates. If passed into law, the combined provisions affecting the Marketplace and Basic Health Program (BHP) would lead to enrollment declines of one-third or more in most states. Enrollment drops of this magnitude can negatively affect Marketplace stability, leading some insurers to withdraw.

In the first year or two, however, enrollment declines could be even greater than we estimate, because of the major disruptions in established enrollment processes and the limited time available for insurers, states, and consumers to adjust. The National Association of Insurance Commissioners, which represents insurance regulators in all 50 states, has warned that there is insufficient time to prepare for the changes and expressed concern about overall market stability. They highlight the required changes to eligibility verification and reenrollment procedures that may prevent many eligible enrollees from successfully gaining or maintaining coverage.

What We Found

We find that these provisions would reduce Marketplace and BHP enrollment (in the three states with a BHP) by 5 million people in total, or 36.4 percent on average (table 1). The decline is mainly due to provisions from the Ways and Means Committee, which account for 3.1 million people. Marketplace and BHP enrollment would fall by one-third or more in 27 states and by 40 percent or more in eight states. These declines would be on top of declines in Marketplace enrollment because of the expiration of the premium tax credit (PTC) enhancements, which we previously estimated would reduce Marketplace enrollment by 7.2 million people.

Finally, we also find that H.R. 1’s Marketplace provisions would leave 2.7 million additional people uninsured in 2026. Our national estimates are largely consistent with the Congressional Budget Office's estimates after accounting for certain differences; for example, we estimate the number of uninsured people would grow to at least 3.5 million in 2034, which is very similar to the Congressional Budget Office's estimate of 4 million.

Considering the compounding impacts of Medicaid cuts, the scheduled expiration of premium tax credits, and the policies modeled here, stakeholders are unsurprisingly raising alarm about risks to individuals and the viability of health insurance markets.