Housing is considered a social determinant of housing. But in this brief we explore the implications of health and its impact on housing outcomes. We specifically focus on the role played by the pandemic in producing adverse outcomes for homeowners. The COVID-19 pandemic undermined homeownership stability by inducing sickness and mortality, fueling a recession, and increasing the desire for home renovations. And disadvantaged communities appeared to have been disproportionately harmed by this shock. This brief explores policies and recommendations learned from the pandemic that can strengthen homeowner resilience to future shocks.

Why This Matters

The relationship between housing and health is not one directional. The pandemic was an extreme example of how health can impact housing. In response to the pandemic, policymakers responded by addressing both the implications of a health crisis and that of a traditional recession. Looking forward, federal, state, and local policymakers can also apply the pandemic’s lessons to promote recovery and strengthen household resilience for future shocks, such as recessions and climate disasters.

Key Takeaways

- COVID-19 undermined homeownership by inducing sickness and mortality. These health outcomes had an outsize impact on mortgage delinquencies following the onset of the pandemic. These health risks were also disproportionately greater for households of color, who experienced higher rates of infection, hospitalization, and death throughout the pandemic.

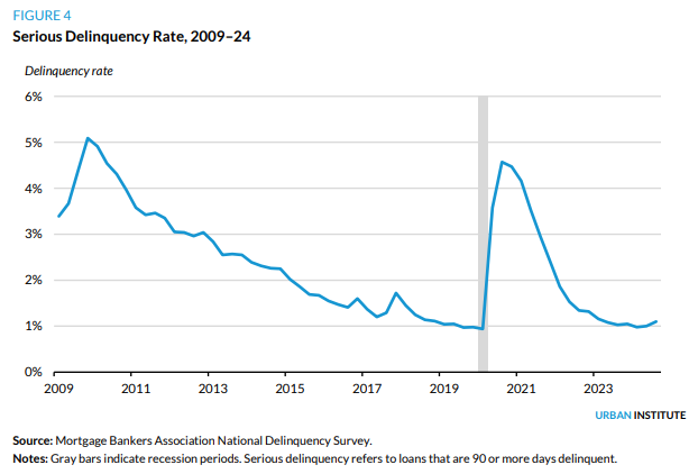

- COVID-19 undermined homeownership by fueling a recession. Amid rising unemployment rates following the onset of the pandemic, the serious delinquency rate for mortgages spiked considerably. Reports also indicate that delinquency was greater among homeowners of color, reflecting an unequal distribution of financial impact attributable to pandemic-related effects.

- COVID-19 undermined sustainable homeownership by highlighting the desire for home renovations. Households of color faced disproportionately greater challenges, as they were more likely to live in physically inadequate homes that required repair. Homeowners of color also faced greater financial constraints that limited their ability to repair their home or increased the renovation costs.

- Policy can improve homeowner sustainability in and out of crisis. Policymakers can apply the successes of the pandemic response to future shocks to ensure vulnerable homeowners can keep their homes. These include actions focused on preventing foreclosures, providing options for home repair, and ensuring climate resilience.

How We Did It

This brief draws on our analysis of American Community Survey, American Housing Survey, Survey of Consumer Finances, and Home Mortgage Disclosure Act data to show the landscape of housing market conditions both before and after the onset of the COVID-19 pandemic. We used timely surveys conducted during the pandemic from the Federal Housing Administration and the Mortgage Bankers Association to capture the pandemic’s effects on mortgage delinquency rates and homeownership sustainability.