In 2025, many families relied on credit and savings to meet their food needs. Families with low incomes and those who reported that their grocery costs had increased a lot in the past year were the most likely to take on debt to pay for groceries, which could leave them less able to meet their basic needs in the future.

Why This Matters

Groceries are one of the largest household budget items for families. Today, families face persistently higher grocery prices than they did five years ago. In such circumstances, they may turn to savings and credit to purchase the food they need. Although access to credit and savings can provide a lifeline and help families smooth household spending, overreliance on these resources may lead to financial instability if they have a hard time keeping up with debt or rebuilding savings.

What We Found

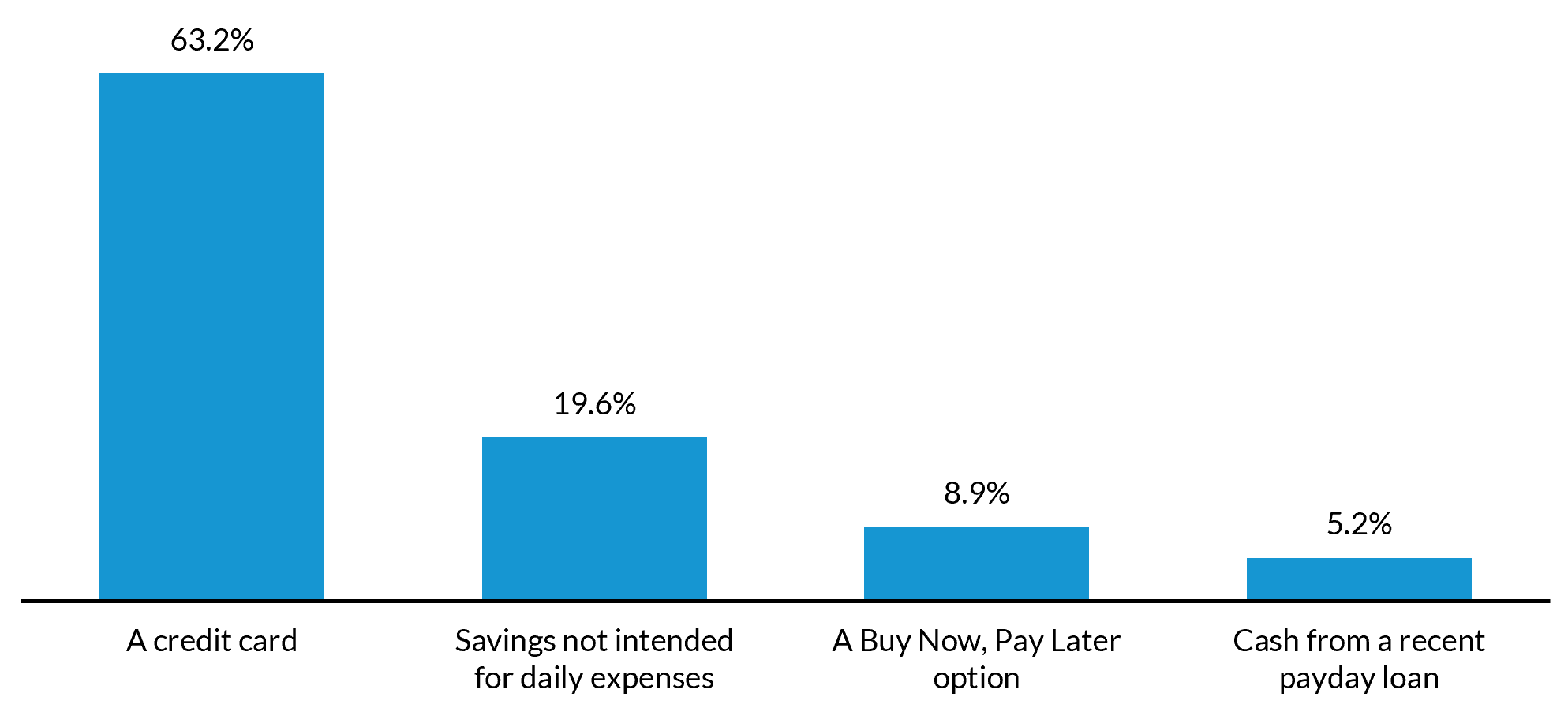

Our analysis found the following about how families paid for groceries in 2025:

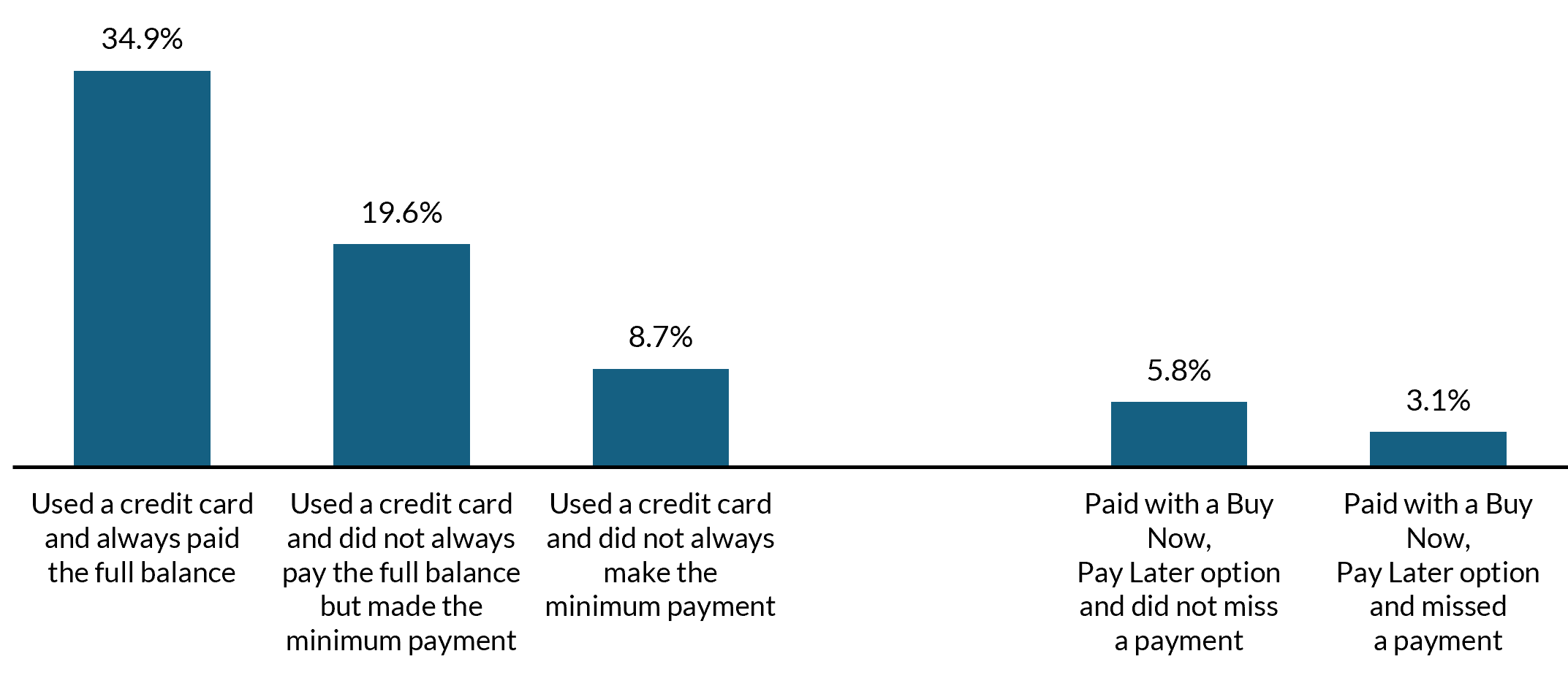

- Although 34.9 percent of working-age adults (ages 18 to 64) paid for groceries with a credit card and paid the bill in full, 19.6 percent paid less than the full balance but always made the minimum payment and 8.7 percent did not always make the minimum payment. This means that over 1 in 4 working-age adults used credit cards to purchase food for their families and experienced repayment challenges.

- Nearly 1 in 10 working-age adults used Buy Now, Pay Later (BNPL) options to pay for groceries; among them, 1 in 3 (34.8 percent) missed a BNPL payment.

- Nearly 1 in 5 working-age adults (19.6 percent) reported paying for groceries with savings not intended for daily expenses.

- Nearly 1 in 20 working-age adults (5.2 percent) used cash from a recent payday loan to purchase groceries.

- Working-age adults with low and moderate incomes were more likely to experience repayment challenges than those with high incomes: more than half of low- and moderate-income working-age adults who paid for groceries with credit cards did not always pay the full balance, compared with just over a third of higher-income adults.

- Just over half (51.3 percent) of working-age adults reported that their grocery costs increased a lot in the past 12 months. They were more than twice as likely (12.4 percent) not to make the minimum payment when using credit cards to purchase groceries, compared with those who reported that their grocery costs increased a little (5.2 percent) or not at all (4.8 percent).

- More working-age adults reported using a credit card to pay for groceries and not always making the minimum payment in 2025 than in 2023 (an increase of 1.6 percentage points, from 7.1 percent in 2023 to 8.7 percent in 2025).

Share of adults ages 18 to 64 whose families used selected types of credit or savings to buy groceries in the past 12 months, December 2025

Source: Well-Being and Basic Needs Survey, December 2025.

Notes: Estimates in this chart are not mutually exclusive; adults could report using more than one method to pay for groceries.

Share of adults ages 18 to 64 whose families used credit cards or Buy Now, Pay Later options to buy groceries and experienced repayment challenges in the past 12 months, December 2025

Source: Well-Being and Basic Needs Survey, December 2025.

Notes: Repayment challenges occur when adults use credit to purchase groceries and do not pay the balance in full and on time.

These findings show that many families used savings, credit cards, BNPL, or payday loans to afford groceries. There is evidence of growing financial stress since 2023, with more working-age adults experiencing repayment challenges when using credit cards to purchase food for their families.

How We Did It

This analysis draws on data from the December 2025 round of the Well-Being and Basic Needs Survey, a nationally representative, annual survey of adults that monitors individual and family well-being in the context of a changing safety net. More than 10,000 adults participated in the 2025 survey, including over 7,500 adults ages 18 to 64.