Wealth-building accounts help to establish a wealth floor and level the playing field, ensuring that individuals with no or low wealth do not start at zero and have the ability to build wealth over time. Investments like these help individuals and families build long-term financial security, protect against job losses and economic shocks, and provide a foundation for investments in education, homeownership, and entrepreneurship. Starting investments at birth, rather than when one enters the workforce, results in an additional $9,000 for postsecondary education at age 18, $65,000 for home or business ownership at age 35, and $473,000 for retirement at age 65.

Unequal access to and participation in financial markets has been shown to deepen existing inequality across gender, class, and race, which has harmful effects on the economy because it limits economic mobility and slows overall economic growth. To support prosperity for all, public and private leaders can ensure that families have opportunities to invest in capital markets and build assets that grow over time.

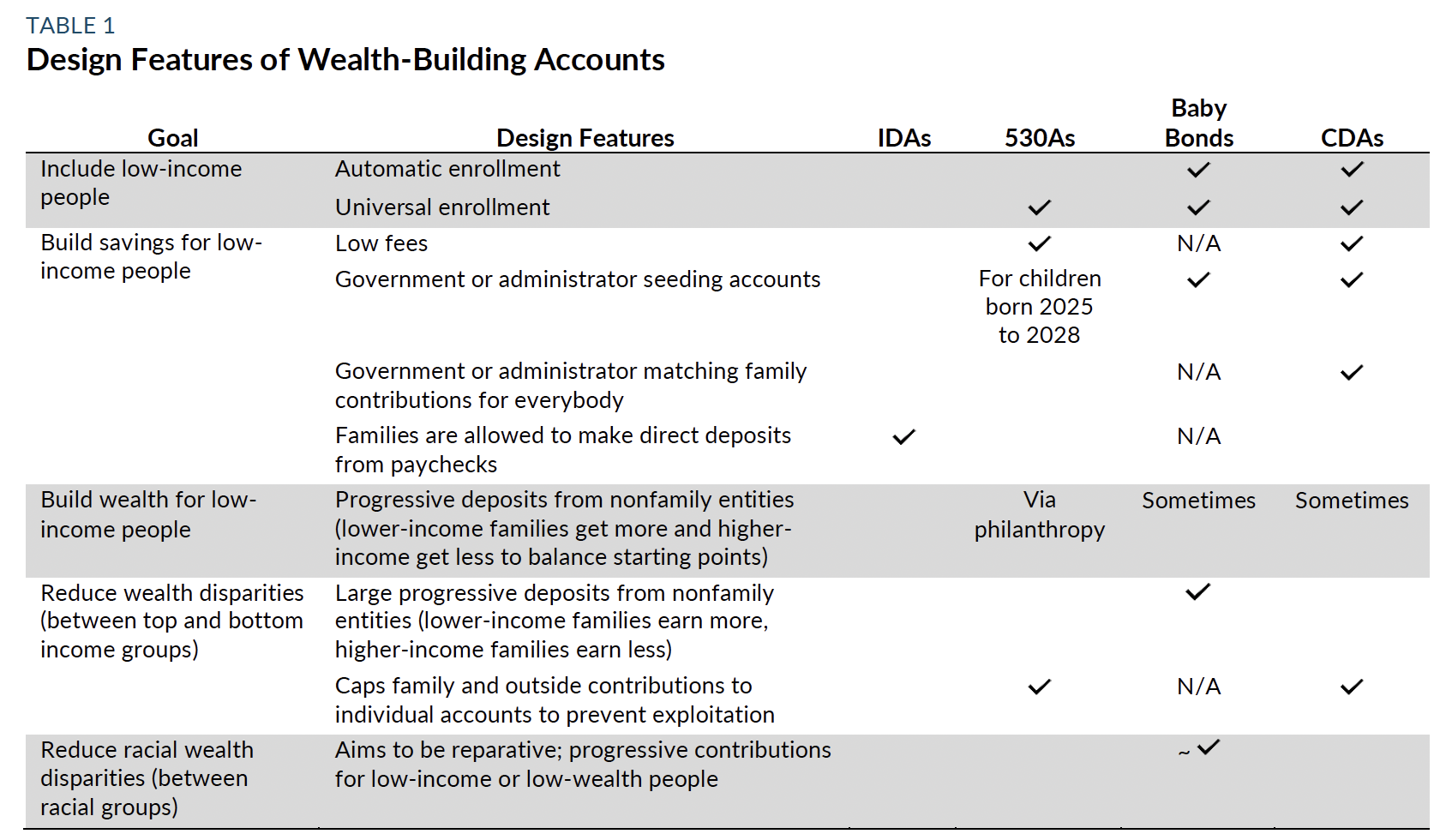

Are wealth-building accounts designed to improve economic mobility?

Yes, depending on how they are designed (see table 1).

What do design choices mean for whom and how these accounts build wealth?

Beginning in the 1990s, Individual Development Accounts (IDAs) were launched as matched savings accounts. McKernan and colleagues found that the federally funded Assets for Independence IDA program decreased material hardship and increased savings for participants, and in some cases increased homeownership and business ownership rates. However, other studies found no significant evidence that IDAs increased net worth or that the accounts reduced racial wealth disparities over time.

Child development accounts (CDAs) were designed as universal and automatic savings accounts (with seeding and matching from entities other than the family). However, seed funding is often less than $200 due to constrained public resources, so CDAs have not significantly reduced wealth disparities as much as expected. In addition, participants’ use of CDA assets is limited—they can use them for higher education but not for other wealth-building activities, such as homeownership, business ownership, or retirement investments.

Introduced in 2010, baby bonds are universal, publicly funded child trust accounts (as opposed to savings accounts). Twenty-three states have passed or considered legislation for baby bonds, and nine states have active pilot demonstrations. At least four simulations of a national baby bonds program found that the policy would reduce racial wealth disparities at varying scales: Cosic and colleagues (2024); Mitchell and Szapiro (2020); Weller, Maxwell, and Solomon (2021); and Zewde (2020). Urban Institute researchers also found that baby bonds would decrease the share of people taking out student loans, and reduce the total amount of borrowers’ student loan debt by age 45, with the greatest impacts among Black and Latino student loan holders.

In 2025, 530As (Trump Accounts) were established as tax-deferred accounts available to all children with social security accounts, but they require parents to opt in via tax returns or online. The federal government will provide a onetime $1,000 seed deposit for all babies born between 2025 and 2028, after which, children born in certain areas and with families meeting certain income thresholds will receive additional funding from private-sector stakeholders.

Notes: Previous research on statewide CDA models and 529 college savings accounts shows that opt-in policies tend to mainly enroll families with more financial resources and more education, even when paired with additional outreach and communication. Low-income families, who are most likely benefit from those programs, are less likely to enroll due to administrative barriers and information gaps. We considered the potential impacts of IDA, 530A, and Baby Bonds design features based on insights and findings from CDA models, studies, and evaluations, including Brown and Cosic (2026); Clancy and Sherraden (2014); Clancy, Sherraden, and Beverly (2019); Huang and colleagues (2021). (~) indicates that this design has not yet been fully implemented.

Policy in Action: Freedom Futures

Freedom Futures is an accelerated baby bond program that was launched by the Georgia Resilience Opportunity Fund in Atlanta in 2025. Established following the introduction of a bill in the 2023–2024 legislative session, the fund aims to produce supporting evidence to advance baby bonds legislation in Georgia. A guaranteed income component of $500 per month helps with day-to-day expenses, and asset-building accounts with an initial $20,000 deposit followed by monthly supplements help to build wealth. Unlike other baby bond programs, Freedom Futures is for young people between ages 18 and 25, rather than for infants, so accounts are more immediately available to participants (i.e., in program years 2 and 3). Although this pilot program has a relatively small number of participants (50), it illustrates a new intervention model and will provide evidence on the impact of an income and wealth-supporting program much sooner than most baby bond programs, which require at least 18 years to reveal potential impacts.

This project was funded by the Black Economic Alliance Foundation. We are grateful to them and to all our funders, who make it possible for Urban to advance its mission.