In 2023, many families relied on credit and savings to meet their food needs. Families who were already facing food hardship were most likely to take on debt to pay for groceries, which could leave them less able to meet their basic needs in the future.

Why This Matters

Increases in the cost of essential goods, a pared-down social safety net, and increased borrowing costs left many families struggling to meet their financial needs in 2023. In such circumstances, families may turn to savings and credit to make ends meet. Although access to credit and savings can provide a lifeline and help families smooth consumption, overly relying on these resources may lead to financial instability if families have a hard time keeping up with debt or do not recover from using savings.

What We Found

Our analysis found the following about how families paid for groceries in 2023:

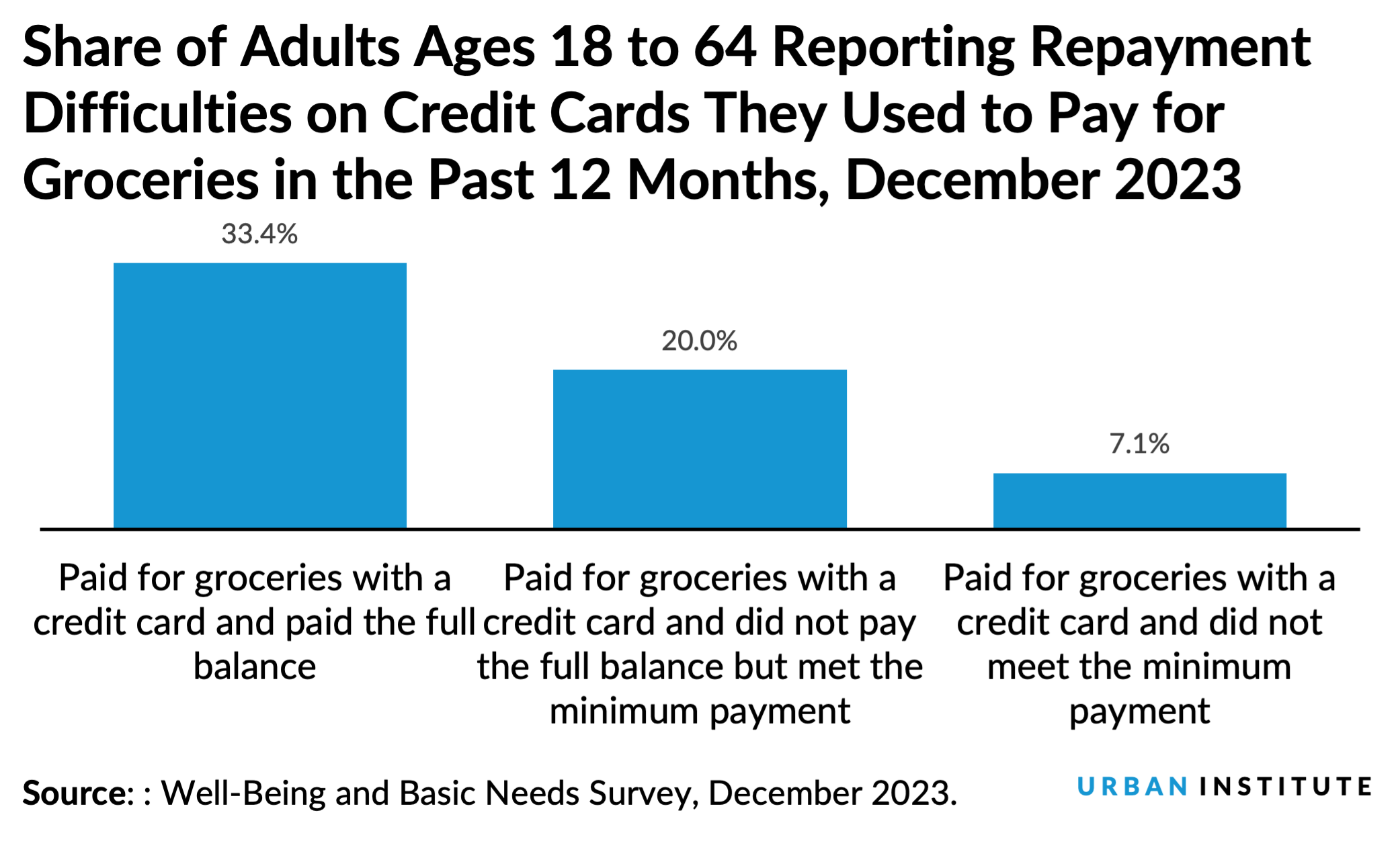

- Although 33.4 percent of adults paid for groceries with a credit card and repaid the bill in full, 20 percent of adults paid less than the full balance on a credit card but always made the minimum payment and 7.1 percent who did not make the minimum payment.

- More than one in six adults (17.8 percent) reported using Buy Now, Pay Later (BNPL) in the past 12 months, including 3.5 percent who reported using BNPL to pay for groceries. Thirty-seven percent of adults who used BNPL for groceries reported missing payments on these loans.

- Nearly one in five adults (19.3 percent) reported paying for groceries with savings that they did not intend to use for routine living expenses.

- Use of payday loans, BNPL options, and savings to pay for basic needs were increasingly common as households experienced greater levels of food insecurity. For instance, adults experiencing very low food security—the most severe form of food hardship—were more likely to report using BNPL to pay for any item (35.2 percent) or pay for groceries (11.5 percent); take out a payday loan (12.6 percent) or pay for groceries with a payday loan (10.0 percent); and draw down savings to pay for groceries (51.3 percent) relative to those reporting less severe food hardship.

- Adults with very low food security were also more likely to experience debt repayment challenges relative to those reporting less severe food hardship: nearly half paid for groceries with a credit card and either paid less than the full credit card balance (21.5 percent) or did not make the minimum required payment (24.7 percent). Half of adults with very low food security who paid for groceries with a BNPL option (11.5 percent) reported missing a payment (5.8 percent).

These findings show that many families used savings, credit from credit cards, BNPL, or payday loans to afford groceries, with families who already struggled to meet their food needs facing starker repayment challenges. Policymakers and practitioners could help families meet their basic needs without taking on high-cost debt by (1) increasing the sufficiency of the Supplemental Nutrition Assistance Program (SNAP) and other safety net supports; (2) expanding the set of financial options designed to extend credit to help families meet their needs; and (3) bolstering the credit counseling and debt management services available to families.

How We Did It

Our analysis draws on data from the Urban Institute’s Well-Being and Basic Needs Survey, a nationally representative internet-based survey of adults ages 18 to 64 designed to monitor changes in individual and family well-being as policymakers consider changes to federal safety net programs.