In the September 2024 edition of At a Glance, the Housing Finance Policy Center’s reference guide for mortgage and housing data, prepayment speeds have increased on recent mortgage originations, residential production reached the highest levels since January 2007, and Fannie Mae’s multifamily home serious delinquencies rose by 0.12% from June-to-July 2024.

Housing Cost Burdens Increased Most for the Lowest-Income Households

The cost of housing increased dramatically from 2019 to the present day. Rents grew by 30.4 percent nationally from 2019 to 2023, faster than wages over the same period (StreetEasy). Homebuying became much less affordable as both interest rates (page 9) and home values (page 24) increased. The share of monthly income that the median new homebuyer would spend on their mortgage increased from a low of 23.6 percent in August 2019 to a high of 39.9 percent in July 2023 (page 23), existing homeowners were less affected as they had locked in their mortgage rate, and many took advance of refinancing opportunities.

It is important to realize increased housing costs were experienced differently depending on household income and housing tenure. Urban’s recent analysis of American Community Survey data from 2019 to 2022 shows that households with low- to moderate-incomes experienced more drastic increases in housing cost burdens.

Cost Burdens Increased More for Renters and LMI Households

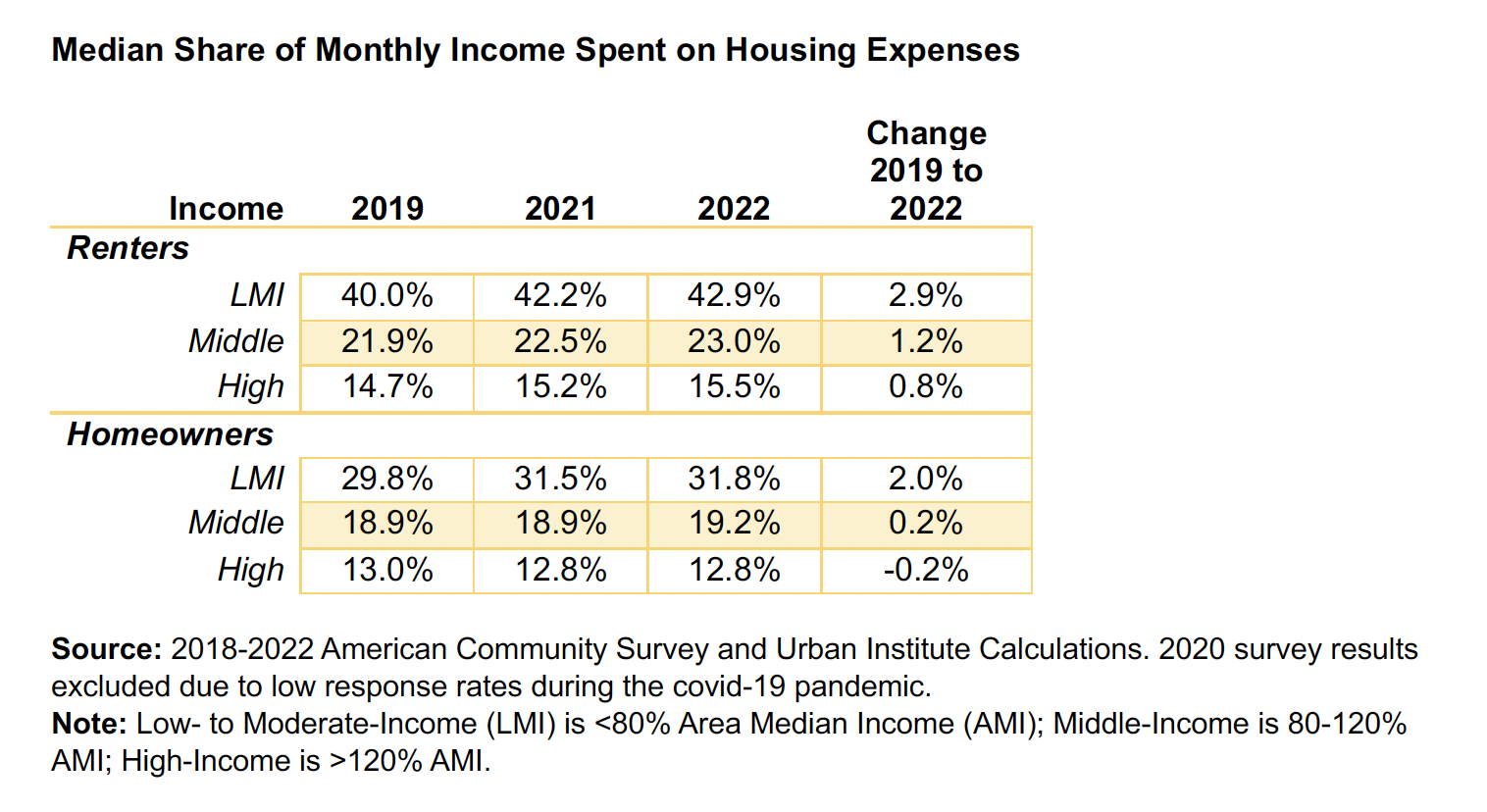

In 2019, low- to moderate-income (LMI) households were already spending a higher share of their income on housing compared to higher income households. The median LMI homeowner in 2019 spent 29.8 percent of their monthly income on housing, including , utilities and condo fees. At the same time, middle-income homeowners spent 18.9 percent and high-income homeowners spent 13.0 percent of their monthly incomes on housing.

For renters, this starting disparity was greater, with the median LMI renter household spending 40.0 percent of their monthly income on rent and utilities, and the highest income renters spent only 14.7 percent. Homeowners spend less of their monthly income on housing compared to renters within the same income group as homeowners have higher incomes than renters, even within these broad income categories.

Along with starting from a higher cost burden, housing cost burdens increased more for households with lower incomes. The median cost burden for LMI renters increased the most by 2.9 percentage points, from 40.0 to 42.9 percent in 2022. Over the same period, the median housing cost burden for high-income homeowners marginally decreased, from 13.0 to 12.8 percent. as so many took advantage of refinancing opportunities.

Cost Burdens Were Less Stable for Lower-Income Homeowners

One of the main benefits of homeownership, besides wealth building, is stable housing payments. Most homeowners in the US have 30-year fixed-rate mortgages; their monthly mortgage payments are set and only change if the homeowner decides to change them. Whereas renters can expect their housing costs to increase every few years as landlords often increase their rent whenever they sign a new lease.

However, the median cost burden for LMI homeowners increased more than the median cost burden for middle- or high-income renters from 2019 to 2022. Homeowners with low- to moderate-incomes were less likely to refinance their mortgage to a lower interest rate when the PMMS got to historic lows in 2020, and LMI homebuyers were more likely than middle- or high-income homebuyers to refinance in 2022 and 2023 when interest rates were high (Agarwal et al 2021 and August 2024 Chartbook, page 38). Most of these refinances are to cash out equity (page 11). This is a powerful tool for accessing cash when in need, however with current high interest rates, it can significantly increase the amount that homeowners will pay over the life of their mortgage and increase monthly mortgage payments.

These differences in how homeowners with different incomes react to changes in interest rates reduce the stability of housing payments for low-income households, and suggest that housing cost burdens are more apt to increase over time for LMI homeowners than others.