Higher Rates Reduce Affordability and Tighten Credit Standards

A new chart added to this month’s chartbook illustrates the decline in agency MBS holdings by the Federal Reserve and Commercial Banks. The actions by these market participants have helped to boost mortgage rates. A supposed silver lining is that credit standards remain easier than their levels in December 2021, just prior to most of the increase in interest rates. However, the increase in mortgage rates since then has outpaced the easing of median DTI over the same period suggesting that the DTI dimension has tightened. As a result, the impact of higher rates on homebuying affordability is being amplified by its impact on credit availability, further raising the barriers to homeownership.

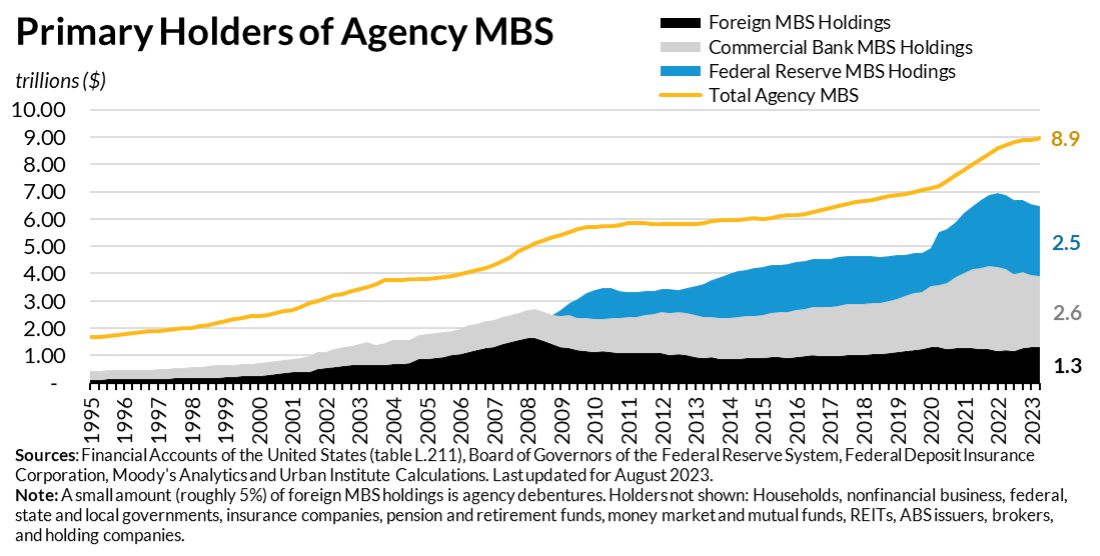

We have added a new figure the month titled Primary Holders of Agency MBS (page 7 of the chartbook). This chart clearly shows the decline in the holdings of agency MBS by the Federal Reserve and by Commercial Banks. This is offset by an increase in the holdings of all other asset holders which includes holders such as insurance companies, pension funds bond funds, mutual funds, and state and local governments shown in the table as the residual between total agency MBS and foreign MBS holdings, Commercial Bank MBS Holdings and Federal Reserve MBS Holdings).

The decline in agency MBS by the Federal Reserve reflects the run-off of agency MBS from its balance sheet; the Fed’s purchases of agency MBS have dropped to zero (page 35 of the chartbook). Commercial banks have also been largely selling agency MBS. Between the week of February 23, 2022 and the week of September 13, 2023, a roughly 1.5 year period, commercial bank holdings of agency MBS have decreased by 14 percent. In addition, spread widening was also influenced by the closures of Silicon Valley Bank and other banks, as well as uncertainty about the course of future federal reserve activity. Combined, the selling plus greater interest rate volatility has boosted the spread between primary mortgages and Treasury rates.

Pressure on mortgage rates has come from both the increase in spreads, but also by the increase in longer-term Treasury rates, reflecting the tightening of monetary policy. Rates have risen as the Fed has increased the federal funds rate and removed demand for longer-term Treasury securities.

Amid higher rates, credit standards for the median borrower remain easier (page 16 of the chartbook). The median FICO score at origination remains lower than its level in December 2021, just prior to the significant increase in interest rates. And both the median debt-to-income ratio (DTI) as well as the median loan-to-value ratio (LTV) remain above their December 2021 level.

However, this does not consider the impact of higher interest rates on DTI. Interest rates impact DTI because DTI includes the projected payment on the new home loan. All else equal, the rise in mortgage rates over 2022 and 2023 (page 9 of the chartbook) has exceeded the increase in the DTI. That is, mortgage rates have increased from 3.22 percent in early 2022 to 7.31 percent recently; bringing the monthly payment on a $350,000 mortgage from $1517 to $2407. For a borrower with $80,000 in income in early 2022, and a 8% increase over the interim period, this increase (without consideration of taxes or insurance on the home, or other debts) would raise mortgage the payment alone from 22.7 percent of total income to 33.4 percent. As a result, many prospective borrowers who might have been able to qualify for a mortgage prior to the run-up in mortgage rates, may find that their DTI is too high for qualification.

Although median FICO scores remain below their December 2021 level, they have been rising over 2023, increasing by 10 points to 743. In addition, house price growth has largely begun to rise again necessitating a larger down payment to maintain an LTV ratio. Against the backdrop of housing and financial market conditions, lending standards are tightening. And when combined with higher rates, is certainly making homebuying more difficult.