In the November 2024 edition of At A Glance, the Housing Finance Policy Center’s reference guide for mortgage and housing data, Year-over-year house price appreciation for the most expensive homes surpassed appreciation for the least expensive homes for the first time since March 2022, the number of mortgages with mortgage insurance is up from Q3, 2023, but the composition has shifted, with the FHA and VA share up, and the PMI share down, and the cashout share of refinances decreased by 20 percent over the last two months, this reflects decreasing rates from May to September 2024 and may reverse as interest rates have begun to climb.

New Chartbook Page for Prepayment Rates

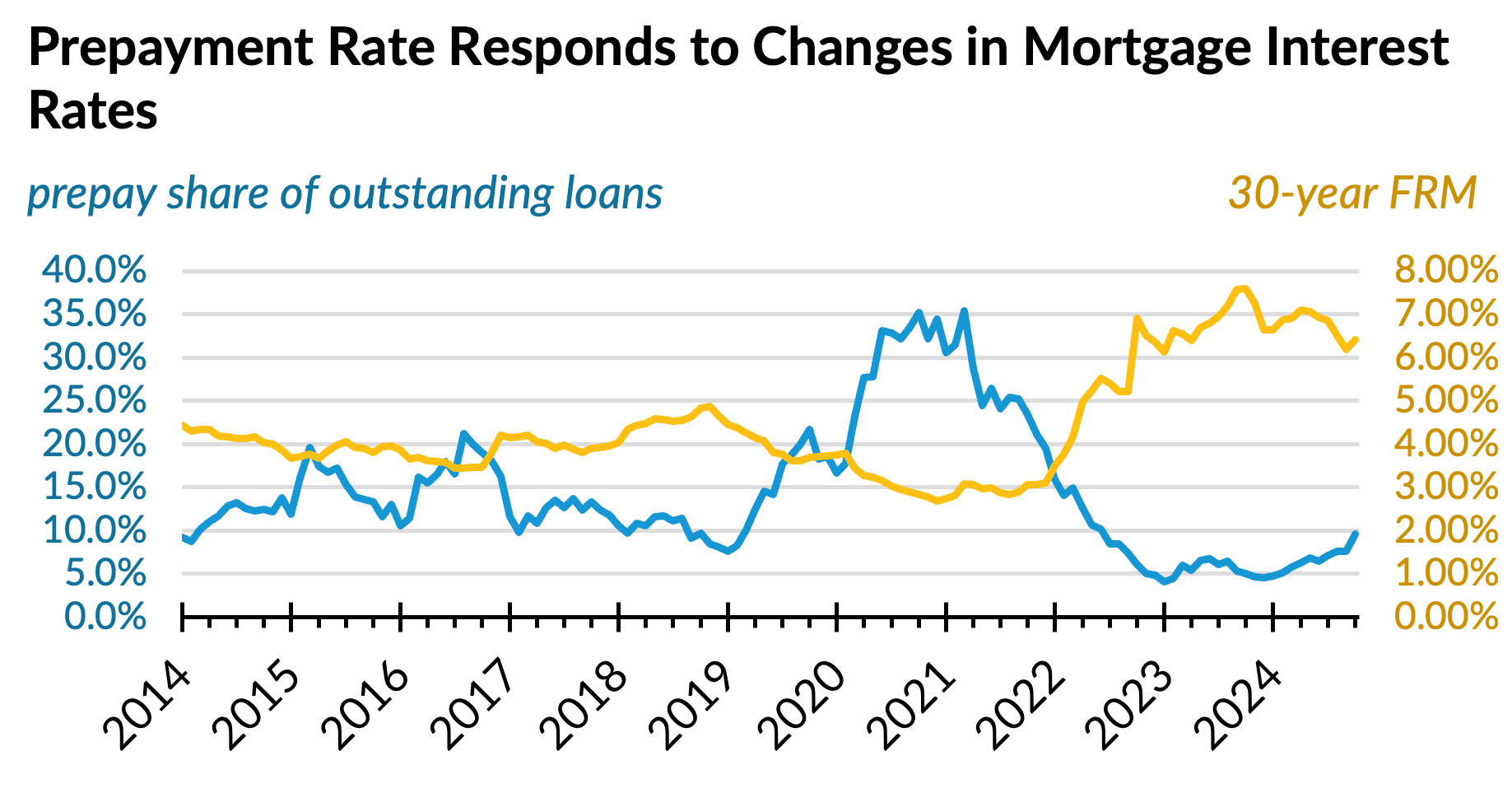

First appearing in the September 2024 edition of the Housing Finance At A Glance Monthly Chartbook, our newest page on prepayment rates with data from Recursion Co. shows the annualized prepay share of outstanding agency mortgages each month (page 11). Prepayments include all loans that are paid off entirely before maturity, this includes mortgage terminations due to both refinances and home sales. It also includes mortgages that were bought out from the securitized pool due to a loan modification or foreclosure proceeding.

Prepayment rates respond to changes in prevailing mortgage interest rates. As mortgage interest rates rise, prepayment rates fall and vice versa. From 2014 through 2018, the overall prepayment rate on outstanding agency loans fluctuated between 10 and 20 percent and averaged 13.1 percent per annum. As mortgage interest rates fell to historic lows over the Covid-19 pandemic, the prepayment rate reached a series high of 35.4 percent in March 2021. As mortgage interest rates increased rapidly over 2022, prepayment rates fell and reached a series low of 4.0 percent in January 2023. As mortgage rates remained elevated over 2023, the share of agency loans that prepaid in 2023 was 5.4 percent, much lower than the 2014-2018 average. Reflecting mortgage rate declines from May through September 2024, the prepayment share has increased over most of 2024 and stands at 9.6 percent in October 2024. However, the prevailing mortgage rate has increased on a weekly basis from September through November 2024 (page 9) which will likely lead to a reversal in prepayment rates in coming months.

Source: Recursion Co, Freddie Mac and Urban Institute Calculations. Data as of October 2024.

Note Rate

Most, 61.1 percent, of outstanding agency borrowers have mortgages with interest rates below 4.00 percent (page 10). Since the prevailing 30-year fixed rate mortgage (FRM) has remained over 6.00 percent since October 2022 (page 9), borrowers with lower interest rates would take a significantly higher rate on a new mortgage if they sold their home or refinanced. This pattern is often referred to as the lock-in effect. Because prepayments include both refinances and home sales, changes in prepayment rates can give us insight into changes in the lock-in effect. Even as interest rates fell over the 2024 Summer, prepayment rates on mortgages with interest rates of 5.00 percent or lower remained unchanged, because despite decreasing, the 30-year FRM has remained above 6.00 percent. However, prepayment rates on loans with interest rates above 5.00 percent increased dramatically as rates fell in 2024. Outstanding agency mortgages with interest rates 5.01 to 6.00 percent prepaid at a rate of 5.6 percent in December 2023 and increased over 2024 to 20.8 percent in October 2024. The prepayment rate on agency loans with interest rates over 6.00 percent increased from 8.1 percent in December 2023 to 36.5 percent in October 2024.

Agency

Ginnie Mae loans, especially VA mortgages generally have higher prepayment rates than loans backed by the GSEs. Part of this difference is likely because both FHA and VA have streamlined refinance programs. For a rate/term refinance, FHA and VA do not require a credit check or a new property appraisal. This makes the process quicker and easier. GSE refinances are essentially considered a new loan, where both a credit check and new appraisal is required. VA is faster than FHA as the VA funding fee on refinances is low; FHA borrowers must pay a new upfront mortgage insurance premium, although they may receive a credit from the fees on the old loan, depending on how long that loan has been outstanding. GSEs collect their loan level pricing adjustments on all refinances.

Vintage

Prepayment rates by vintage show the annualized prepayment share of outstanding loans by the year the loans were originated. Prepayment rates on mortgages originated in 2008 and before are less responsive to changes in interest rates than mortgages originated later over our time series. This is because most mortgages originated in 2008 and before that would have refinanced into a lower rate had likely already done so before our data begins in 2014. Mortgages that were originated before 2022 have low prepayment rates in 2023 and 2024. Many of these were low-rate mortgages originated in 2020 and 2021 because mortgages originated before 2019 had the opportunity to refinance at generationally low rates in 2020 and 2021 and hence did not respond to the interest rate decline over the Summer of 2024. However, Mortgages originated in 2022 and since were likely originated with high interest rates and did respond to the interest rate decline, rising from 4.9 percent in December 2023 to 17.2 percent in October 2024.