In the July 2024 edition of At A Glance, the Housing Finance Policy Center's reference guide for mortgage and housing data, house price appreciation slows, cash-out refinance volume remains tepid, and housing equity expands amid modest growth in mortgage debt outstanding.

HomeReady and Home Possible Programs Could Boost Affordability

In recent months, consumer inflation has shown signs of slowing. At the same time, labor market conditions remain healthy, reflecting solid economic growth. Amid these trends, market participants are betting that the Federal Reserve will cut its key policy rate later this year. In response, mortgage rates have begun to decline, decreasing nearly half a percent from their peak earlier this year. Lower rates could bring some relief to a market that has been historically unaffordable.

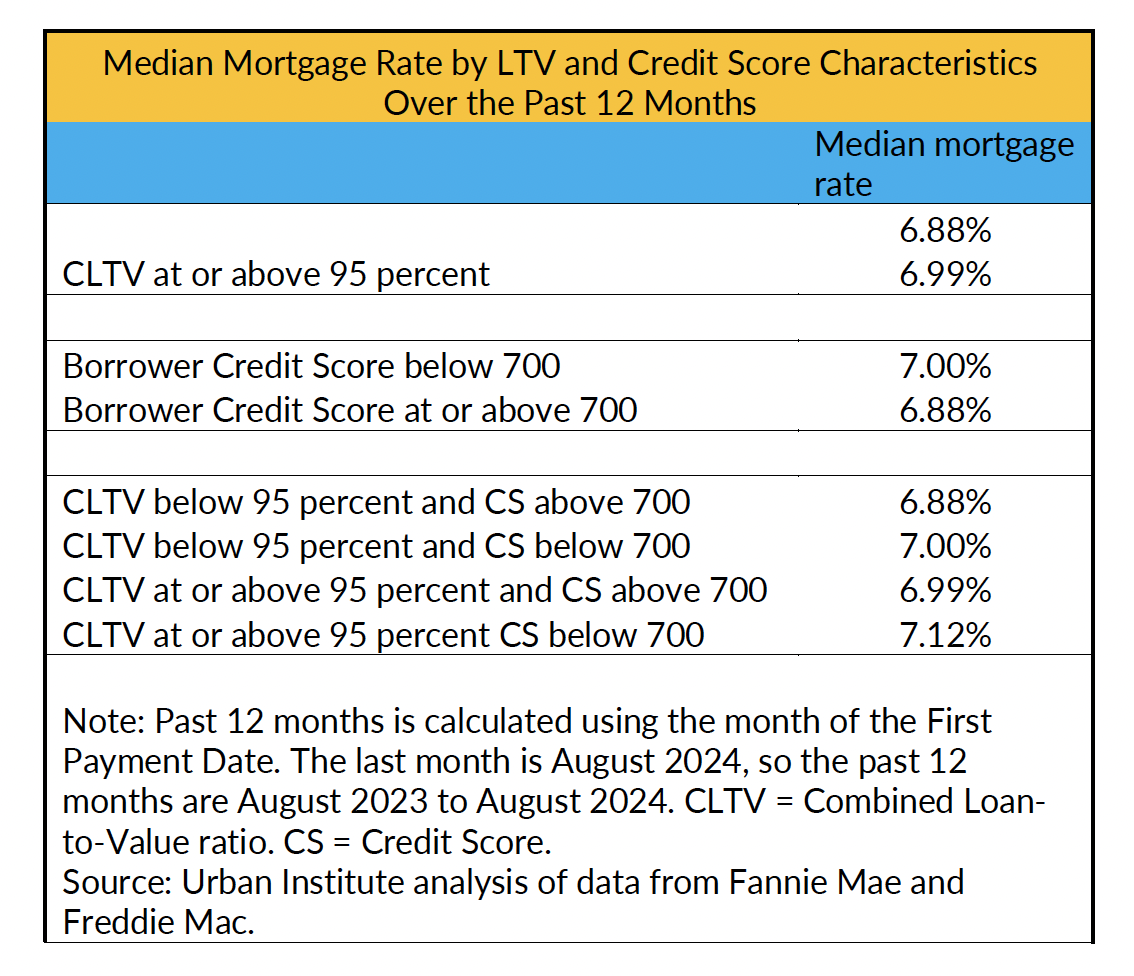

However, not all potential borrowers pay the same rate. Using loan level data from Fannie Mae and Freddie Mac and covering loans in 2024 indicates that the median borrower with a lower credit score, one at or below 700, obtains a higher mortgage rate compared to borrowers with a higher credit score. Similarly, the median borrower with a higher loan-to-value ratio (LTV), one at or above 95 percent, obtained a higher mortgage rate. This largely reflects the GSEs loan level pricing adjustments based on risk characteristics; these upfront charges are usually factored into the rate. (See page 30 of this chartbook for Fannie Mae’s LLPA matrix).

The government-sponsored enterprises Fannie Mae and Freddie Mac have developed programs for lower income borrowers, many of whom will have high LTVs and low credit scores. For example, under its HomeReady program, Fannie Mae provides mortgage credit, typically to buy a home, for lower-income borrowers with a combined LTV of up to 97 percent of a home’s sale price. And in some cases, a borrower can obtain up to 105 percent of a home’s purchase price if the subordinate lien is a Community Seconds loan. A community seconds loan is one where community, nonprofits and employers are a source of funding for closing costs as well as down payment assistance.

In addition, a borrower must have a credit score, but the score can be as low as 620, as long as there are other compensating factors. More recently, Fannie Mae announced that very low income borrowers in its HomeReady program can also receive a $2,500 credit to offset down payment or closing costs.

Freddie Mac’s Home Possible loan can be used by borrowers with a maximum LTV of 97 percent. In addition, borrowers can have a credit score as low as 660. And the Home Possible program provides a loan option for borrowers lacking a credit score, but this option requires a five percent down payment.

One important benefit of these programs is their impact on mortgage rates. Use of these programs will not incur any loan-level pricing adjustments (LLPAs).

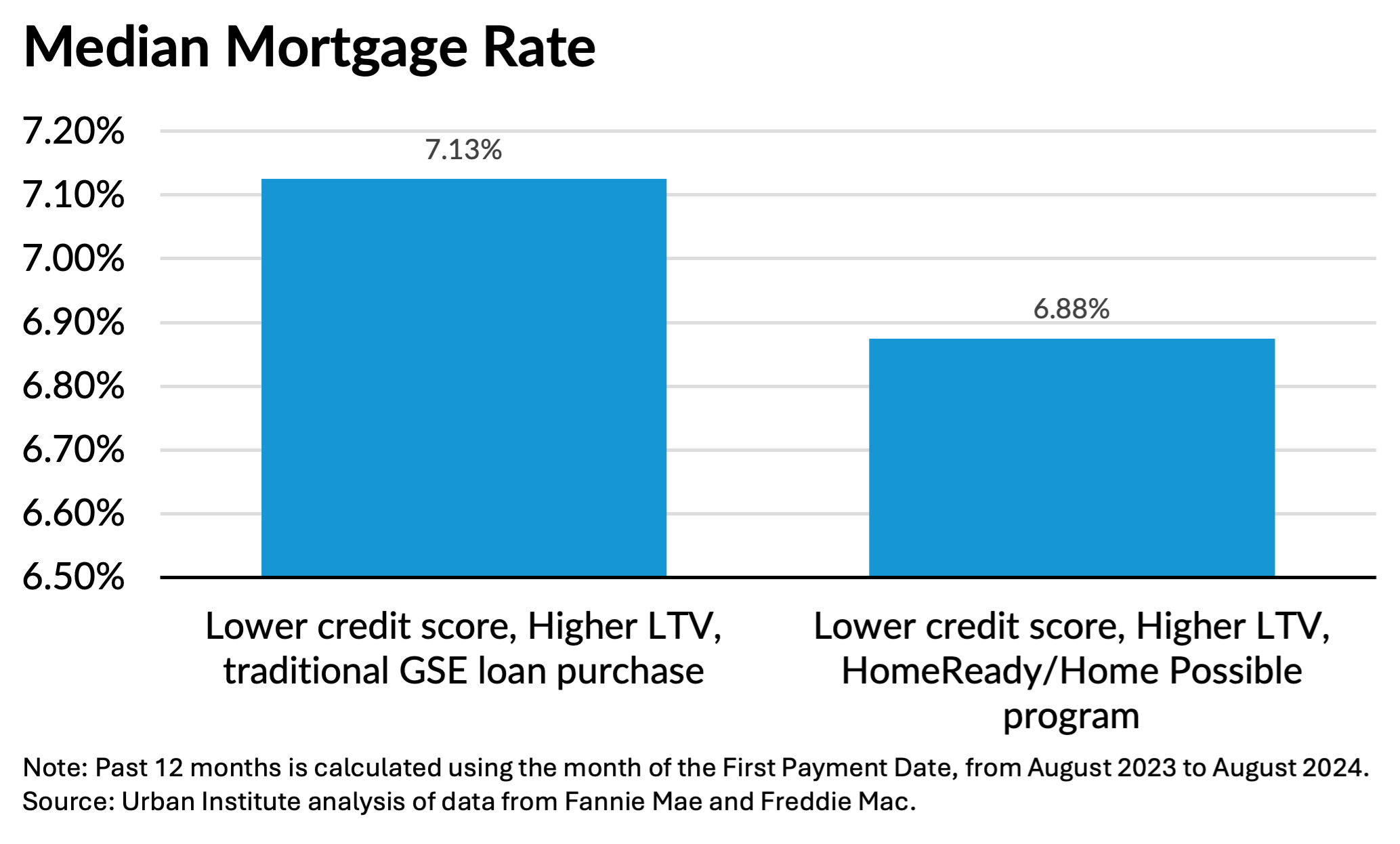

Analysis of Fannie Mae and Freddie Mac purchase loans in 2024 suggests that the median borrower in HomeReady or Home Possible obtained a lower mortgage rate compared to similar borrowers in a traditional Fannie or Freddie purchased loan. The table above compares borrowers with a credit score below 700 and combined LTV of 95 percent of higher that are also in either the HomeReady or Home Possible program with borrowers existing in similar LTV and credit score buckets, but not in any GSE program.

These results suggest that borrowers with fewer financial resources and a lower credit score could take advantage of the HomeReady or Home Possible programs. And in turn, these programs could modestly boost affordability and strengthen homeowner sustainability. Lower income borrowers have historically turned to FHA mortgages, still a very viable alternative. They should compare the execution, and choose the rate that is more favorable for them (see page 36 of this chartbook for an example). This is especially important now, because lower rates can potentially move more renters into range where they can afford homeownership.