Congress passed enhanced premium tax credits (PTCs) in March 2021 as part of the American Rescue Plan Act and extended them through 2025 by the Inflation Reduction Act of 2022. The enhanced PTCs substantially increased the subsidies available to buy insurance in the Marketplace, making coverage more affordable for eligible people. As a result, enrollment steadily increased and jumped by 5 million people, or 31 percent, during the 2024 open enrollment period. Soon, Congress will debate whether to extend enhanced PTCs again, make them permanent, or let them expire.

In this summary, we estimate household premiums for people with Marketplace coverage in 2025 with and without enhanced PTCs by income and state to gauge the impact on families if the more generous credits were to expire. When estimating coverage under a policy without enhanced PTCs, we assume an alternate scenario in which the original Affordable Care Act PTCs would have remained in effect.

Why This Matters

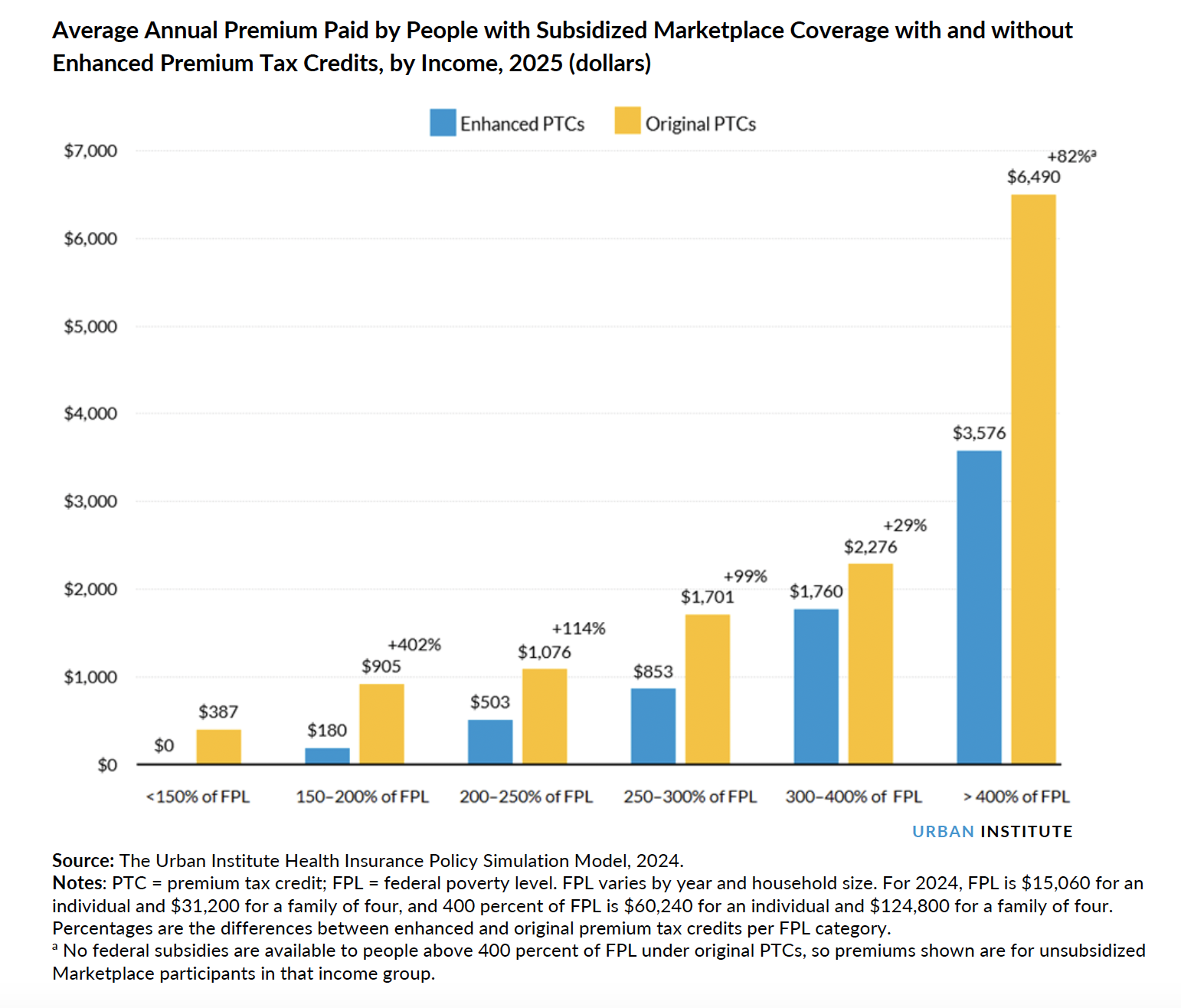

Without the enhanced PTCs, households with incomes below 400 percent of the federal poverty level (FPL) would be required to pay a greater share of their income towards premiums, while households with higher incomes would lose eligibility for PTCs and be responsible for the entire premium. As a result, required family contributions for Marketplace coverage would be sharply higher. Some people would drop coverage; those who keep coverage would be more financially burdened.

What We Found

Our key findings are as follows:

- Without enhanced PTCs, Marketplace participants with very low incomes (less than 150 percent of FPL) would pay an average of $387 per year in premiums; under enhanced PTCs, they would pay no premium.

- Without enhanced PTCs, people with Marketplace coverage and incomes between 150 and 200 percent of FPL will see their average premium increase from $160 to $905 per year.

- The average person with an income above 400 percent of FPL, who would lose eligibility for PTCs, would pay over $2,900 more in premiums if they keep Marketplace coverage.

- If enhanced PTCs expire, increases in household premiums will vary by state and geographic area. For people with incomes below 250 percent of FPL, the average annual increase in premiums if enhanced PTCs were to expire ranges from $193 in New Mexico to $924 in Alaska. For people with incomes above 250 percent of FPL, the premium increase would range from $119 per year in West Virginia to $1,434 in California.