Maryland’s taxes looked very different after Martin O’Malley’s eight years as governor. Income tax changes made the state’s tax system more progressive, but sales tax increases moved things the other way. While O’Malley has not yet released a formal tax plan as a presidential candidate, we know he made several tax changes as governor.

When O’Malley assumed office in 2007, the state’s individual income tax was essentially flat—there were four tax rates, but the 4.75 percent top rate started at just $3,000 in annual taxable income.

By 2015, Maryland tax had eight brackets and a higher top tax rate of 5.75 percent on taxable incomes above $250,000. O’Malley and the legislature also increased Maryland’s personal exemption from $2,400 to $3,200 and the state’s earned income tax credit from 20 percent to 25 percent of the federal credit.

Most of the personal income tax changes—as well as an increase in Maryland’s corporate income tax from 7.0 percent to 8.25 percent—came about through the Tax Reform Act of 2007, when the governor and the legislature worked together to address the state’s structural budget deficit.

The act also levied a sales tax on computer services, but public backlash resulted in repeal the following year. A temporary 6.25 percent surtax rate on personal income above $1 million took its place and expired on schedule in 2011.

O’Malley and the legislature increased income taxes again in 2012, arguing that the state needed more revenue to maintain education spending.

In all, Maryland’s income tax became significantly more progressive during O’Malley’s term. But there were regressive tax increases, too. The 2007 Tax Reform Act also raised the state sales tax from 5 percent to 6 percent, and the cigarette tax from $1 per pack to $2 per pack. In 2011, the state’s alcohol tax went from 6 percent to 9 percent and two years later, annual inflation-adjusted gas tax increases were created as part of a larger transportation bill.

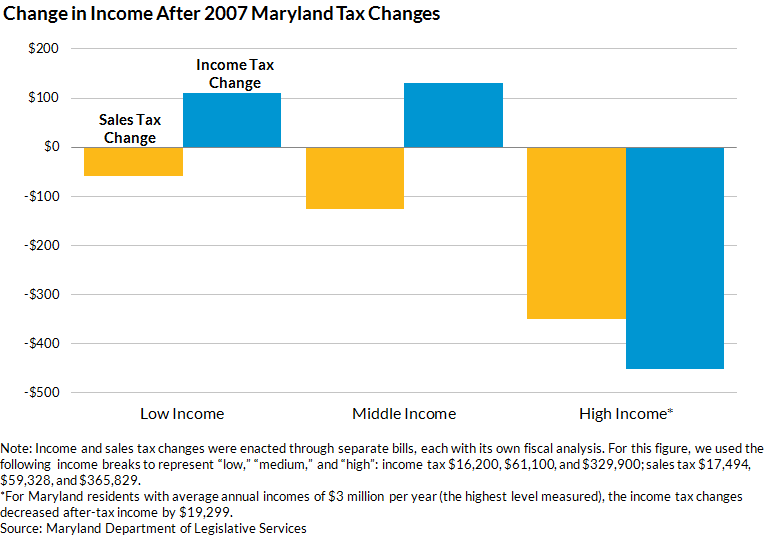

There is no official tax incidence report for all of the tax changes that occurred during O’Malley’s term. However, Maryland’s Department of Legislative Services estimated the income tax changes in the 2007 Tax Reform Act reduced the average state and local taxes paid by Marylanders earning less than $100,000 a year but raised them for residents earning above that.

Meanwhile, the sales tax hike raised taxes on all Marylanders. For residents earning less than $100,000, the tax decrease was generally larger than the tax increase.

This is one in a series of posts from the Urban Institute’s State and Local Finance Initiative examining the records of current and former governors running for president.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.