The federal tax code allows homeowners to write off mortgage interest payments from their income before calculating their tax bill. Although it’s old news for tax- and housing-policy wonks that homeowners are getting federal subsidy payments, it may surprise others who assume that the federal government’s housing assistance goes mostly to low-income renters.

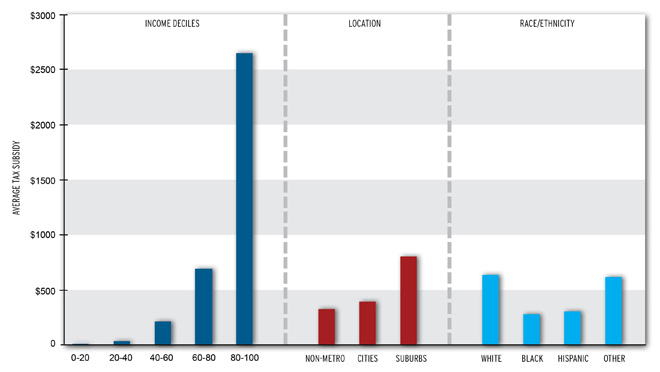

The mortgage interest deduction adds up to a lot of money – an estimated $131 billion in 2012. That dwarfs total spending by the Department of Housing and Urban Development (under $50 billion). The biggest tax benefits go to high-income homeowners who’ve taken out big mortgages for expensive homes. Recent results from the Urban Brookings Tax Policy Model show that means affluent white families living in the suburbs, not the low- or moderate-income people who are struggling to buy homes or make ends meet or the central city neighborhoods that need reinvestment.

Distribution of Benefits from the Mortgage Interest Deduction

For decades, low-income housing experts and advocates have argued that the mortgage deduction should be scaled back or restructured and that the extra tax revenues should go to housing programs that help poor people. There’s ample evidence of enormous need. But the mortgage interest deduction has been too popular among affluent homeowners and the real estate industry to touch.

Now, however, the federal debt crisis may intensify pressures for increased revenue so much that even the mortgage interest deduction gets serious consideration. Next week, tax policy experts, housing advocates, and real estate industry reps meet at the Urban Institute to debate the deduction’s future.

What should that future look like? Should we just eliminate the mortgage interest deduction to raise more revenue and simplify the tax code? Some may argue that the tax code should be purged of social policy incentives, but I think that’s unrealistic. Instead, if we’ve finally got a real reform opportunity, let’s redirect at least some of the tax savings from the mortgage interest deduction to help families and neighborhoods with serious housing needs, rather than the richest homeowners in the affluent suburbs.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.