As homeownership rates have dropped to their lowest levels since 1994, more and more families are turning to renting. But those actually aren’t the only two options, or at least not as conventionally understood. For individuals and families who don’t struggle to pay their monthly bills, but find homeownership out of reach, shared equity can provide the bridge to their first home.

Shared equity is a model that allows income-eligible families to buy homes at below-market prices. In return, the owner’s potential capital gains from selling the home are restricted. Under this approach—which is different from a shared appreciation mortgage—the market cost of the home is shared between the buyer and the entity administering the program, and the program keeps a share of the equity. When the buyer later sells the house, the buyer is able to access a share of the profits, but the house will remain affordable to the benefit the next low-income homebuyer. Shared equity is a broad designation that includes the following community land trusts and deed restricted programs (e.g. inclusionary zoning).

As part of an ongoing six-year impact study, we are releasing baseline findings on shared equity homeownership programs in nine metro areas. Our baseline report details the people interested in these programs.

Individuals and families interested in affordable homeownership programs often live in market-rate rental units. They don’t necessarily struggle to pay their rent each month, but their limited income prevents them from saving enough for a down-payment or sustaining monthly payments on a market-priced home.

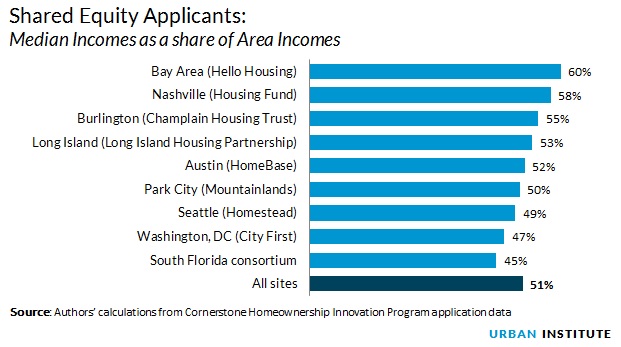

Across the sites, applicants’ median incomes were just 45 to 60 percent of the median income in their area. Most homeowners with conventional mortgages earn more than 100 percent of the median income in their area, so shared equity applicants are considerably lower income than market-rate homebuyers.

Notwithstanding their modest incomes, shared equity applicants are highly educated: 70 percent have a college degree. Most are in their 30s and working full time for moderate wages in jobs like office administration and healthcare that, though stable, do not pay enough to support buying a market-rate home. And the data show that they have little or no net worth on average.

Public assistance programs generally target very low-income families that struggle to pay for food or shelter on a regular basis. Shared equity homeownership targets a group that is often overlooked: families whose incomes are stable, but insufficient to enter the homeownership market.

High-cost housing markets are best suited to the shared equity model—for example, the Bay Area and Washington, DC, as well as places like Park City, Utah, where the cost of vacation homes drives up house prices for local residents.

What’s more, shared equity buyers tend to move into market-rate homeownership after they’ve built equity in their initial home. Shared equity homeownership programs not only allow more people to buy homes, they also give families a stepping stone to greater opportunity.

Tune in and subscribe today.

The Urban Institute podcast, Evidence in Action, inspires changemakers to lead with evidence and act with equity. Cohosted by Urban President Sarah Rosen Wartell and Executive Vice President Kimberlyn Leary, every episode features in-depth discussions with experts and leaders on topics ranging from how to advance equity, to designing innovative solutions that achieve community impact, to what it means to practice evidence-based leadership.