When Dave Stevens, head of the Mortgage Bankers Association (MBA), claimed that the GSEs denied 56 percent of black mortgage applicants, many, including Fannie Mae, responded that MBA’s numbers overestimated the denial rate for minorities. But our numbers show that even the MBA’s denial rate underestimated the tightness of the GSE market. Preserving the status quo of GSEs is not enough to provide needed credit to borrowers with weaker credit profiles, including many minority applicants.

Denial rate only matters for weaker credit profile applicants

The Home Mortgage Disclosure Act (HMDA) is the source for mortgage application data. From HMDA, it is possible to calculate the denial rate for all mortgage applicants. However, HMDA does not include applicant credit profiles, a critical omission since applicants with a strong credit profile are unlikely to be denied. So the denial rate really only matters for weaker credit profile applicants. Including applicants who have no chance being denied in the denial rate calculation gives a false impression of what is happening in the mortgage market. As we show below, denial rates for weaker credit profile applicants are much higher than the denial rates for all applicants.

GSE denial rates for weaker credit profile applicants

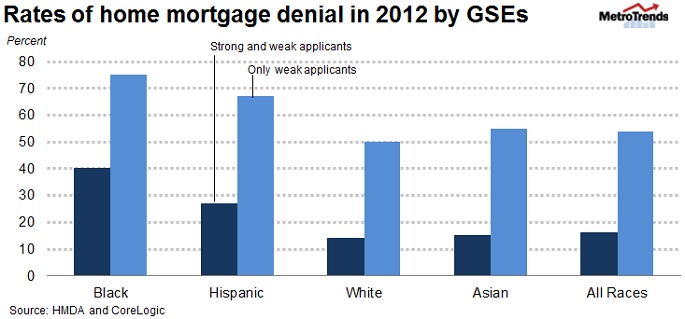

According to HMDA, at least 16 percent were denied GSE loans for purchase of an owner-occupied property in 2012; but by matching HMDA’s data with CoreLogic’s, we found that the denial rate for low credit profile applicants of GSE loans was at least 54 percent (See below for the details of the calculation). By race and ethnicity, in 2012, at least 40 percent of all African American applicants, 27 percent of Hispanic, 14 percent of white and 15 percent of Asian applicants were denied GSE loans. Yet of low credit profile applicants, at least 75 percent of African American applicants were denied GSE loans, 67 percent of Hispanic, 50 percent of white and 55 percent of Asian. In 2001 (a pre-bubble year), at least 37 percent of African Americans were denied GSE loans, as were 25 percent of Hispanics, 15 percent of whites and 11 percent of Asians. But if we narrow down to applicants of GSE loans with weaker credit profiles, these denial rates jump to at least 56 percent, 49 percent, 42 percent and 35 percent.

The ultimate point of Stevens' remarks was to assert that GSE reform is needed in part because minority borrowers are not currently being well served by the GSEs. Our numbers show that the GSE market is excluding the majority of borrowers with weaker credit profiles, including but not limited to African Americans.

Okay, housing data lovers: here’s how we did our calculations

According to HMDA, in 2012 there were a total of 1,552,897 completed applications for purchase of an owner-occupied property with a conventional loan (including GSE, portfolio and private labeled security loans). Of these, 255,834 were denied, and 1,297,063 approved, a 16 percent denial rate. Of the 1,552,897 conventional loan applications, a number, Y, of these applications is intended to GSE loans. In fact, to maintain liquidity, lenders try to sell as many as possible if not all of their loans to GSEs.

If the applications don’t meet the GSE’s lending standards or have repurchase risk, the loan application is either denied, originated and sold in the private labeled security market, or originated and kept in the institution’s own portfolios. In any case, this preference suggests that the denial rate for GSE loan applications would be higher than that of the other conventional channels. The 16 percent denial rate for all applications can be treated as the lower boundary of GSE’s; and this treatment applies to other calculated denial rates for GSEs.

Assuming loan application denial is solely based on credit-worthiness (a reasonable assumption, although undoubtedly some applicants were denied for other reasons), all 0.16*Y denied loan applicants should be applicants with weaker credit profiles. We matched the loans HMDA showed as having been made with loans in the CoreLogic Prime Servicing database, but the matched data shows that only 17 percent of the originated loans that were purchased by the GSEs were made to weak credit profile borrowers.

We defined weak credit profile at origination as a borrower who takes out a loan with either a combined loan to value ratio (CLTV) above 90, a back-end debt to income ratio (DTI) above 45, or a CLTV below 90 and DTI below 45 but with a FICO credit score below 680. Using this definition, there are (1-0.17)*(1-0.16)*Y high credit profile borrowers of GSE loans, which should equal the total number of high credit profile applicants of GSE loans, given our assumption that high credit profile applicants have zero chance being denied.

Then, the number of low credit profile applicants equals X- [(1-0.17)*(1-0.16)*Y], and the denial rate for low credit profile applicants equals 0.16*Y/{Y-[(1-0.17)*(1-0.16)*Y]}=0.16/{1-(1-0.17)*(1-0.16)}=0.16/0.3, which is 54 percent, versus the 16 percent overall denial rate for all applicants. We similarly calculated the denial rate for weak credit profile applicants by races and ethnicities for 2012 and 2001.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.