<p>Finished brick homes in the Newport News Housing project for African American families are pictured in October 1937. Photo by John Vachon via Shutterstock.</p>

Black History Month celebrates the progress toward racial equality the United States has achieved and reminds us of the work that remains. Gains in black homeownership have been hard won, which amplifies our concern that in the last 15 years, black homeownership rates have declined to levels not seen since the 1960s, when private race-based discrimination was legal.

Unless this setback to black homeownership is addressed, black families will rent for more years before homeownership than they did a few years ago. This will shrink the landscape of housing choice available to black families, increase their exposure to displacement, and delay or close off a key wealth-building mechanism. All three of these outcomes will widen the inequality that underlies so many current struggles.

What has happened to black homeownership?

The black community was hit harder than other groups by the housing crisis

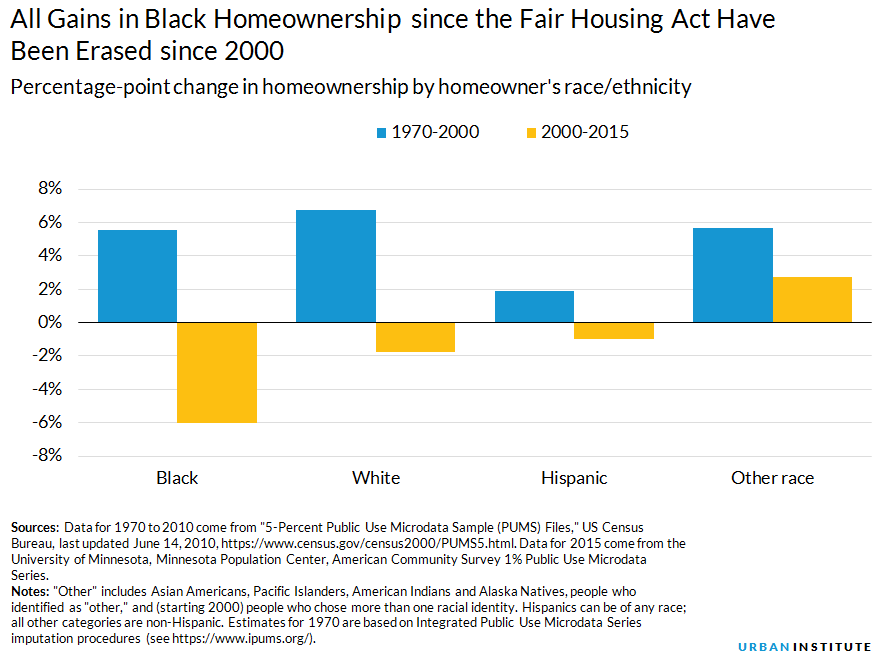

In the three decades after the Fair Housing Act passed, black homeownership rose by almost six percentage points. But from 2000 to 2015, that gain was more than erased as forces within and beyond the housing market aligned to reduce the black homeownership rate to 41.2 percent. Black homebuyers bought homes at the peak of the bubble at higher rates than whites and Asians, having often been offered subprime loans even when they qualified for prime loans.

Black families did not benefit on average as much as their white counterparts from the post-9/11 economic recovery. As a result, the black homeownership rate dropped more than 2 percentage points from 2000 to 2010 and slid even faster after 2010. White and Hispanic homeownership dropped less from 2000 to 2015, and homeownership rose for people in other racial groups (mainly Asian Americans). Click here to download more detailed data on black homeownership.

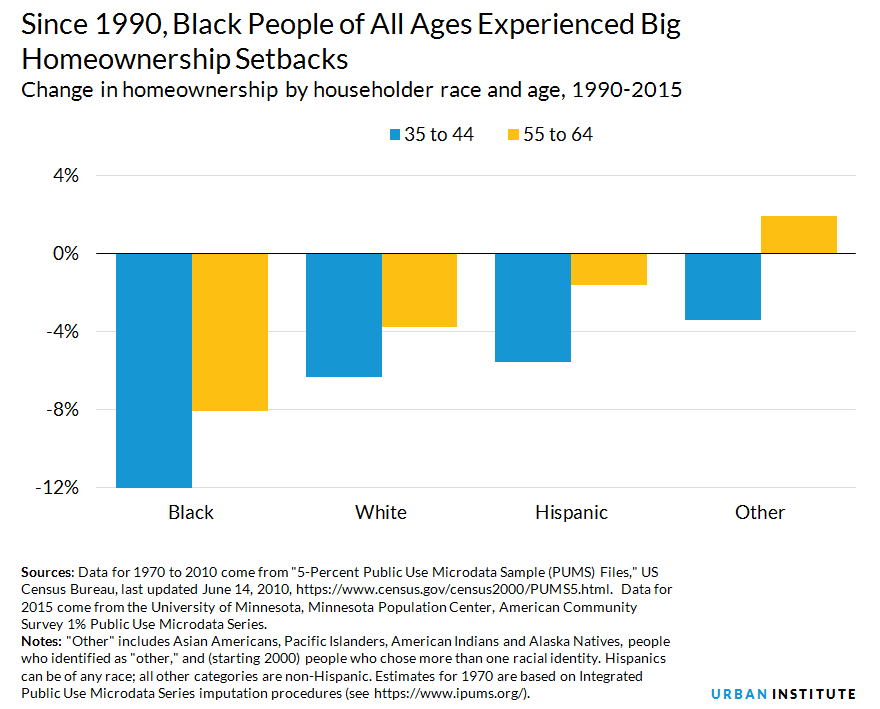

Big homeownership declines for black households of all ages, especially young adults

The decline in homeownership has been most marked for younger members of the black community. The homeownership rate for black 35- to 44-year-olds fell from 45 percent in 1990 to 33 percent in 2015, half the level for whites of the same age and lower than the black homeownership rate in 1960. Homeownership also fell from 1990 to 2015 for whites, Hispanics, and others in that same age group, but not by nearly as much as for black people. Among 55- to 64-year-olds, black homeownership fell 8.1 percent, while homeownership for white and Hispanic households of the same age fell 3.7 and 2.1 percent, respectively.

An unprecedented generational retrocession

The history of homeownership by generation is particularly troubling. This view shows that the prospects for black homeownership have gone from hopeful to pessimistic in only 15 years.

About half of black people born in the last 10 years of the baby boom (1956–65) were homeowners by the time they turned 50. The early gen Xers (born 1966–75) had a higher homeownership rate in 2000 (when they were in their late 20s and early 30s) than the late boomers had enjoyed 10 years earlier. But the financial and housing crisis slowed early gen Xers’ transition into homeownership from 2000 to 2010 (when they were in their 30s and early 40s) and caused more of this generation to lose their homes than to become owners after 2010. This retrocession is unprecedented for any other generation or age group.

The picture only gets worse for younger black generations. Those born from 1976 to 1985—spanning late gen Xers and early millennials—have barely begun their homeownership transition, but they’re getting an even slower start than either of the two older cohorts.

Inequality will get worse with inaction

The overall decline in homeownership threatens to exacerbate racial inequality for decades to come. If recent trends continue, black people born between 1965 and 1975 will likely become part of the first generation since those born before 1900 to reach retirement age with more renters than homeowners among their community.

The period since the housing crisis began has been a tragic chapter in the history of the black community’s access to the wealth building, security, and the sense of belonging offered by homeownership. We must take action to avoid further decline. Reforms are needed that provide more affordable rental housing and more plentiful and secure access to homeownership.

These reforms need to go beyond housing to include safe and healthy neighborhoods, high-quality education, measures to build and protect financial health, fair credit scoring, and access to good jobs and affordable health care. These influences will affect whether today’s youngest generations will be homeowners by the time they retire.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.