Now that Bank of America has pulled back its fees for debit-card holders, let’s turn to those who are really on the outside looking in at mainstream financial services: American consumers with no bank account at all. As measured by the FDIC’s January 2009 survey, 7.7 percent of U.S. households are unbanked. That’s 17 million adults. Another 17.9 percent of households—some 43 million adults—are underbanked. They have bank accounts, but still make some use of payday loans, pawnshops, and other alternative financial products.

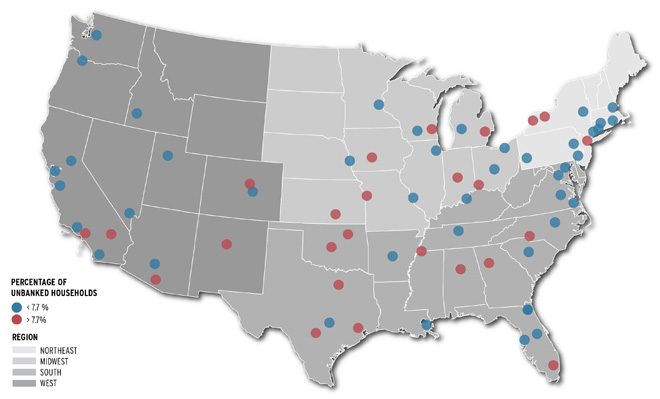

The unbanked population is predominantly urban. Fully 81 percent of unbanked households reside in Metropolitan Statistical Areas (MSAs). If we look at the unbanked rates of very large MSAs that are also represented in the FDIC survey by at least 100 sample households, we find that 25 of these 69 metros have unbanked rates above the 7.7 percent national average.

All Regions Contain Large MSAs With High Unbanked Rates

Among these high-need areas, Memphis ranks highest at 17.3 percent. Indeed, three-fourths of its Census tracts have unbanked rates exceeding the 7.7 percent benchmark, according to recent estimates by Corporation for Enterprise Development (CFED)—which has just released a powerful data tool for researching local patterns of bank use.

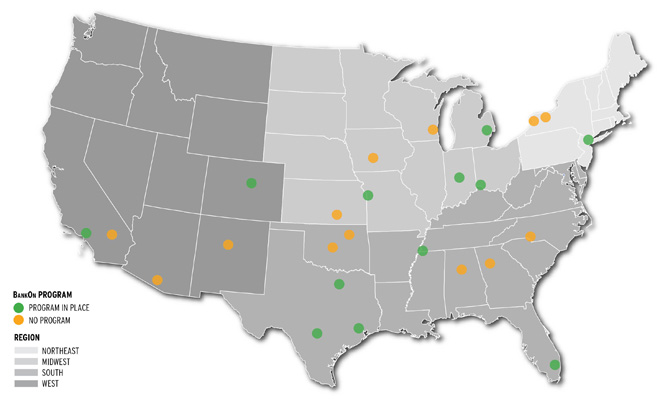

In the past five years CFED has also supported the creation of BankOn initiatives. These public-private partnerships promote access to mainstream retail financial services by negotiating with banks and credit unions to get them to offer starter or “second-chance” accounts. Among the 56 such programs up and running now, most focus on a core city or metro area while others are state or county entities.

How well do BankOn programs cover the neediest metro areas? Quite simply, much has been accomplished and much remains to be done. Of the 25 high-need MSAs, only 12 have a BankOn program.

BankOn Initiatives Are Widespread, But Do Not Reach Many High-Need MSAs

Among the 13 others are some with unbanked rates as high as Tulsa’s 12.6 percent.

Because most financial services providers work in a particular state or region, we need to develop strategies to better serve the unbanked residents of the high-need communities they serve. That means concentrating on the interior southwest (Riverside, Tucson, and Albuquerque), the central plains (Wichita, Tulsa, Oklahoma City, and Des Moines), the Great Lakes (Milwaukee, Buffalo, and Rochester), and the interior southeast (Birmingham, Atlanta, and Charlotte). BTW: Charlotte is Bank of America’s corporate headquarters.

Willie Sutton robbed banks because “that’s where the money is.” Banks, credit unions, and other mainstream institutions need to reach the underserved segments of their retail markets because that’s where the need and opportunity are.

Tune in and subscribe today.

The Urban Institute podcast, Evidence in Action, inspires changemakers to lead with evidence and act with equity. Cohosted by Urban President Sarah Rosen Wartell and Executive Vice President Kimberlyn Leary, every episode features in-depth discussions with experts and leaders on topics ranging from how to advance equity, to designing innovative solutions that achieve community impact, to what it means to practice evidence-based leadership.