A market composition change—not lower lending standards—explains the decrease in average credit scores for conventional and FHA mortgages. Despite rising home prices and gradual housing recovery, the mortgage lending rules have remained tight, inhibiting housing demand and economic growth.

Recent reports have suggested that the lower average credit scores for purchase loans might mean that the tight credit box is finally starting to expand. The Wall Street Journal noted that credit scores for borrowers seeking conventional mortgages and Federal Housing Administration (FHA) loans are easing because “scores on purchase mortgages stood at 755 in March, down from 761 a year earlier, according to data from Ellie Mae, a mortgage-software provider. Those on purchase loans backed by the FHA dropped to 684, compared with 696 one year earlier.”

Consistent with the WSJ findings, our analysis shows credit scores on conventional mortgages sold to government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac averaged 752, down from 758 a year earlier. Credit scores on purchase loans backed by FHA declined even more, averaging 686, a 11-point drop down from 697.

But pooling the loans together reveals that credit scores actually remained the same. The average credit score of all purchase loans stayed around 730 during the one-year period—no actual credit easing.

But if the credit is still tight, what’s causing GSE and FHA credit scores to both go down? The FHA is losing market share to private mortgage insurers (PMIs), which provide insurance for GSE loans with loan to value (LTV) ratio above 80. That lost share primarily consists of higher FICO borrowers (higher by the FHA standards, though not so by the GSE standards). The FHA does not do risk-based pricing and has raised insurance premiums several times since 2009, whereas private mortgage insurers vary premiums and GSE-imposed loan-level pricing adjustments (LLPAs) by credit score. For borrowers with high FICO scores, especially scores above 680, PMI’s risk-based rates make borrowing through the GSEs more favorable than through the FHA.

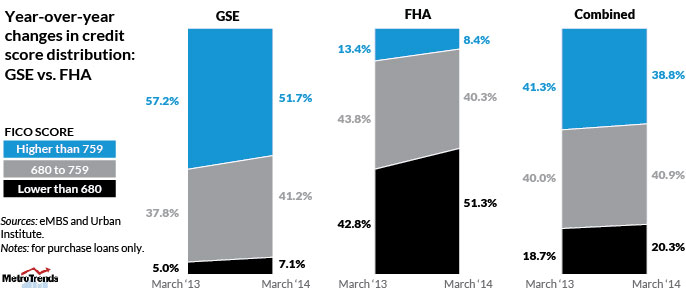

As a result, the FHA is losing borrowers at the higher end of its credit score spectrum and lowering its average credit score. The GSEs are absorbing borrowers at the lower end of their credit spectrum, also dragging their average score down (figure 2). The average FHA credit score declined year over year, and in March 2014, the share of borrowers in the 680-759 and 760-plus higher credit score brackets dropped from last year’s 44 percent and 13 percent to 40 percent and 8 percent respectively. The GSE’s former average credit score of about 758 also fell, with its share of 680-759 credit score borrowers increasing from 38 percent to 41 percent.

But credit standards aren’t declining. The credit score distribution for the market as a whole is largely unchanged. Most of the buzz about credit score declines in GSE and FHA loans are due to higher FICO score borrowers now choosing GSE lending over FHA—shifting the market share and reducing the credit scores of both.

Tune in and subscribe today.

The Urban Institute podcast, Evidence in Action, inspires changemakers to lead with evidence and act with equity. Cohosted by Urban President Sarah Rosen Wartell and Executive Vice President Kimberlyn Leary, every episode features in-depth discussions with experts and leaders on topics ranging from how to advance equity, to designing innovative solutions that achieve community impact, to what it means to practice evidence-based leadership.