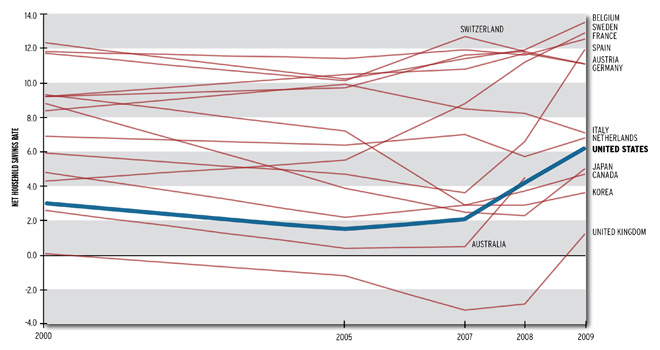

American households save far less than their counterparts in other OECD countries. In his insightful new book, Beyond Our Means: Why America Spends While the World Saves, Princeton historian Sheldon Garon puts our low net savings rate in perspective. Yes, it trended upward during the 2000s, but it’s still less than half of the double-digit rates in such economically robust European countries as Austria, Belgium, France, Germany, Sweden, and Switzerland.

Net Household Saving Rates For Selected OECD Countries, 2000-2009 (Percent Of Disposable Household Income)

Source: Sheldon Garon, Beyond Our Means: Why America Spends So Much While The World Saves

As for why, Garon points to institutions that emerged in Britain, continental Europe, and the Far East during the 19th and early 20th centuries to promote small-dollar savings among younger generations and the working class. Thrift was bred through savings banks in schools, post offices, and other community institutions. We saw their like here in the Northeast and Upper Midwest, reinforced by patriotic savings campaigns during World Wars I and II. Yet, our government has never nurtured saving behavior the way many others have. As Professor Garon observes, instead of trying to help democratize saving, our policy has increasingly deregulated credit, especially during the 1980s and 1990s when credit card borrowing, home equity lines of credit, and subprime mortgage lending all exploded, sweeping unwitting low-income borrowers into the feeding frenzy.

Now that we’re striving to spend our way through an economic recovery, let’s not allow the low-income population to get caught in the groundswell again. Working families need savings incentives even stronger than those our tax system gives to middle- and upper-income families. At a minimum, we shouldn’t allow deficit reduction to undermine the few savings programs designed to help the poor and near-poor. It’s consoling that in the pending FY12 omnibus appropriation Congress didn’t gut individual development accounts (IDAs) under the Assets for Independence Act, which has provided matching funds for the savings accounts of more than 78,000 low-income households since 1998. (The conference committee reduced this program by 16 percent, far less than a 63 percent cut earlier proposed in the House.)

As the economic recovery moves along, the short-term challenge in boosting personal saving will be to help households weather income shocks and meet emergency expenses as they regain liquidity. Looking farther ahead, we need easier ways for would-be small-dollar savers to realize their good intentions. School savings banks and postal savings banks seem antiquated now, but we should focus our energy on devising modern-day, higher-tech equivalents.

Tune in and subscribe today.

The Urban Institute podcast, Evidence in Action, inspires changemakers to lead with evidence and act with equity. Cohosted by Urban President Sarah Rosen Wartell and Executive Vice President Kimberlyn Leary, every episode features in-depth discussions with experts and leaders on topics ranging from how to advance equity, to designing innovative solutions that achieve community impact, to what it means to practice evidence-based leadership.