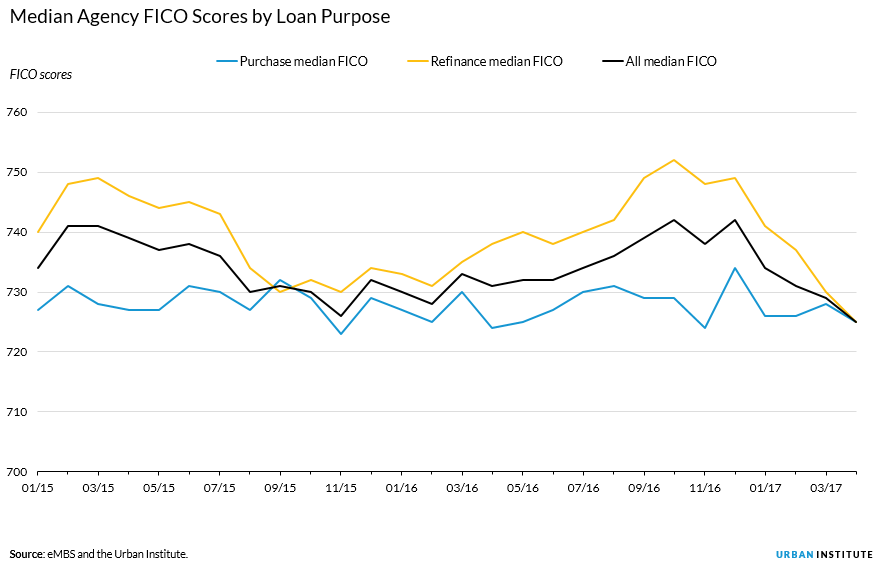

The median FICO score for borrowers approved for agency-originated loans (i.e., those backed by Fannie Mae, Freddie Mac, and Ginnie Mae) has declined from 742 in June 2016 to 725 in April 2017. The present level represents a new low after the 2008 housing crisis (the median FICO score for agency originations briefly touched 726 in November 2015).

But this drop in FICO scores does not necessarily indicate that credit availability is improving. An analysis of agency FICO scores by loan purpose shows that the decline was driven almost entirely by refinance scores. Refinance credit scores fell 27 points from October 2016 (752) to April 2017 (725). Purchase FICO scores, in contrast, declined only 4 points (729 to 725). The figure below illustrates this trend.

One explanation for the refinance-driven reduction in FICO scores is that lenders, in the wake of rising rates, are approving more refinance applications from slightly less creditworthy borrowers to maintain volumes amid a shrinking pool of in-the-money refinance borrowers.

The figure below shows that the share of borrowers who would save money by refinancing has shrunk since last November, when rates began rising.

If lenders are refinancing an increasing number of marginal borrowers from this pool, one would expect the average FICO scores for those who remain in the pool to decline.

An analysis of these “refinanceable” borrowers conducted by the Urban Institute confirms this hypothesis. The average FICO score for borrowers in the refinanceable pool has declined from 716 in October 2016 to 705 in May 2017. At the same time, the share of refinanceable borrowers declined from 41 to 16 percent. The FICO scores in the figure below show this more clearly.

As the pool of refinanceable borrowers has shrunk, lenders have shown more willingness to approve marginal borrowers’ refinance applications.

This doesn’t mean much for overall credit availability. Although a drop in refinance FICO scores is good for current homeowners who can reduce their monthly payments, it doesn’t do anything to ease credit availability for those with less-than-perfect credit who seek to become homeowners for the first time.

Tune in and subscribe today.

The Urban Institute podcast, Evidence in Action, inspires changemakers to lead with evidence and act with equity. Cohosted by Urban President Sarah Rosen Wartell and Executive Vice President Kimberlyn Leary, every episode features in-depth discussions with experts and leaders on topics ranging from how to advance equity, to designing innovative solutions that achieve community impact, to what it means to practice evidence-based leadership.